The United Arab Emirates

UAE investment and infrastructure 2026

Executive Summary

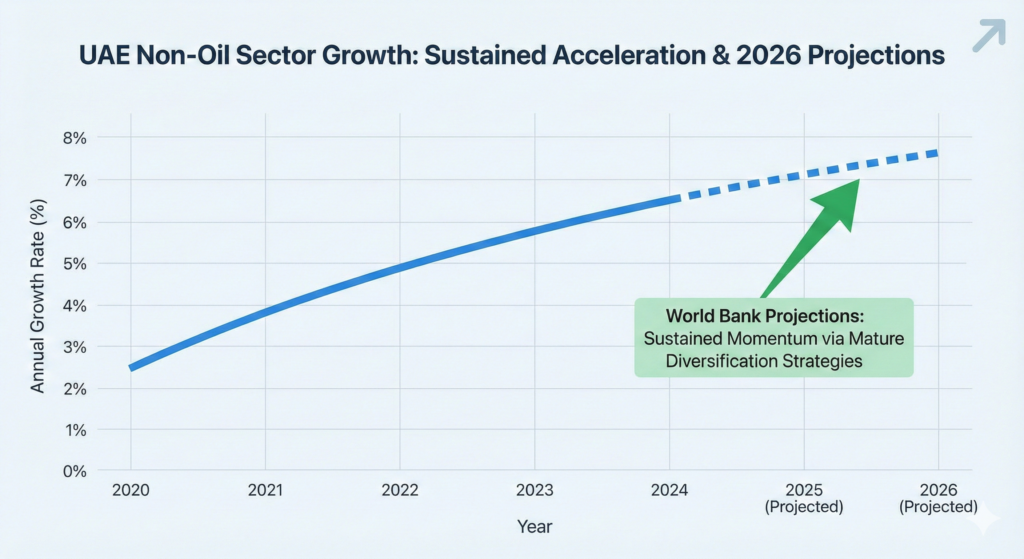

The United Arab Emirates has executed one of the world’s most successful economic transformation programs, evolving from an oil-dependent economy to a diversified, innovation-driven powerhouse with global competitive relevance. As of 2024, non-oil sectors contribute 75.5% of the UAE’s AED 1.776 trillion ($483 billion) economy, a remarkable shift from 46.71% a decade earlier. The UAE’s 4.0% GDP growth in 2024—with World Bank projections of 4.6% in 2025 and 4.9% in 2026—demonstrates the structural resilience of this diversification strategy. With AAA credit ratings from S&P, Moody’s, and Fitch (all with stable outlooks), the UAE has positioned itself as a stable, predictable investment destination in a volatile region. The nation’s strategic vision for 2031 targets doubling GDP to AED 3 trillion while generating AED 800 billion in non-oil exports and AED 4 trillion in total foreign trade value. This case study examines how business-friendly policies, world-class infrastructure, fintech innovation, renewable energy leadership, and strategic trade agreements have transformed the UAE into a global economic hub, attracting over $15 billion in major foreign direct investment announcements in 2024-2025 alone.

Macroeconomic Positioning and Fiscal Strength

The UAE’s economic resilience rests on two complementary pillars: fiscal discipline and structural diversification. The nation’s sovereign credit rating of AA from all three major agencies reflects more than financial stability—it signals institutional credibility in a region marked by geopolitical volatility. The Federal Competitiveness and Statistics Centre reports that in the first half of 2024, total real GDP reached AED 879.6 billion with 3.6% growth, while non-oil GDP alone expanded at a faster 4.4% clip, growing to approximately AED 660 billion. This consistent non-oil outpacing of total GDP growth indicates that the diversification strategy is actively accelerating.

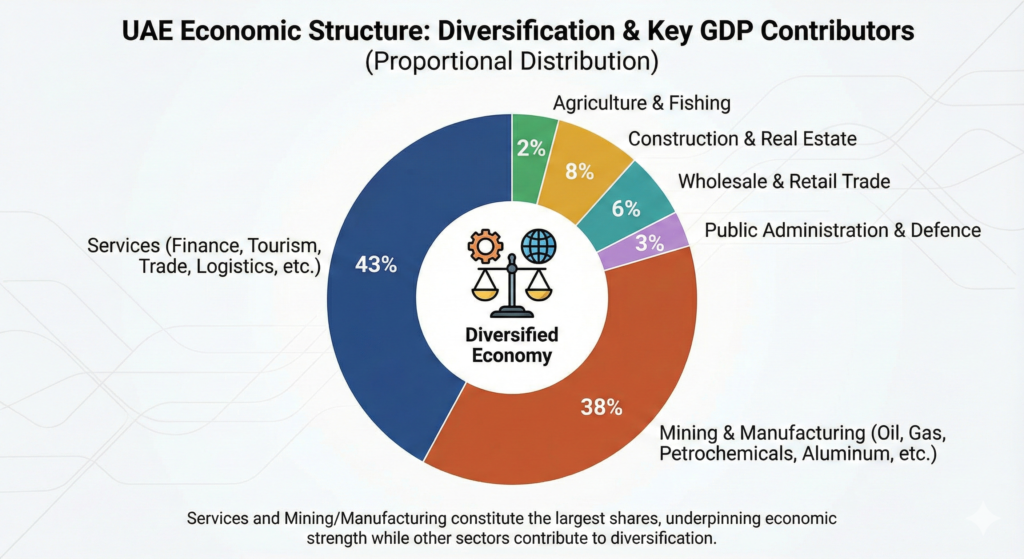

Non-oil sector contribution has grown from 46.71% of GDP over the past decade to 58.21% in 2023, establishing services as the economy’s largest sectoral engine at 33.1% of GDP, followed by mining, manufacturing, and utilities at 29.94%. The services sector’s expansion reflects the UAE’s success in developing high-value sectors: financial services, tourism, logistics, and technology-enabled businesses. Critically, oil and gas production growth—projected at 2% for 2025 with the UAE implementing a gradual OPEC+ quota increase to 5 million barrels per day by 2027—remains supplementary rather than central to economic expansion. This structural shift insulates the UAE from crude price volatility while enabling reinvestment of hydrocarbon revenues into strategic sectors with higher multiplier effects.

The Fintech Revolution: Becoming the Middle East’s Financial Innovation Leader

The UAE’s fintech ecosystem has emerged as one of the world’s fastest-growing financial technology markets. The sector attracted USD 265 million in startup funding in 2024—representing approximately one-third of all venture capital flowing into UAE startups—demonstrating the investment community’s confidence in the region’s fintech potential. The broader fintech market is projected to grow from USD 3.16 billion in 2024 to USD 5.71 billion by 2029, representing an expansion of 80.7% over five years. The underlying CAGR of fintech investment exceeds 15%, double the global fintech growth rate, positioning the UAE as the fastest-growing fintech jurisdiction in the MENA region.

The digital payments segment exemplifies this expansion. Transaction values reached USD 27 billion in 2023 and are projected to reach USD 37.45 billion by 2028. This 38% expansion reflects both population growth and behavioral shifts toward digital payments. The Central Bank of the UAE (CBUAE) has institutionalized this momentum through its FinTech Strategy centered on Open Banking APIs, enabling third-party providers (TPPs) to layer innovative services on top of incumbent financial institutions’ infrastructure. The regulatory framework explicitly supports Open Insurance and Open FX innovations, positioning the UAE as a genuine financial technology incubator rather than merely a fintech user.

A critical success factor has been the integration of artificial intelligence into fintech operations. Emirates NBD’s evolution from pre-AI to post-AI operations has delivered measurable improvements in fraud detection, credit scoring, compliance automation, and risk modeling. Islamic fintech represents another distinctive UAE advantage—Sharia-compliant solutions are booming as global capital seeks halal lending platforms and digital Islamic savings accounts. The UAE’s position as the Islamic finance capital of the world, combined with its technological leadership, creates a unique arbitrage opportunity for fintech entrepreneurs.

Free zones such as Hub71 and the Abu Dhabi Global Market (ADGM) provide institutional scaffolding for fintech growth. Hub71 alone supports 300 startups that have collectively raised AED 9 billion ($2.45 billion) and generated AED 5 billion ($1.36 billion) in revenue. The ecosystem offers 100% subsidies for early-stage startups, access to venture capital networks, and mentorship from successful founders—dramatically reducing the cost and risk of entrepreneurship. Government equity-free incentives enable founders to retain ownership while accessing capital, differentiating Hub71 from traditional venture accelerators.

uAE Artificial Intelligence: From Strategy to Gigawatt-Scale Infrastructure

The UAE’s AI ambitions have evolved from aspirational government statements in 2017 to concrete, capital-intensive infrastructure investments. In October 2017, the UAE became the world’s first nation to appoint a Minister of State for Artificial Intelligence, establishing the institutional architecture for AI leadership. The updated UAE Artificial Intelligence Strategy 2031 aspires to position the UAE as a global leader by 2031 through enhanced integration across healthcare, education, government services, and defense.

The market opportunity is staggering. The AI market was valued at USD 1.257 billion in 2025 and is projected to reach USD 4.285 billion by 2030—a 241% expansion. More significantly, AI is expected to contribute 13.6% of the UAE’s total GDP by 2030, with AI and digital industries accounting for 12% of non-oil GDP in 2025 and reaching 20% by 2030. This is no longer a peripheral sector; it is being positioned as a structural economic driver comparable to financial services in developed economies. UAE investment and infrastructure 2026.

The infrastructure investment backing these projections is unprecedented. Abu Dhabi has announced strategic investments of approximately $35 billion in AI and digitalization over 2025-2027. Microsoft’s $15 billion investment in G42 (announced April 2024) represents the single largest foreign direct investment commitment in the region, with an additional $1 billion AI innovation fund established jointly. In May 2025, during President Trump’s visit to Abu Dhabi, G42 announced the Stargate UAE project in partnership with OpenAI, Nvidia, Cisco, SoftBank, and Oracle—a 5 GW AI data center campus with Phase One (200 MW capacity) expected by 2026. This project alone will cost billions and establish the UAE as a critical computing hub for global AI development.

The current data center landscape reflects this buildout momentum. The UAE currently hosts over 250 MW of live data center capacity, with an additional 5.5 GW under construction. Dubai has 18 operational centers while Abu Dhabi has 16, but Abu Dhabi leads in asset value at USD 1.23 billion compared to Dubai’s USD 815 million, reflecting the capital intensity of enterprise-grade AI infrastructure. Eleven new data centers worth USD 3 billion are under construction with expected completion by 2026, while six more in pre-execution phases carry a USD 41 billion valuation (USD 40 billion of which is allocated to the G42 AI Campus).

The renewable energy-AI nexus represents a strategic insight underlying UAE’s AI infrastructure strategy. Data centers and AI workloads consume extraordinary amounts of electricity—the Stargate campus alone will require 5 GW of continuous baseload power. Masdar’s $6 billion world-first 24/7 renewable energy project directly addresses this constraint. The facility combines a 5.2 GW solar photovoltaic capacity with a 19 gigawatt-hour battery energy storage system (BESS), enabling 1 GW of uninterrupted renewable baseload power. Completed by 2027, this project will supply clean power to data centers and AI operations while avoiding 5.7 million tons of annual carbon emissions—aligning AI growth with the UAE’s Net Zero 2050 commitment.

uAE E-Commerce: Transforming Middle Eastern Digital Retail

The UAE e-commerce market has become the region’s largest and fastest-growing digital retail ecosystem. The market reached USD 79.94 billion in 2024 and is projected to expand to USD 270.5 billion by 2032, representing a compound annual growth rate (CAGR) of 16.46% from 2026-2032. This exceptional growth trajectory reflects three structural tailwinds: demographic factors, infrastructure maturity, and government policy.

Demand-side infrastructure is nearly complete. Smartphone penetration in the UAE reached 97.6% by 2023, while internet penetration extended to 99% of the population—among the world’s highest rates. Mobile shopping specifically surged 41% year-on-year in 2023, with the average UAE consumer conducting 3.7 online transactions monthly. The psychological shift toward digital commerce, accelerated by COVID-19 and sustained through habit formation, has produced a permanent 23% increase in Dubai e-commerce transactions relative to pre-pandemic 2019 levels.

Business-to-consumer (B2C) transactions dominate the market at 68% of total value, with approximately AED 38 billion in B2C sales recorded in 2023. Leading platforms such as noon.com and Amazon.ae serve over 12 million active users, operating in an ecosystem where the top e-commerce verticals by revenue are consumer electronics, fashion (enabled by virtual try-on technology and AI recommendations), and home goods. Government initiatives like Smart Dubai have further accelerated adoption by promoting digital transformation across the emirate’s administrative and commercial infrastructure.

The supply-side infrastructure is equally sophisticated. Dubai alone generated AED 80 billion (approximately USD 21.8 billion) in logistics and supply chain value during 2023, with e-commerce fulfillment services expanding at 27% annually. The digital economy currently contributes 4.3% of the UAE’s GDP, with government targets of 20% by 2031—implying that e-commerce and digital services will drive substantial future economic growth. The Dubai Digital Government Strategy and Smart Dubai initiative have systematized the digital-first approach, creating a regulatory and operational environment that competitors in the region cannot easily replicate.

uAE Tourism: From Iconic Destinations to Structural Economic Engine

Tourism has evolved from an ancillary sector to a major economic pillar. In 2024, the travel and tourism sector contributed AED 257.3 billion to the UAE’s GDP, representing 13% of total economic output and demonstrating 3.2% growth relative to 2023. The sector’s contribution has grown 26% from pre-pandemic 2019 levels, proving that Dubai and Abu Dhabi are not merely recovering but expanding their global tourism position.

International visitor spending reached AED 217.3 billion in 2024, growing 5.8% from 2023 and 30.4% from 2019. The UAE hosted 29 million international visitors in 2024, with projections of 22 million visitors to Dubai alone in 2025. The top visitor markets are India (14%), United Kingdom (8%), Russia (8%), China (5%), and Saudi Arabia (5%), with the remainder distributed across 60% of other global regions—indicating genuine global appeal rather than concentration in specific markets.

Hotel sector metrics validate the strength of tourism demand. Revenue from hotel establishments reached nearly AED 45 billion in 2024, with occupancy rates climbing to 78%—among the world’s highest regional benchmarks. The sector hosted 30.75 million hotel guests in 2024, a 9.5% increase from 2023, with projections suggesting 33 million guests in 2025. The sector is expected to generate AED 48 billion in revenue in 2025, an increase of 7% year-over-year. Hotel establishments grew to 1,243 properties with over 216,000 rooms by mid-2025, with 16 new hotels entering the market during 2024 alone.

Aviation infrastructure underpins this growth. Total passenger traffic through UAE airports exceeded one billion passengers between 2015 and 2024, reflecting the capacity investment in facilities such as Sheikh Khalifa International Airport (Dubai) and Abu Dhabi International Airport. In the first eight months of 2025 alone, the UAE handled 102.9 million passengers, representing 5.3% growth compared to the same period in 2024. The expansion of airport capacity and launch of new international routes position the UAE to handle 160 million passengers by year-end 2025.

Tourism investments attracted by the UAE totaled AED 32.2 billion in 2024, rising from AED 28.8 billion in 2023 and projected to reach AED 35.2 billion in 2025. These capital inflows fund landmark attractions such as the expansion of Sheikh Khalifa International Airport and the Louvre Abu Dhabi, creating virtuous cycles of visitor growth, investment attraction, and employment generation. The “World’s Coolest Winter” campaign, across its five editions, has generated approximately AED 6.7 billion in hotel revenues alone.

UAE Real Estate: Capital Appreciation and Strategic Development

The UAE’s real estate market combines robust transaction volumes with institutional infrastructure quality. The residential and commercial real estate sector is projected to expand from USD 82.41 billion in 2024 to USD 132.39 billion by 2030, representing an 8.06% CAGR. The Dubai Real Estate Sector Strategy 2033 targets even more ambitious outcomes: doubling the sector’s GDP contribution to approximately AED 73 billion, increasing transaction volumes by 70%, and expanding the market value to AED 1 trillion.

Transaction volumes validate the underlying demand. In the first nine months of 2024 alone, Dubai recorded over 163,000 transactions valued at more than AED 544 billion, while real estate investments exceeded AED 376 billion during the same period. The H1 2024 transaction value reached AED 306.3 billion—a 36% increase from the same period in 2023. Q1 2025 transactions alone reached AED 239 billion, indicating sustained momentum into 2025.

Price dynamics reflect scarcity-driven appreciation. Dubai’s residential market prices increased 4.3% in Q3 2024, with a 19.9% year-on-year appreciation. Ras Al Khaimah experienced even more dramatic growth: 39% year-on-year residential price appreciation in Q1 2025, with average apartment values reaching AED 1,684 per square foot and villa values averaging AED 1,145 per square foot. The emirate recorded over 1,300 off-plan residential sales transactions valued at AED 2.4 billion during Q1 2025 alone. These price trajectories, combined with rental yields ranging from 6% to 6.8%, attract institutional investors seeking both capital appreciation and income generation.

Branded residences have emerged as a premier investment category for high-net-worth individuals. Global hospitality brands are expanding their branded residential footprint, with approximately 4,800 branded units projected for completion through 2030 in Ras Al Khaimah alone—representing 25% of upcoming freehold supply in the emirate. These properties combine the prestige of luxury brands (such as Wynn, North One, and others) with real estate investment characteristics, creating a hybrid asset class that appeals to international affluent capital.

Strategic mega-projects shape the development trajectory. Masdar City in Abu Dhabi continues to evolve as a sustainable urban development offering exceptional opportunities for commercial real estate investment, particularly for businesses in renewable energy, clean technology, and sustainable urban solutions. The 5.2 GW solar facility and battery storage systems being developed within Masdar City provide the infrastructure foundation for AI and data center clustering, creating synergistic development dynamics.

Renewable Energy: Global Innovation Leadership

The UAE has positioned itself at the forefront of global renewable energy innovation, combining gigawatt-scale solar deployment with cutting-edge energy storage technology. The nation’s renewable energy capacity has expanded dramatically, with the Mohammed bin Rashid Al Maktoum Solar Park in Dubai targeted to reach 5,000 MW capacity by 2030. The Al Dhafra Solar Plant in Abu Dhabi, operational as of 2024, contributes 2 GW of capacity and demonstrates the UAE’s commitment to record-scale projects.

The most innovative project is Masdar’s world-first 24/7 renewable energy facility—a $6 billion investment combining 5.2 GW of solar photovoltaic capacity with a 19 gigawatt-hour battery energy storage system (BESS). This facility delivers 1 GW of guaranteed baseload renewable power around the clock, directly addressing the intermittency challenge that historically limited renewable energy deployment. Upon completion by 2027, the facility will avoid 5.7 million tons of annual carbon emissions and meet one-third of the UAE’s 2030 renewable energy targets. The project incorporates AI-enhanced forecasting and intelligent dispatch systems, optimizing energy storage and delivery in real time.

Masdar’s global renewable energy ambitions extend far beyond UAE borders. The company operates in more than 40 countries and has developed the world’s largest offshore wind farm and delivered multiple gigawatt-scale projects including the 2 GW Al Dhafra facility and the 800 MW Phase 3 of the Mohammed bin Rashid Solar Park. The UAE government has committed more than $20 billion to renewable energy programs through Masdar, with the company actively pursuing global expansion across Asia, Europe, Africa, and the United States.

The renewable energy sector directly enables the AI infrastructure buildout. Data centers consume extraordinary amounts of electricity, and the alignment of renewable energy capacity with AI data center location strategy creates a unique competitive advantage for the UAE. The grid infrastructure being developed to support the 24/7 renewable facility—including virtual power plant capabilities, grid-forming technology, and black-start capabilities—represents world-leading technology deployment.

Strategic Framework: Free Zones and Business-Enabling Policy

The UAE’s 40+ free zones represent a centerpiece of economic diversification strategy, accounting for 60% of new business registrations and contributing substantially to non-oil GDP. These zones provide a business framework unmatched globally: 100% foreign ownership with no local partner requirements, zero corporate and personal income tax (in most zones), full repatriation of profits and capital without restriction, and streamlined licensing with processing times measured in days rather than months.

The sectoral differentiation of free zones creates specialized innovation ecosystems. Dubai Internet City and Dubai Media City serve the digital and creative industries; Jebel Ali Free Zone (JAFZA) and Dubai South focus on logistics and trade; RAKEZ and Hamriyah Free Zone support advanced manufacturing; twofour54 in Abu Dhabi targets media and gaming; and emerging zones like Dubai CommerCity specialize in e-commerce and digital trade. Each zone provides world-class infrastructure including office spaces, warehousing, high-tech facilities, and proximity to global transport networks (ports, airports, soon rail).

JAFZA deserves particular attention as the world’s largest free zone by area. Connected to Jebel Ali Port—one of the world’s busiest container ports serving 150+ ports globally via 180+ shipping lines—JAFZA provides integrated sea, road, and air connectivity. The port ecosystem includes 310 berths with collective cargo capacity exceeding 80 million tons, making the UAE’s maritime infrastructure a critical node in global trade. This infrastructure advantage enables U.S. exporters and other foreign businesses to use the UAE as a diversified re-export hub accessing high-growth markets across the Middle East, Africa, and South Asia.

Hub71, Abu Dhabi’s technology ecosystem, exemplifies the evolution of free zones toward innovation enablement. Established in 2019 as a flagship initiative of the Ghadan 21 economic accelerator program (AED 50 billion investment), Hub71 has scaled to support 300 startups that have collectively raised AED 9 billion and generated AED 5 billion in revenue. The ecosystem now includes four specialist communities: Hub71+ AI (supporting 24 investors and 15 new strategic partners as of 2025), Hub71+ Digital Assets, Hub71+ ClimateTech, and Hub71+ Life Sciences (launched 2025). Cohort 15 brought 21 new startups from 80% non-UAE origins, demonstrating Hub71’s ability to attract international entrepreneurial talent.

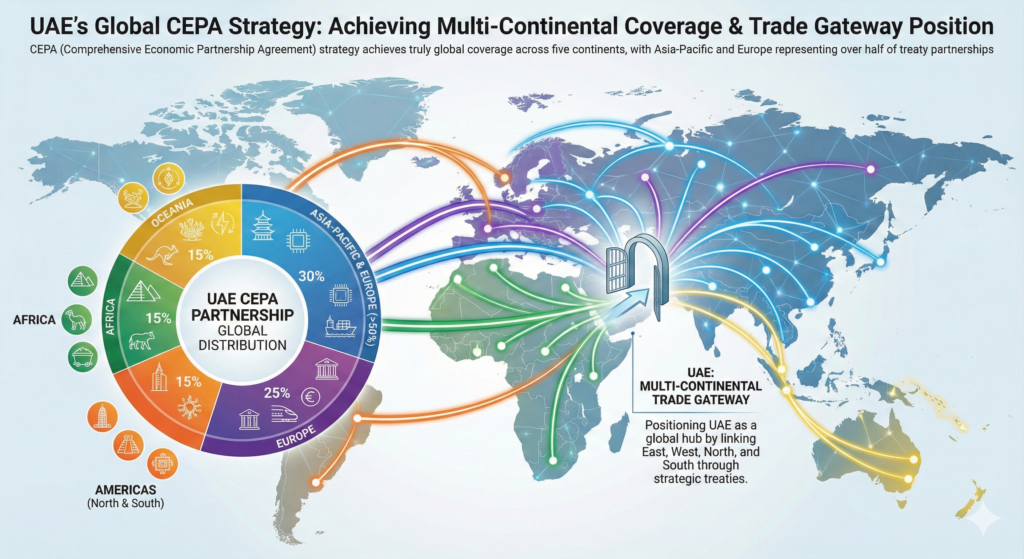

Global Trade Integration: The CEPA Strategy

The Comprehensive Economic Partnership Agreement (CEPA) program represents the UAE’s systematic approach to constructing global trade relationships on favorable commercial terms. As of December 2024, the UAE had concluded 24 CEPAs covering approximately 2.5 billion people—about 25% of the global population.

The results are quantifiable. The UAE-India CEPA, concluded in February 2022, has delivered exceptional trade growth. Non-oil trade between the two countries grew 20.5% by end-2024, with UAE exports to India jumping 75%. India-UAE bilateral trade reached USD 85 billion in 2023-24 with a target of USD 100 billion by 2027. The UAE-Jordan CEPA, which entered into force in May 2025, covers energy, logistics, tourism, and pharmaceuticals, with bilateral trade already reaching USD 5.62 billion in 2024 (a 34% year-on-year increase).

In 2025 alone, the UAE signed five new CEPAs with Malaysia, New Zealand, Kenya, Ukraine, and the Central African Republic. Notably, the UAE is in final-stage negotiations with Japan—a major economy that would expand the UAE’s trade network within Asia’s largest developed market. The CEPA strategy explicitly targets non-oil trade expansion, renewable energy, technology, financial services, green industries, advanced materials, agriculture, and sustainable food systems—aligning bilateral trade agreements with Vision 2031 economic diversification targets.

The geographic distribution of CEPA partnerships spans all continents: 30% Asia-Pacific (reflecting strategic focus on India, Indonesia, China, and ASEAN), 25% Europe, 20% Africa (addressing growing African trade potential), 15% MENA and other regions, and 10% Americas. This global footprint positions the UAE as a genuinely global trader rather than a regional player constrained by geographic proximity.

Government Vision: “We the UAE 2031” Strategic Roadmap

The “We the UAE 2031” vision provides the strategic framework directing all government economic initiatives. The plan aspires to double the UAE’s GDP from AED 1.49 trillion to AED 3 trillion by 2031—a compound annual growth target of approximately 8-9%. This ambitious target is supported by four strategic pillars: Forward Economy, Forward Society, Forward Diplomacy, and Forward Ecosystem.

The Forward Economy pillar targets AED 800 billion in non-oil exports and AED 4 trillion in total foreign trade value by 2031, up from current levels of approximately AED 400-450 billion and AED 2.5 trillion respectively. Foreign direct investment inflows are targeted at AED 240 billion annually (USD 65 billion) by 2031, compared with recent annual inflows of AED 32-35 billion. Tourism is targeted to contribute AED 450 billion to GDP, representing growth from current levels of AED 257 billion.

The Advanced Manufacturing pillar emphasizes the “Make it in the Emirates” initiative, which aims to transform the UAE from a simple assembly economy to one producing sophisticated, high-tech industrial products with significant local content. The Digital Economy pillar prioritizes AI, fintech, and modern digital services—sectors where the UAE demonstrates genuine competitive advantage. The Logistics & Connectivity pillar seeks to reinforce the UAE’s position as the world’s premier trade and logistics hub connecting Asia, Europe, and Africa.

The Renewable Energy & Green Economy pillar aligns with the UAE Centennial 2071 vision of net-zero emissions by 2050. The plan emphasizes clean energy transition, sustainable finance, and circular economy principles across all economic sectors. This commitment is not aspirational; it is being operationalized through Masdar’s renewable energy investments, clean technology free zones, and the integration of sustainability metrics into corporate governance and capital allocation decisions.

Implementation is systematic. The National Investment Strategy 2031 directs government capital toward priority sectors, while legislative reforms create agile regulatory frameworks supporting emerging industries. Public-private partnerships are leveraged to accelerate innovation deployment, with the government providing strategic capital while private sector expertise executes operational delivery. Digital transformation of government services—using AI, blockchain, and advanced data analytics—aims to eliminate inefficiencies and reduce transaction costs for businesses.

Smart Infrastructure and Digital Government

The UAE’s smart city initiatives represent a comprehensive integration of digital technology, artificial intelligence, and sustainable infrastructure into urban planning and governance. Abu Dhabi Smart City and Dubai Smart City are flagship projects incorporating IoT sensors, AI-driven management systems, blockchain-based governance, and renewable energy integration.

Smart Dubai specifically aims to make Dubai the world’s happiest and smartest city through six key pillars: economy, living, governance, environment, people, and mobility. The Dubai Paperless Strategy eliminates paper transactions, while the Dubai Blockchain Strategy applies distributed ledger technology to government services and commercial transactions. AI-driven security systems incorporating facial recognition, traffic management platforms using machine learning for predictive congestion management, and automated government services exemplify the technology deployment.

Masdar City represents the most integrated smart city model, combining AI-powered systems with renewable energy infrastructure. The city integrates low-carbon urban design with digital systems for real-time resource optimization, positioning it as a living laboratory for sustainable urban development.

The digital government evolution has been accelerative. The Telecommunications and Digital Government Regulatory Authority (TDRA) has integrated generative AI into the Unified Digital Platform and “U Ask” services, streamlining government information access. In February 2025, the Ministry of Finance released a consultation on standardized invoice formats and a Peppol-based Decentralized Continuous Transaction Control and Exchange (DCTCE) model, enabling real-time verification of invoices through secure digital platforms. These systems reduce compliance costs for businesses while improving government tax administration efficiency.

Public-private partnerships accelerate deployment. Intel partnered with Abu Dhabi Digital Authority in 2020 to conduct workshops on blockchain, augmented reality, video analytics, IoT, and AI. Huawei partnership with Dubai Municipality supports digital capability development and smart service launches. These collaborations combine government regulatory authority with private sector technological expertise.

Competitive Advantages and Positioning

The UAE’s position as a global economic hub rests on multiple reinforcing competitive advantages that are difficult for competitors to replicate:

Geographic and Logistical Supremacy. The UAE occupies a critical position connecting Asia, Europe, and Africa. The 12 commercial ports with 310 berths and 80+ million-ton capacity, combined with world-class airports and developing rail infrastructure (Etihad Rail), create a logistics ecosystem of unmatched comprehensiveness in the Middle East. Over 61% of GCC cargo flows through UAE ports, establishing the nation as the region’s uncontested logistics leader.

Institutional Credibility. The AA credit rating from all three major rating agencies provides sovereign risk reassurance unmatched in the Middle East except for Qatar. The stable outlook reflects confidence in the durability of economic and governance structures across multiple cycles and administrations.

Regulatory Progressiveness. The appointment of a Minister of State for Artificial Intelligence, establishment of financial regulatory sandboxes, and continuous evolution of legal frameworks for emerging technologies position the UAE ahead of most developed economies in regulatory adaptability.

Capital Availability and Velocity. The concentration of sovereign wealth in Abu Dhabi (via Mubadala, the State General Reserve Fund, and others), combined with access to global capital markets through ADGM and DIFC, provides entrepreneurs and businesses with capital availability unmatched in emerging markets. The velocity with which capital can be deployed—$15 billion Microsoft investment, $6 billion Masdar renewable project, $40 billion Stargate campus—demonstrates execution capacity.

Technology Infrastructure. Internet penetration at 99% and smartphone penetration at 97.6% exceed most developed economies. The buildout of 5.5 GW data center capacity under development, combined with 1 GW of guaranteed renewable baseload power coming online by 2027, positions the UAE to support AI and advanced technology applications at scale.

Human Capital Attraction. The Golden Visa and Green Visa programs provide long-term residency pathways for high-net-worth individuals and specialized professionals. The establishment of MBZUAI (Mohamed bin Zayed University of Artificial Intelligence) and other specialized institutions create talent pipelines and retain talent within the emirate.

Tax Efficiency. The absence of corporate and personal income tax in most free zones, combined with exemptions from import/export duties, reduces the cost of capital and operations below levels available in competing jurisdictions.

Strategic Challenges and Future Development Vectors

While the UAE’s diversification strategy has delivered exceptional results, several challenges require strategic management to sustain momentum:

Energy Intensity of AI Infrastructure. The power demands of large-scale AI data centers and computing operations are extraordinary. While the 24/7 renewable energy facility addresses this constraint partially, continued AI expansion will require additional renewable capacity buildout and potentially nuclear energy integration (Abu Dhabi has nuclear capacity operating since 2020).

Talent Shortage in Specialized Sectors. Rapid expansion in fintech, AI, and advanced manufacturing has created demand for highly specialized technical talent that outpaces domestic supply. While visa programs attract international talent, the pace of integration and knowledge transfer remains a constraint.

Regional Integration of Free Zones. Historically, free zone businesses operated separately from mainland UAE commerce. Recent policy shifts are fostering integration, but regulatory harmonization across emirates and between free zones and mainland jurisdictions requires continued coordination.

Renewable Energy Intermittency Solutions. While the 24/7 facility addresses this challenge for new projects, the broader power grid integration of massive renewable capacity requires continued investment in battery storage, grid modernization, and demand management systems.

Conclusion

The United Arab Emirates has executed a master-class in economic diversification, transforming from an oil-dependent economy to a multifaceted, innovation-driven hub with global competitive relevance. The rise of non-oil sectors to 75.5% of GDP, the deployment of AED 50 billion+ in innovation infrastructure (Hub71, Masdar, and free zones), and the attraction of $15+ billion in major foreign direct investment announcements in 2024-2025 demonstrate the strategic efficacy of this transformation.

The UAE’s positioning across fintech, artificial intelligence, e-commerce, tourism, renewable energy, and advanced logistics creates a portfolio of high-growth sectors with structural tailwinds extending through 2031 and beyond. The Vision 2031 ambition to double GDP to AED 3 trillion while generating AED 800 billion in non-oil exports is architecturally sound and supported by concrete investments in infrastructure, regulatory frameworks, and human capital.

For multinational enterprises, investors, and entrepreneurs, the UAE offers a rare combination of stability, growth opportunity, regulatory progressiveness, and global connectivity. The world-class free zones provide operational bases for regional expansion; the CEPA network provides preferential market access across 2.5 billion consumers; the renewable energy infrastructure provides sustainable power for technology operations; and the institutional capacity for execution provides confidence that announced initiatives will be delivered.

As geopolitical risk persists elsewhere in the Middle East and global supply chains seek geographic diversification, the UAE’s position as a business-friendly, technology-forward hub with institutional credibility and proven execution capacity positions the nation to capture a disproportionate share of regional capital flows, talent migration, and foreign direct investment through 2031 and beyond.

UAE’s economic structure is diversified across multiple sectors, with services and mining/manufacturing forming the largest contributors to GDP

UAE’s economic structure is diversified across multiple sectors, with services and mining/manufacturing forming the largest contributors to GDP

UAE demonstrates leadership across multiple high-value sectors, combining regional dominance with globally competitive positioning in emerging areas like renewable energy and fintech

UAE’s CEPA strategy achieves truly global coverage across five continents, with Asia-Pacific and Europe representing over half of treaty partnerships, positioning UAE as a multi-continental trade gateway

UAECentral Government Portals

| Official UAE Government Portal | Official UAE Government Portal |

| Ministry of Foreign Affairs & International Cooperation | Ministry of Foreign Affairs & International Cooperation |

| Ministry of Health and Prevention | Ministry of Health and Prevention |

| Ministry of Education | Ministry of Education |

| Ministry of Interior | Ministry of Interior |

| Ministry of Economy & Tourism | Ministry of Economy & Tourism |

| Ministry of Industry and Advanced Technology | Ministry of Industry and Advanced Technology |

| Ministry of Climate Change and Environment | Ministry of Climate Change and Environment |

Read more country case studies done before this.

| china | china |

| hong kong | hong kong |

| japan | japan |

| sinagpore | singapore |

| taiwan | taiwan |

| india | india |

| south korea | south korea |

| isreal | isreal |

Rummy calling, nabobrummy answering! Been playing on this one and honestly, it’s keeping me entertained. Give it a go if you fancy a round. Get on over to nabobrummy