Taipei 101

Taiwan semiconductor industry 2026.

Taiwan stands as one of the world’s most strategically important economies relative to its physical size and population. With a nominal GDP of $793.2 billion USD (2024) and a population of 23.9 million, the island economy punches vastly above its weight through extraordinary specialization in semiconductor manufacturing, electronics components, and precision manufacturing. Taiwan’s centrality to global supply chains—particularly the semiconductor ecosystem that underpins all modern technology—makes it perhaps the single most consequential island economy in the world. This comprehensive case study examines Taiwan’s economic structure, competitive advantages, geopolitical positioning, and trajectory through 2025-2035.

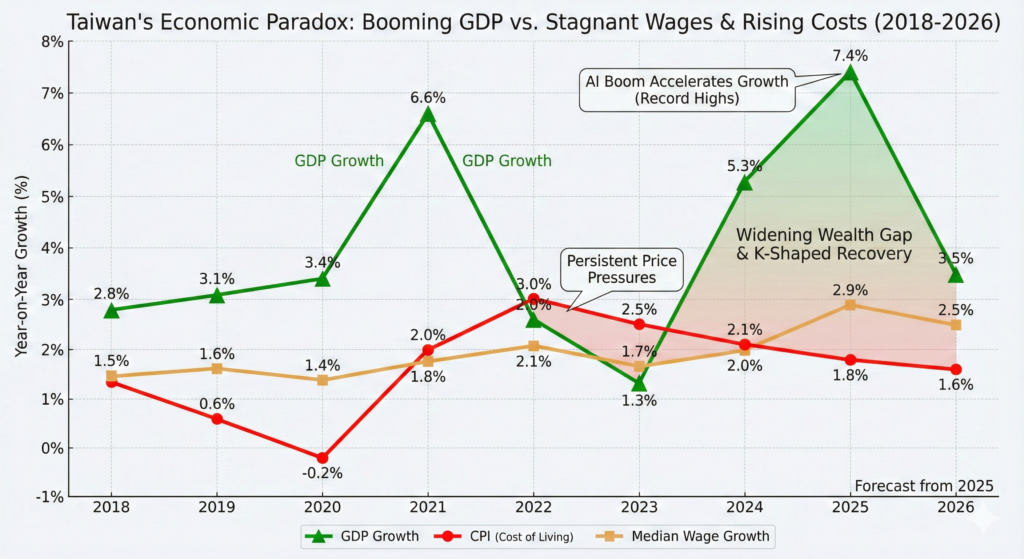

taiwan Economic Performance: AI Boom Accelerates Growth

Taiwan’s economic performance in 2024-2025 reflects the extraordinary impact of global artificial intelligence demand on semiconductor manufacturing and export orders. The economy demonstrated remarkable acceleration, departing from historical trends of modest growth.

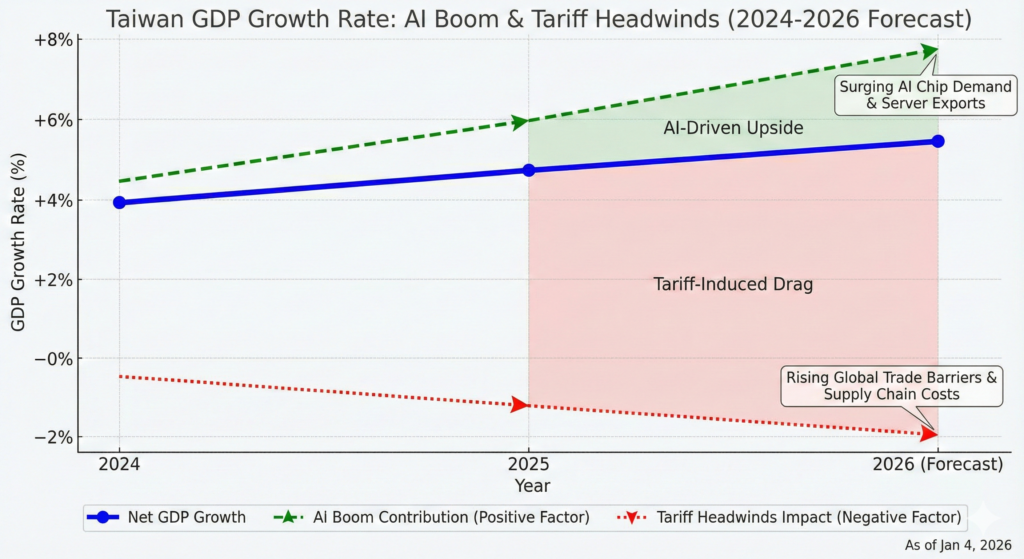

Taiwan GDP Growth Rate: AI Boom and Tariff Headwinds (2024-2026)

2024 Performance: Taiwan’s real GDP grew 4.27% in 2024, a solid performance driven by robust technology sector demand and investment in manufacturing capacity expansion. Nominal GDP reached 25.5 trillion New Taiwan dollars ($793.2 billion USD) at current prices. Taiwan semiconductor industry 2026.

2025 Surge: The Directorate of Budget, Accounting and Statistics dramatically revised 2025 growth forecasts upward from 3.1% (May forecast) to 4.45% (August forecast)—an extraordinary 1.35 percentage point revision—reflecting stronger-than-expected AI semiconductor demand. Quarterly performance tells an even more dramatic story: Q1 2025 recorded 5.45% growth, Q2 accelerated to 8.01%, and Q3 reached 8.21% year-over-year (revised upward from initial 7.64% estimate), marking the fastest growth rate since Q2 2021.

Export growth similarly surged. The statistics agency revised 2025 export projections upward from 8.99% to 24.04%—a 15 percentage point jump—reflecting surging demand for advanced chips and AI servers. Taiwanese export orders hit record highs: $70.2 billion in September 2025, $69.37 billion in October, and $72.9 billion in November 2025 (up 39.5% year-over-year).

2026 Outlook: Despite this strength, the government cautioned about 2026 prospects, projecting deceleration to 2.81% growth as US tariff policies (20% tariffs on Taiwanese goods announced by President Trump) take effect, reducing export momentum. Inflation is projected to remain modest at 1.76-1.93%, reflecting structural deflationary pressures despite commodity price volatility.

TSMC: The Semiconductor Colossus Reshaping Global Technology

Taiwan Semiconductor Manufacturing Company (TSMC) represents not merely a large corporation but the most critical technology chokepoint in the global economy. The company’s market dominance, technical capabilities, and supply chain centrality make it the “silicon shield” of Taiwan’s economic power.

Market Share and Dominance: TSMC’s market share in semiconductor foundry services reached 64.9% in Q3 2024, rising to an estimated 70% in Q2 2025 and 72% by Q3 2025—an extraordinary concentration of global chip production in a single company. This dominance reflects TSMC’s five critical advantages: (1) leading-edge process technology (commercial 2nm production beginning H2 2025), (2) unmatched manufacturing scale and efficiency, (3) premium pricing power from technology leadership, (4) first-mover advantage in advanced node capacity, and (5) ecosystem lock-in through long-term customer relationships.

For context, Samsung (TSMC’s closest competitor) holds only 9.3% of foundry market share, and the top five foundries collectively control roughly 80% of the market—highlighting TSMC’s dominance even within an already concentrated industry.

Revenue and Profitability: TSMC’s Q1 2025 revenue reached $25.52 billion (down 5% quarter-over-quarter but up 22.6% year-over-year), with gross margin expanding to 52.7% and net profit margin reaching 43.1%—exceptional profitability reflecting pricing power and operational excellence. For context, rivals like Samsung operate with 6.1% net profit margins in contrast to TSMC’s 43.1%—a 7x profitability gap illustrating the disparity in value-add capabilities.

Advanced Process Technology Leadership: TSMC is advancing through process nodes with unprecedented speed. Commercial 2nm production commenced in H2 2025, with pathfinding for 1nm extending into the next decade. This technological leadership is non-replicable within the next 5-10 years given extreme capital requirements ($20+ billion per fab), shortage of extreme-ultraviolet (EUV) lithography equipment (ASML dominates with limited annual production), and accumulated process knowledge representing decades of R&D investment.

AI Accelerator Dominance: High-performance computing (primarily AI accelerators for data centers) supplied 52% of TSMC’s wafer revenue in 2025, with AI processors projected to reach 20% of total company sales by 2028. This concentration on AI-driven demand creates both opportunity and vulnerability: opportunity in that AI represents the fastest-growing compute segment, and vulnerability in that economic slowdown or competitive breakthroughs could rapidly shift demand.

Capacity Expansion and Capital Intensity: TSMC’s massive capital expenditure (capex) program expanded manufacturing capacity globally: facilities in Arizona (USA), Japan (partnership with Sony), and Germany (joint venture with Infineon) demonstrate geographic diversification. However, this global expansion raises questions about technology transfer risks and sustainability of TSMC’s capital-intensive model.

Energy and Resource Constraints: TSMC’s electricity consumption reached 7.3% of Taiwan’s total power supply in 2024, with potential to reach 12.5% when 2nm production fully matures—creating vulnerability to Taiwan’s limited renewable capacity and raising carbon emission concerns. Water reuse at 90% and advanced heat recovery partially mitigate resource pressure, but grid constraints represent real limitations.

Taiwan’s Semiconductor Ecosystem: Beyond TSMC

While TSMC dominates foundry services, Taiwan’s semiconductor ecosystem extends across fabless design, original equipment manufacturers (OEMs), and materials/equipment suppliers.

Integrated Circuit Market: Taiwan’s integrated circuit market (encompassing both TSMC and design houses) was valued at $32.28 billion in 2025 and is projected to reach $50.80 billion by 2030 (9.49% CAGR). ICs generated 86.1% of total Taiwan semiconductor revenue in 2024, with microprocessors and AI accelerators employing cutting-edge gate-all-around structures that few global peers can replicate at scale.

Design Houses and Fabless Companies: Design companies controlled 67.9% of 2024 revenue, delivering the single largest slice of the Taiwan semiconductor market. MediaTek exemplifies this dynamic: Q1 2025 saw 14.9% year-over-year sales rebound as AI-centric smartphones penetrated the upper-midrange tier, demonstrating agility of fabless operations avoiding large capex burdens. MediaTek’s forthcoming GB10 Grace Blackwell Superchip (2nm tape-out September 2025) showcases how Taiwan’s design houses depend on TSMC’s leading-edge capabilities while driving innovation.

Original Equipment Manufacturers (OEMs): Taiwan hosts major OEM/ODM (original design manufacturing) companies including Quanta Computer, Compal Electronics, and Pegatron, which assemble consumer electronics, servers, and infrastructure equipment. These companies leverage Taiwan’s design ecosystem, TSMC’s manufacturing capabilities, and supply chain integration to serve global customers.

Packaging and Test Services (OSAT): ASE Technology, the world’s leading assembly, test, and packaging (OSAT) service provider, generates substantial value through advanced packaging—chiplet integration, chip-on-wafer-on-substrate, and co-packaged optics. ASE’s USD 200 million panel-level packaging program (commercial output late 2025) represents emerging value-add opportunity as chiplet architectures and heterogeneous integration become essential for AI performance.

Materials and Specialty Chemicals: Taiwan’s materials and chemical suppliers support semiconductor manufacturing through photoresists, specialty gases, and process chemicals. While less visible than TSMC, these suppliers represent critical vulnerabilities: supply disruptions in rare-earth materials, specialty gases, or photoresists could bottleneck the entire semiconductor value chain.

taiwan Electronics Manufacturing: Diversified Beyond Semiconductors

Taiwan’s electronics manufacturing extends far beyond semiconductors into consumer electronics, IT infrastructure, and emerging categories.

H1 2025 Export Performance: Information, Communication and Audio-video Products exports reached $101.9 billion in H1 2025 (surpassing Parts of Electronic Product for the first time), with electronic products surging $55.6 billion (up 31.4% year-over-year). These categories encompass smartphones, routers, servers, base-station equipment, and consumer electronics—diverse enough to diversify revenue sources while integrated enough to leverage common supply chains.

Major Electronics Companies: ASUS (notebooks, routers, tablets), Acer (notebooks, monitors, desktops), Quanta (servers, notebooks), Compal (notebooks, smartphones), and Foxconn (contract electronics assembly, semiconductors) represent the ecosystem. Foxconn, though headquartered in Taiwan, operates vast facilities in China and Vietnam, leveraging Taiwan’s design capabilities and TSMC’s semiconductor access while maintaining diversified manufacturing footprint.

Advanced Packaging and Integration: As AI chips become more complex, advanced packaging—chiplets, heterogeneous integration, co-designed logic and memory—becomes increasingly critical. Taiwanese OSAT companies (ASE, MediaTek’s internal assembly, TSMC’s back-end capabilities) position the island to capture incremental high-margin value from next-generation compute architectures.

Emerging Growth Sectors: EVs, Green Energy, and Specialty Manufacturing

Beyond semiconductors and consumer electronics, Taiwan is diversifying into electric vehicle components, green energy, and specialized manufacturing.

Electric Vehicle Components: Taiwan is becoming a major supplier of EV-related components: power electronics (inverters, on-board chargers), battery management systems, and sensor modules. Companies like MediaTek (chip design for EV control), TSMC (automotive SoCs), and specialty suppliers are positioning Taiwan as a critical node in the EV supply chain.

Green Energy and Renewables: Taiwan’s government committed to renewable energy expansion, with offshore wind capacity expanding substantially. The island’s solar and wind manufacturing capabilities, combined with battery and energy storage systems, position Taiwan to participate in the global energy transition.

Drone Manufacturing and UAV Ecosystem: Taiwan launched a strategic drone manufacturing program, backed by $1.35 billion (2024-2028) investment, targeting 15,000 units per month production by 2028. Taiwan’s expertise in precision electronics, flight-control ASICs, and miniaturized sensors creates competitive advantage in this emerging category.

tiwan Supply Chain Integration and Export Concentration

Taiwan’s export success rests on vertical supply chain integration: design → semiconductor manufacturing → packaging → OEM assembly → global distribution. However, critical vulnerability exists in geographic concentration.

China and Hong Kong Dependence: 52% of Taiwan’s electronic components were exported to China and Hong Kong in 2024, with an additional 24% to Southeast Asia—meaning 76% of Taiwan’s electronics exports flow through Chinese markets or regional manufacturing hubs. These components are incorporated into final consumption goods (smartphones, computers, servers) that are subsequently exported to Western markets, particularly the USA. This geographic concentration creates geopolitical vulnerability: any China-Taiwan conflict, US-China trade restrictions, or supply chain disruptions could catastrophically impact Taiwan’s export model.

Q2 2025 Tariff Anticipation Orders: The acceleration of export orders in Q2-Q3 2025 reflected customers placing advance orders in anticipation of US tariffs (20% on Taiwanese goods announced for January 2026 implementation). This “pull forward” effect creates artificial demand spike in 2025, with expected deceleration in 2026 once tariffs take effect and orders shift to tariff-advantaged manufacturing locations (Vietnam, India, Mexico).

taiwan Research and Innovation Ecosystem

Taiwan’s competitive advantage rests not merely on manufacturing scale but on a sophisticated research and innovation ecosystem integrating academic institutions, government research centers, and private companies.

National Research Facilities: Taiwan’s National Center for High-Performance Computing, Taiwan Semiconductor Research Institute, and academic centers (National Taiwan University, National Tsing Hua University, National Chiao Tung University) drive semiconductor and electronics research. This ecosystem, while smaller than US or European equivalents in absolute scale, concentrates expertise in relevant domains (advanced packaging, process technology, device design).

Government Industrial Initiatives: The government’s Ten Major AI Infrastructure Projects and Ten Asian-Pacific Strategic Industries program provide directed investment and policy support for emerging sectors (AI, semiconductors, green energy, biomedicine). These initiatives, while smaller in scope than comparable government programs in larger economies, provide strategic focus and capital allocation.

Private R&D Investment: TSMC’s substantial R&D spending (15-20% of revenue in recent years), combined with design house R&D, sustains innovation momentum. However, Taiwan’s R&D intensity remains lower than leading countries like South Korea, Israel, or Switzerland—raising questions about long-term innovation sustainability.

Competitive Positioning and Strategic Risks

Structural Strengths:

- Semiconductor foundry dominance (72% market share, leading-edge technology)

- Diversified electronics manufacturing ecosystem (notebooks, servers, consumer electronics)

- Advanced packaging and materials expertise

- Deep supplier relationships and vertical integration

- Government strategic support for technology sectors

- Skilled engineering and manufacturing workforce

- Export-oriented culture and supply chain expertise

Structural Vulnerabilities:

- Extreme geographic export concentration (76% to China/SE Asia, then to US)

- Geopolitical vulnerability to China-Taiwan tensions

- US-China trade war exposure (tariff risks, export restrictions)

- Dependence on ASML for EUV lithography (single-source risk)

- Limited domestic market (23.9M population, requiring export orientation)

- Energy and water constraints for advanced chip fabrication

- Brain drain of top talent to US and other tech hubs

- Regulatory restrictions on technology exports (semiconductor controls)

Emerging Opportunities:

- AI chip demand sustained growth (9.8% CAGR through 2030)

- Advanced packaging value capture (chiplets, heterogeneous integration)

- EV component supply chain leadership

- Green energy and battery ecosystem participation

- Geopolitical friendshoring (Japanese, US, European investment in Taiwan manufacturing)

- Drone and autonomous system manufacturing expansion

Strategic Risks:

- 2026 tariff deceleration reducing export momentum

- Potential US-China military conflict disrupting supply chains

- Samsung and China SMIC capability advancement threatening TSMC dominance

- Energy transition constraints (power supply, carbon regulations)

- Regulatory export controls limiting semiconductor sales to certain customers

- Economic recession reducing AI infrastructure investment

Conclusion: Strategic Indispensability Amid Geopolitical Uncertainty

Taiwan’s economy, though only $793.2 billion in nominal GDP (less than 1% of global GDP), exercises disproportionate influence over global technology supply chains. TSMC alone manufactures 72% of the world’s advanced semiconductors—the critical inputs for all artificial intelligence, high-performance computing, and next-generation electronics.

The 2025 growth acceleration to 8.21% GDP (Q3, highest since 2021), driven by surging AI chip demand and record export orders ($72.9 billion in November), reflects Taiwan’s extraordinary positioning at the center of the global AI buildout. However, the projected 2026 slowdown to 2.81% growth, driven by anticipated US tariff impacts, illustrates the economy’s vulnerability to geopolitical shocks and external policy shifts beyond Taiwan’s control.

Over the 2025-2035 period, Taiwan faces a fundamental strategic choice: deepening specialization in advanced semiconductors and electronics manufacturing (doubling down on TSMC-centric dominance) versus diversification into new sectors (green energy, EVs, emerging technologies) to reduce geopolitical vulnerability. The government’s Ten Major AI Infrastructure Projects and strategic industry initiatives suggest movement toward both specialization (semiconductor leadership) and diversification (emerging sectors)—a balanced approach reflecting recognition of both Taiwan’s comparative advantage and vulnerability.

Success will ultimately depend on factors beyond Taiwan’s direct control: maintaining access to critical materials and equipment (ASML, specialty gases), avoiding military conflict with China, navigating US-China trade dynamics, and sustaining technological leadership as competitors (Samsung, Intel, China’s SMIC) advance. Taiwan’s economic resilience rests on the geopolitical assumption that the US and allies remain committed to preserving semiconductor supply chain diversity and preventing Chinese monopolization of advanced chip manufacturing.

The island economy’s 2025 boom will be remembered as either the beginning of sustained AI-driven prosperity or a temporary surge before structural constraints and geopolitical risks constrain longer-term growth. The next five years will prove decisive.

Taiwan GDP Growth Rate: AI Boom and Tariff Headwinds (2024-2026)

taiwan Main Government Portal

| Taipei City Government | Taipei City Government |

| Government Portal | Government Portal |

| Executive Yuan | Executive Yuan |

| Ministry of the Interior | Ministry of the Interior |

Read more country case studies done before this.

Downloaded the 70winapp the other day. Easy to install, and surprisingly fun. Perfect for when you’re just chilling at home. Give it a shot and see if you can win big. Get started here 70winapp!