Saudi non-oil economy growth 2026

Executive Summary

Saudi Arabia stands at a strategic inflection point in its economic history. Launched in April 2016, Vision 2030 represents an unprecedented attempt by a petro-state to fundamentally restructure its economy away from hydrocarbon dependence toward diversified, sustainable growth engines. With nine years of implementation now complete, the initiative has achieved measurable progress across multiple dimensions: non-oil sectors now contribute 50-51% of GDP, unemployment has dropped to 7% (six years ahead of schedule), and the Public Investment Fund has grown 390% to $941.3 billion in assets. Yet the scale of ambition remains extraordinary, and execution risks—particularly around oil price volatility, foreign capital attraction, and structural labor market challenges—remain material. This case study examines Vision 2030’s strategic framework, evaluates progress across key diversification pillars, analyzes competitive positioning within the region, and identifies critical success factors for achieving the 2030 vision.

Part 1: Vision 2030 Strategic Framework and Evolution

Three Core Pillars and Strategic Coherence

Vision 2030 rests on three integrated pillars designed to address Saudi Arabia’s core vulnerabilities: creating a vibrant society, building a thriving economy, and establishing the kingdom as a global investment powerhouse. The framework emerged from a stark recognition: at current oil dependency levels, any marked decline in global oil demand would trigger severe economic contraction. Crown Prince Mohammed bin Salman’s vision transcends traditional industrial policy, incorporating social reform, geopolitical positioning, and long-term fiscal sustainability into an interconnected strategy.

The “vibrant society” pillar encompasses social modernization—including women’s labor force participation (now 35.4%, doubled from 17% in 2017), cultural opening, and entertainment sector development. The “thriving economy” pillar focuses on economic diversification into tourism, mining, advanced manufacturing, technology, and renewable energy. The “ambitious nation” pillar targets global connectivity and positioning Saudi Arabia as a bridge between Africa, Asia, and Europe. This coherence distinguishes Vision 2030 from fragmented sectoral policies, creating synergies where mega-projects like NEOM simultaneously advance urbanization, technological leadership, tourism appeal, and job creation.

The Public Investment Fund: Transformation Engine

At the operational center of Vision 2030 sits the Public Investment Fund, which has evolved from a peripheral fund into one of the world’s most active sovereign wealth vehicles. PIF assets exploded from $241 billion in 2016 to $941.3 billion in 2024, a 390% increase reflecting both capital deployment and reinvestment returns. The Fund’s 2030 target has been revised upward to $2.67 trillion, signaling confidence in execution. Critically, PIF now operates not as a passive allocator but as an active sector catalyst, directly investing in strategic industries, acquiring stakes in global companies (notably Electronics Arts at $55 billion), and driving localization in emerging sectors like gaming and clean energy. Saudi investment and industrial transformation 2026.

This capital concentration strategy differs markedly from decentralized private sector development. By channeling vast capital through a single sovereign vehicle, Saudi Arabia creates concentrated decision-making power and execution capability, though this approach also concentrates execution risk and creates potential market distortions in capital allocation.

Part 2: Progress Across Diversification Pillars

Sector Performance Overview

Vision 2030 Progress: 2024 Performance vs 2030 Targets

Tourism: Explosive Growth with Structural Momentum

Tourism represents Vision 2030’s most visible early success. Saudi Arabia achieved 116 million visitors in 2024, exceeding the baseline 2030 target of 100 million five years ahead of schedule. The 2030 target has been raised to 150 million annual visitors, driven by several reinforcing factors: the opening of the country to leisure tourism in 2019, aggressive visa reforms, infrastructure development (Riyadh Air launched in 2023), and mega-projects like NEOM and the Red Sea Project that position Saudi Arabia as a distinctive luxury destination.

Tourism spending surged 14% year-over-year to approximately SR 292 billion ($78 billion) in 2024, with the sector projected to grow 8% in 2025. However, the sector faces structural challenges: religious tourism (Hajj/Umrah) still dominates visitor volume and spending, accounting for roughly 50% of arrivals. Converting the remaining 50% into higher-margin leisure tourism requires sustained capital investment in hospitality infrastructure—the pipeline targets 252,000 hotel keys across all categories by 2030, with 64% in four- and five-star categories. Manufacturing constraint, not demand, now limits growth: hotel licensing increased 168% since 2019 as regulatory barriers fell, but construction execution remains a bottleneck.

Non-Oil Economic Growth: Core Engine of Diversification

Non-oil sectors expanded 4.3% in 2024 and 4.7% in Q4 2024, demonstrating resilience despite global headwinds and continued oil sector contraction (-4.5% in 2024). This decomposition is critical: Saudi Arabia’s overall 1.3% GDP growth masks a highly successful non-oil economy being dragged down by OPEC+ production cut extensions. The Q4 2024 acceleration to 4.5% year-over-year growth (highest in two years) suggests momentum is building as mega-projects reach operational phases.

Non-oil revenue reached $137.29 billion in 2024, representing 113% growth versus the 2016 baseline of $60 billion. Retail, hospitality, construction, and manufacturing led growth. The private sector’s contribution to GDP reached 47%, with a 2030 target of 65%—implying the need to create substantial new private-sector-led activities across currently underdeveloped sectors. Saudi investment and industrial transformation 2026.

Technology and Innovation: Building Competitive Advantage

Saudi Arabia Economic Transformation: 2016-2030 Performance and Projections

Saudi Arabia’s technology and innovation ecosystem represents the fastest-growing element of Vision 2030, though from a modest base. The sector’s contribution to GDP grew from 3.9% in 2019 to 5.3% in 2024, with a stated target of 13% by 2030. This dramatic acceleration reflects PIF’s $100+ billion commitment to tech and innovation, alongside institutional infrastructure investments including KAUST’s $10 billion R&D endowment and SDAIA’s AI governance and funding apparatus.

Startup activity has accelerated dramatically: approximately 2,000 active startups operate within Saudi Arabia, backed by over 140 support programs. Venture capital funding nearly tripled in recent years, with 2023 recording $1.38 billion in startup funding and $1.7 billion in AI-focused investments alone. Critically, Saudi Arabia captured nearly 50% of all MENA venture capital funding in 2023, up from less than 15% just five years prior—a structural shift that positions the Kingdom as the region’s primary innovation hub.

Key unicorn successes validate the ecosystem’s potential: Foodics (restaurant management software) and Sary (logistics) have achieved valuations exceeding $1 billion, demonstrating that Saudi-anchored ventures can compete at global scale. However, the startup ecosystem remains heavily dependent on government funding mechanisms (Monsha’at grants, KAUST partnerships, PIF investment) rather than organic angel and institutional venture capital—a structural dependency that may limit competitive intensity and innovation velocity.

Gaming and Entertainment: Strategic Cultural Pivot

Saudi Arabia’s gaming and esports sector generated $12 billion in revenue in 2024, representing 20% of MENA total revenue. This achievement is particularly notable given the sector’s nascent status just three years prior. The Savvy Gaming Group, PIF’s gaming subsidiary, has aggressively acquired global gaming assets—including stakes in Electronic Arts ($55 billion), Nintendo, Capcom, and Take-Two—positioning Saudi Arabia as a major player in the $180+ billion global interactive entertainment industry.

The Kingdom’s 2029 Esports World Cup, inaugurated in 2023 with $60 million in prize purses and 1,500 competitors, signaled Saudi Arabia’s ambition to become a hosting and production hub, not merely a consumer of entertainment. Targets are ambitious: 39,000 jobs and $13.3 billion GDP contribution by 2030. Yet success depends on overcoming cultural headwinds—gaming remains culturally controversial in parts of Saudi society—and on integrating global content expertise with domestic talent development.

Renewable Energy and Sustainability: Bridging Diversification and Decarbonization

Diversification Opportunity: Current State vs 2030 Targets by Sector

Saudi Arabia’s renewable energy strategy represents a critical convergence of economic diversification and climate commitment. The Kingdom targets 50% of electricity generation from renewables by 2030, a dramatic shift from just 2% renewable penetration in 2024 (4.7 GW of 86+ GW total installed capacity). This requires installing roughly 54 GW of new capacity in just five years—an extraordinary execution challenge.

Major projects are in advanced stages: ACWA Power and Saudi Aramco have signed long-term power purchase agreements for 15 GW of combined solar and wind capacity (12 GW solar, 3 GW wind) with $8.3 billion in investment and commissioning targeted for 2027-2028. Saudi Aramco independently plans 5.7 GW of solar capacity across five projects, generating enough clean energy to power approximately 1.5 million homes while displacing 8 million tons of annual carbon emissions. The NEOM Green Hydrogen project, a $5 billion public-private partnership between NEOM, ACWA Power, and Air Products, reached financial close in 2023 and represents the Kingdom’s deepest commitment to green energy innovation.

However, renewable energy expansion faces dual challenges: execution risk in deploying capital and technology at scale, and demand risk if Saudi Arabia’s own energy consumption growth (driven by population growth and giga-project electricity demands) absorbs new renewable capacity rather than enabling oil export increases. The latter constraint is particularly acute given Saudi Arabia’s reliance on oil export revenues to fund Vision 2030 investment.

Mining Sector: Third Economic Pillar

The mining sector embodies Vision 2030’s ambition to create entirely new economic pillars rather than merely optimize existing ones. Government strategy targets mining as the nation’s third economic pillar alongside oil and petrochemicals, with GDP contribution rising from approximately $17 billion in 2024 to $75 billion by 2030—a 4.4x expansion.

Saudi Arabia possesses substantial untapped mineral wealth estimated at $2.5 trillion, encompassing gold (495,000 ounces produced in 2024 with 10 million+ ounces in identified reserves), phosphate (concentrated in the Wa’ad Al-Shamal hub in Northern Borders Region), bauxite (integrated with aluminium processing at Ras Al-Khair), copper, lithium, and rare earth elements. Strategic partnerships are accelerating exploration and development: Ajlan & Bros-Moxico Resources partnership targets $14 billion in mining and processing investments by 2030, while Royal Road Minerals collaborates with Saudi MSB on copper and gold exploration.

The sector’s distinction lies in integration toward downstream processing and value-added manufacturing. Government targets $100 billion in downstream processing investments by 2035, with initiatives including battery chemistry complexes for EV manufacturing, steel mills for defense and shipbuilding, and copper processing facilities. This vertical integration strategy aims to transform raw material exports into finished goods, multiplying economic value and employment.

Part 3: Workforce Development and Labor Market Dynamics

Unemployment: Early Achievement with Structural Questions

Unemployment has fallen from 12.3% in 2016 to 7% in Q4 2024, achieving Vision 2030’s stated target six years ahead of schedule. This represents meaningful progress in absolute terms, particularly for a labor market that historically struggled with youth unemployment exceeding 27% and female unemployment above 33% in 2017. The achievement reflects both genuine job creation (driven by public sector hiring and mega-project employment) and demographic normalization as the youth bulge aged into working years.

However, beneath the headline figure lies persistent structural fragility. Saudi unemployment remains elevated relative to regional peers, and the composition matters critically: educated Saudis—particularly college graduates—face elevated joblessness, suggesting a supply-demand skill mismatch rather than pure job scarcity. The unemployment reduction achievement also reflects reduced labor force participation by Saudi citizens (with expatriate workers substituting), rather than genuine absorption of national labor supply into productive private sector employment.

Saudization: Economic Tradeoffs and Implementation Realities

Saudization—policies requiring employers to hire Saudi nationals at prescribed ratios—operates as Vision 2030’s social contract mechanism, ensuring that economic growth directly benefits Saudi citizens. The Nitaqat system, introduced in 2011 and continually refined, establishes sector-specific employment quotas. Government has complemented quotas with incentives: the Tawteen program offers financial bonuses to employers hiring Saudis at minimum salaries of SR 5,000 (approximately $1,330).

The policy has demonstrable employment impact: Saudi nationals now represent roughly 35-40% of private sector employment (up from 18.6% in 2017), with particularly strong progress in hospitality, retail, and construction. Female participation in the workforce more than doubled to 35.4%, driven partly by regulatory reforms that made women’s employment less complicated (removing guardianship restrictions for working women in 2019).

Yet Saudization carries substantial economic costs. Saudi workers command 30-50% wage premiums relative to expatriate workers in comparable roles, increasing employer costs. Additionally, Saudi workers exhibit lower tenure—employees frequently leave positions after 12-24 months, citing preference for government employment or better opportunities, creating high turnover costs for employers. These dynamics create a tension: Saudization advances social objectives (national employment, female participation) but increases private sector labor costs precisely when capital-intensive mega-projects require cost control.

Education and Skills Development: Lagging Execution

A critical constraint on Saudization success is the skills gap. While educational attainment has improved (the workforce is increasingly university-educated), the training pipeline remains misaligned with private sector needs. Graduates concentrate in fields like business and humanities, creating surpluses, while technical and vocational training in manufacturing, construction trades, and specialized services remains underdeveloped.

Government response has been multi-pronged: KAUST offers world-class STEM education with direct ties to R&D commercialization; SDAIA develops AI expertise; Monsha’at offers entrepreneurship and skill-building grants; and HRDF (Human Resources Development Fund) provides training subsidies. However, these initiatives remain supply-constrained relative to labor force growth. Saudi Arabia’s youth population continues expanding—59% of the population was under 30 in 2016—requiring continuous creation of productive opportunities to prevent unemployment re-acceleration.

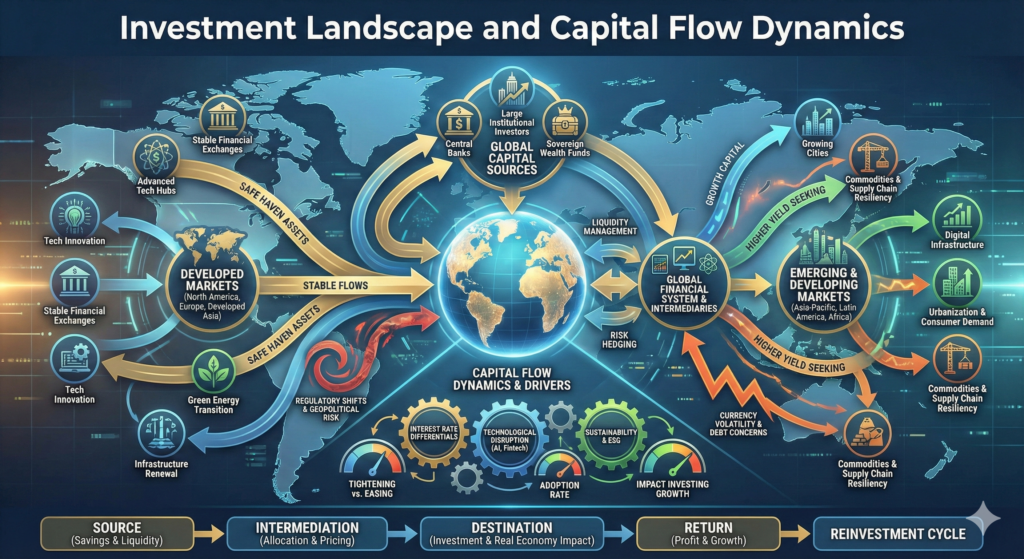

Part 4: Investment Landscape and Capital Flow Dynamics

Foreign Direct Investment: Progress Against Targets but Structural Gaps

Saudi Arabia Economic Transformation: 2016-2030 Performance and Projections

Foreign direct investment inflows reached SR 119 billion ($31.7 billion) in 2024, representing 24% growth from 2023 and exceeding the annual target of SR 109 billion for the fourth consecutive year. Manufacturing captured the largest share (29% of inflows, SR 35.12 billion), demonstrating FDI concentration in sectors with heavy capex and localization requirements.

However, FDI remains substantially below Vision 2030’s target of $100 billion annually by 2030. The Kingdom appears to be tracking at roughly $32 billion in 2024, implying a need to triple FDI inflows within six years. This gap reflects both global FDI slowdown (2024 saw global FDI decline) and structural constraints specific to Saudi Arabia:

- Regulatory Uncertainty: Frequent changes to investment regulations and licensing procedures create friction for multinational capital allocation decisions, which require multi-year ROI horizons and regulatory stability.

- Foreign Participation in Financial Markets: Foreign ownership of Saudi Arabian government debt remains minimal (under 2% of outstanding sukuk and bonds), limiting the equity investor base and signaling confidence gaps among global institutions.

- Sector Concentration: FDI concentrates in manufacturing, energy, and basic services rather than high-value sectors like technology, financial services, and advanced R&D—where margins are highest and knowledge transfer greatest.

- Capital Competition: Saudi Arabia competes for global capital against the UAE (which has advantages in financial services, trade hubs, and business continuity policies) and against developed economies offering larger scale, clearer IP protection, and deeper talent pools.

The government has responded through regulatory reforms: over 50,000 foreign investment licenses have been issued since Vision 2030’s launch, 660+ global companies have relocated regional headquarters to Saudi Arabia, and the Kingdom entered the World Bank’s top-10 in ease of doing business. Yet these metrics suggest process improvements rather than transformational capital attraction.

Sovereign Capital Deployment: PIF as Growth Catalyst

In the absence of sufficient foreign capital, PIF has become the primary growth catalyst. The Fund’s $56.8 billion in capital deployment across priority sectors during 2024 (cumulative $171 billion since 2021) dwarfs typical private capital rounds. This PIF-dominant capital model creates asymmetries:

- Execution Capacity: Large capital commitments enable mega-projects impossible through private markets (NEOM, Red Sea Project, Riyadh Metro). However, the concentration of capital and decision-making in a single sovereign fund reduces competitive intensity and may result in capital misallocation relative to market mechanisms.

- Financial Returns vs. Strategic Objectives: PIF operates simultaneously as a wealth fund (targeting financial returns) and a strategic development arm (targeting employment creation, diversification, and geopolitical positioning). These objectives can conflict—a profitable manufacturing plant in Germany may deliver better returns than a lower-margin domestic facility with high employment. The allocation of capital across these competing objectives remains opaque.

- Market Distortion: PIF’s participation in sectors like gaming, sports (majority ownership of Al Nassr FC), and entertainment raises questions about crowding-out private investment. When a sovereign fund commits $55 billion to acquire Electronic Arts, smaller venture investors face capital constraints and diminished returns.

Part 5: Competitive Positioning and Regional Dynamics

Saudi Arabia vs. UAE: Competing Visions in the GCC

The GCC’s largest economy competition between Saudi Arabia and the UAE shapes regional investment flows and policy competition. While both countries pursue diversification, their strategies diverge significantly: the UAE emphasizes becoming a regional trade and financial hub with openness to global capital and talent, while Saudi Arabia emphasizes domestic industrial base development, manufacturing capacity, and resource wealth integration.

In 2024, Saudi Arabia attracted $31.7 billion in FDI (highest capital investment among GCC nations), while the UAE led in project count (1,973 total FDI projects regionally). Saudi Arabia’s strategic advantage lies in capital scale (PIF $941 billion vs. Abu Dhabi Investment Authority $700+ billion), natural resource wealth, and domestic market size (35 million population). The UAE’s advantages include established financial hubs, more developed legal and business infrastructure, and perception as a politically stable neutral ground for global business.

This competition manifests across sectors: both countries are developing gaming ecosystems (Saudi Arabia through Savvy Games, UAE through established gaming companies); both are building mega-cities (Saudi Arabia’s NEOM, UAE’s Dubai and Abu Dhabi expansions); and both are attracting multinational regional headquarters. The 2021 Saudi decision to restrict GCC imports from tariff-free zones—a measure directly targeting UAE free zones—demonstrates the economic friction beneath diplomatic cooperation.

Saudi Arabia’s regional advantage consolidates if Vision 2030 succeeds in job creation and private sector development: the Kingdom’s larger labor force provides both consumer market scale and employment opportunity, potentially attracting capital seeking to establish regional manufacturing bases and emerging consumer-facing businesses. However, if Vision 2030 execution slips, the UAE’s more developed institutional infrastructure and global positioning may prove more resilient.

Global Positioning: BRICS Integration and Geopolitical Diversification

Saudi Arabia’s 2023 accession to BRICS (alongside UAE) represents a significant geopolitical reorientation complementing Vision 2030’s economic diversification. BRICS membership provides exposure to 40% of global population, creates preferential trade relationships and investment access, and signals non-Western alignment amid U.S.-China strategic competition. This geopolitical positioning matters directly for Vision 2030: integration with India, Brazil, and other emerging markets creates alternative capital sources and technology partnerships to supplement traditional Western investment and partnership.

However, BRICS integration also introduces geopolitical risks. Saudi Arabia’s traditional alliance with the United States creates potential friction if BRICS commitments diverge from U.S. preferences. The Kingdom’s balancing act—maintaining U.S. security partnerships while deepening BRICS relationships—reflects the fundamental uncertainty in global geopolitical ordering that creates both opportunity (alternative capital sources, technology partnerships) and risk (alliance instability, sanctions exposure) for Saudi Vision 2030.

Part 6: Fiscal Sustainability and Structural Risks

Debt Dynamics: Rising Leverage Against Diversification Timeline

Saudi Arabia Fiscal Sustainability: Path to Balanced Budget with Economic Diversification

National debt reached $319.7 billion in December 2024, representing 14% year-over-year growth and a debt-to-GDP ratio of 29.9%. While this ratio remains low relative to developed economies (U.S. 120%+, Japan 250%+), the trajectory reflects structural fiscal stress: oil prices declined from $75+ per barrel in 2023 to $60-65 by early 2026, straining government revenues that depend on oil for approximately 55% of fiscal receipts.

The IMF calculated Saudi Arabia’s breakeven oil price (the price at which the government runs neither deficit nor surplus) at $96.2 per barrel in 2024 and $84.7 per barrel in 2025. Current prices at $60-65 per barrel imply widening fiscal deficits even with aggressive non-oil revenue mobilization. The government projects a 2025 fiscal deficit of approximately 2.3% of GDP ($27 billion), with the IMF warning of potential 4% deficits if oil prices remain depressed.

Debt service is currently manageable (interest coverage ratios remain healthy), and net debt stands at 17% of GDP. However, the projection model is concerning: if oil prices remain above $84.7 per barrel (but below historical averages), debt-to-GDP could reach 46% by 2030—still moderate, but a sharp increase from current 29.9% and creating fiscal constraints for continued Vision 2030 mega-project investment at current scale.

To bridge the fiscal gap, the government and PIF have aggressively tapped capital markets. PIF raised $11 billion in 2025 through bond and sukuk issuances, while overall corporate debt issuance reached $47.9 billion in H1 2025. Sukuk and corporate bonds now total $465.8 billion outstanding, with sukuk representing 60.4% of the market.

The debt market structure reveals a critical risk: foreign participation in Saudi debt instruments remains minimal (under 2%), concentrating refinancing risk among domestic financial institutions. This domestic-heavy funding base becomes precarious if interest rates rise or confidence in diversification momentum falters. The government’s plan to issue $168 billion in sukuk and bonds between 2025-2029 will test market capacity and foreign appetite.

Oil Dependency Persistence: Structural Constraint

Despite nine years of diversification effort, oil and gas remain the economy’s foundation. Crude oil and natural gas contributed 22.3% of GDP in 2024, down from roughly 30-40% in the pre-2016 era, yet still the dominant sector. The non-oil sectors have grown rapidly (4.2% growth in 2024), but they are growing from a lower base: total non-oil GDP in 2024 was approximately $840 billion, while oil and natural gas GDP was $240+ billion.

This composition matters critically for fiscal dynamics. Oil revenues constitute 55% of government fiscal receipts, meaning each $10 per barrel movement in oil prices translates to approximately $18-20 billion annual fiscal impact. By contrast, non-oil taxes and fees (VAT, income tax, licensing fees) generate revenues more slowly. Vision 2030 targets non-oil revenues reaching $266 billion by 2030, up from $137 billion in 2024, but even this represents only 50% of total revenue assuming modest oil prices.

The implication is that Saudi Arabia remains in a medium-term structural dependency on oil prices, even as diversification progresses. This dependency creates a trade-off: Vision 2030 requires sustained capital investment (estimated at $1.2 trillion total through 2030), yet that investment must be financed partly from oil revenues that are volatile. Lower oil prices force either reduced Vision 2030 investment (executing delay) or increased borrowing (debt accumulation). Neither option is politically attractive.

Fiscal Sustainability Scenario Analysis

Three scenarios emerge for Saudi Arabia’s fiscal trajectory through 2030:

- Base Case ($70-80/barrel Brent): Non-oil diversification proceeds as planned, government runs modest deficits (2-3% of GDP), debt-to-GDP reaches 35-38% by 2030. Vision 2030 execution proceeds at planned pace with modest slippage. Fiscal sustainability achieved through combination of oil revenues, non-oil taxation growth, and debt issuance.

- Bull Case ($90-110/barrel): Higher oil revenues accelerate debt reduction and enable aggressive Vision 2030 investment. Non-oil revenue growth accelerates with positive sentiment. Debt-to-GDP stabilizes at 25-28%. This scenario was common 2010-2014 but appears increasingly unlikely given structural global oil market dynamics and EV transition timelines.

- Bear Case ($40-60/barrel): Sustained low oil prices force difficult fiscal choices. Government either significantly reduces Vision 2030 investment (mega-project delays, infrastructure spending cuts) or pursues aggressive borrowing/taxation/privatization. Debt-to-GDP rises sharply to 40-45%, potentially triggering sovereign rating downgrades and rising financing costs. Non-oil economic momentum slows as private investment capital responds to government spending reductions and higher interest rates.

Current base rates suggest the base case as most probable, with elevated downside risk if global recession or continued EV acceleration depresses oil demand further.

Part 7: Critical Success Factors and Implementation Challenges

Execution Risk: Megaproject Delivery at Scale

Vision 2030 Megaprojects: Investment Scale vs Projected Economic Impact

Saudi Arabia is simultaneously constructing $1.5 trillion in active projects—NEOM ($500B), Red Sea Project, ROSHN (400,000+ homes), Riyadh Metro expansion, King Salman International Airport, Qiddiya, and dozens of smaller initiatives. This level of concurrent capital deployment far exceeds historical construction capacity globally and creates substantial execution risk across multiple dimensions:

- Cost Overruns: Mega-projects typically experience 20-40% cost overruns. A 30% overrun on $1.5 trillion would add $450 billion to project costs—equivalent to three years of government revenues at current oil prices.

- Timeline Delays: Construction delays cascade through dependent projects. Riyadh Metro delays affect surrounding development velocity; airport delays constrain tourism growth; NEOM delays reduce early-stage technology hub benefits. Each year of delay increases opportunity cost and potentially reduces ROI.

- Supply Chain Constraints: Large-scale projects compete for materials, labor, and specialized equipment globally. The global construction equipment market has experienced shortages; skilled trades (welding, electrical work, specialized fabrication) are constrained in availability. Saudi Arabia is competing against UAE, Egypt, India, and other megaproject economies for scarce inputs.

- Workforce Skill Gaps: Executing projects at NEOM’s scale (33x NYC size) requires world-class project management, specialized engineers, and technical trades. While Saudi Arabia is developing local capacity through KAUST and vocational programs, substantial international talent importation remains necessary—creating dependency on foreign labor despite Saudization objectives.

- Regulatory Coordination: Mega-projects require seamless coordination across multiple government agencies (infrastructure, utilities, labor, environment, customs). Bureaucratic delays or unclear permitting pathways have historically constrained GCC mega-project velocity.

Private Sector Development: Capital Crowding and Competition Distortion

PIF’s dominant capital position creates a paradox for private sector development. While the Fund enables mega-projects impossible through private capital, its presence can crowd out private investment in sectors where PIF participates. Gaming exemplifies this dynamic: PIF’s $55 billion EA acquisition and substantial investments in global gaming properties may deter private venture capital from funding Saudi-based gaming startups (which face capital-constrained local competition).

Similarly, PIF’s direct investments in manufacturing, logistics, and energy sectors may reduce private capital incentives in these areas—when a sovereign wealth fund commits massive capital, private investors typically assume the state intends to maintain control and long-term involvement, reducing private competitive entry.

This crowding dynamic creates a structural risk: Vision 2030 success requires private sector contribution to rise from current 47% to 65% of GDP. Yet PIF’s preponderant capital role may prevent the market-driven competitive intensity needed to achieve private sector dynamism. The resolution requires explicit clarity on PIF’s exit strategies in sectors (e.g., divesting from profitable gaming properties to private investors, ceding manufacturing control to private manufacturers) that many observers question.

Regulatory Clarity and Institutional Maturity

Foreign investors and large private firms require predictable regulatory frameworks and institutional stability. Saudi Arabia has made substantial progress—over 50,000 investment licenses issued, streamlined permitting, and improved property rights protections. However, gaps remain:

- Permitting Timeline Clarity: Construction and operational permitting timelines remain uncertain for many project types, creating financing and planning challenges.

- Labor Law Predictability: Saudization quotas change periodically; labor standards evolve; enforcement is inconsistent across ministries. This creates hiring uncertainty for multinational employers.

- IP Protection: While Saudi Arabia signed the TRIPS agreement and established IP institutions, enforcement remains questioned by multinational tech companies and pharmaceutical firms concerned about counterfeit products and enforcement gaps.

- Transparency in Government Procurement: Government contracting and PIF-managed procurement follows established legal frameworks, but competitive bidding processes and award rationales are not always transparently published, creating perception of favoritism toward connected Saudi contractors.

These institutional gaps don’t prevent large-scale investment (as evidenced by ongoing FDI), but they increase cost of capital and reduce attractiveness versus other regional alternatives.

The Education-Employment Mismatch: Structural Labor Market Challenge

Perhaps Vision 2030’s deepest structural challenge lies in labor market dynamics. The Kingdom has dramatically increased university enrollment over the past 15 years, yet graduate unemployment remains elevated and employers report difficulty filling positions despite unemployed Saudi graduates. This skill mismatch reflects three root causes:

- Educational Specialization Mismatch: Graduates concentrate in business, humanities, and law, while manufacturing, construction, logistics, and technical services require specialized vocational training.

- Reservation Wage Effects: Saudi workers developed expectations of high public sector wages (often 3-5x private sector equivalents) during the oil boom. Private sector wages are insufficient to induce labor supply of educated Saudis for many roles.

- Job Quality Expectations: Saudi nationals aspire to white-collar, air-conditioned, low-physical-demand employment. Manufacturing, construction, hospitality, and other labor-intensive sectors struggle to attract Saudi applicants regardless of wages.

Addressing these structural mismatches requires multi-year educational reorientation (KAUST expansion, vocational training growth), expectation adjustment (through both wage normalization and cultural messaging), and potentially immigration policy adjustments (allowing higher-wage skilled foreigners) that conflict with Saudization objectives.

Part 8: Sector-Specific Deep Dives

Tourism: Infrastructure and Cultural Enablement

Tourism’s 116 million visitors in 2024 represents extraordinary progress, yet achievement conceals future challenges. The visitor composition remains heavily skewed toward religious tourism (Hajj, Umrah, Ziyarah visits to Shia sites)—perhaps 50-60% of arrivals. These visitors generate substantial spending (pilgrims spend significantly), but are relatively inelastic to discretionary attractions: they visit for religious purposes and concentrate spending in specific seasons (Hajj dates) and locations (Holy Cities).

Converting to leisure tourism growth requires differentiated strategies: heritage tourism (Diriyah, Madain Saleh), eco-tourism (Red Sea marine reserves, desert landscapes), adventure tourism (mountain activities, desert camping), and cultural experiences (music festivals, culinary experiences). The government is enabling these through mega-project development (NEOM as futuristic/tech showcase, Red Sea resorts as luxury eco-destinations), regulatory opening (women driving, cinema licensing, reduced religious police presence), and infrastructure investment.

However, leisure tourism faces structural constraints: Saudi Arabia remains perceived as culturally conservative and religiously restrictive relative to UAE, Egypt, or Oman—competing destinations for regional leisure tourists. Overcoming this perception requires consistent cultural opening (women’s rights expansion, religious enforcement reduction, LGBTQ+ inclusion) and time. Additionally, Saudi Arabia has limited beaches relative to UAE, limited historical ruins relative to Egypt, and limited recognized cultural brands in global tourism consciousness.

The 2029 Asian Winter Games and 2034 FIFA World Cup represent inflection points: successful hosting creates perception shifts and infrastructure legacies that amplify leisure tourism appeal. Conversely, execution failures (delays, cost overruns, poor operational execution) would damage international perception and reduce tourism inflows.

Renewable Energy: Ambitious Targets Against Execution Capacity

The 50% renewable energy target by 2030 represents 13-14 GW of annual capacity additions—a pace that has never been achieved in Saudi Arabia and equals the entire global average. This target is achievable technically (manufacturing capacity exists globally, technology is proven), but requires extraordinary capital discipline, supply chain execution, and regulatory coordination.

Current trajectory shows 4.7 GW operational (2024), with 8.3 billion in signed contracts for 15 additional GW (commissioning 2027-2028). This pipeline is sufficient to reach the 50% target if executed on schedule. However, delays are possible: supply chain disruptions, contractor bankruptcies, or permitting delays could push commissioning into 2029, narrowing renewable’s percentage contribution.

Additionally, achieving 50% renewable penetration without battery storage infrastructure creates grid stability challenges. Saudi Arabia has not yet built significant battery storage capacity, meaning renewable electricity variability (solar production peaks at midday, zero at night; wind varies seasonally) must be balanced through fossil fuel generation. Grid engineers indicate that 50% renewable penetration is technically manageable with Saudi Arabia’s existing natural gas and oil generation providing reserve capacity, but requires sophisticated demand management and real-time load balancing.

Mining: Greenfield Development Complexity

Mining sector development is the least mature of Vision 2030’s diversification pillars. The strategy requires transforming mineral exploration licenses into producing mines, then integrating mining output into downstream processing (battery chemicals, steel, aluminum) serving domestic manufacturing and export markets. This requires 8-12 years from initial exploration to commercial production at scale.

Current mining GDP contribution (~$17 billion) reflects largely historical production—Saudi Arabia’s gold mining dates back decades. New sources of growth (phosphate production at Wa’ad Al-Shamal, lithium exploration, copper development) are early stage. The risk is that first-mover international mining operators (Rio Tinto, BHP, Glencore) may exit or reduce commitment if project returns disappoint or Saudi operational/political risk increases. This would delay mining sector development and force reliance on smaller regional operators with less expertise and capital.

Successful mining development also depends on sustained commodity prices (gold $1,500-2,000+/oz, copper $4-5/lb, lithium $10-15k/ton). If commodity markets weaken mid-decade, investment returns disappoint, and mining sector momentum stalls.

Part 9: Investment Thesis and Recommendations

For International Investors: Risk-Return Dynamics

Saudi Arabia presents a “conviction bet” investment thesis rather than a “low-risk yield” option. The diversification vision is real, implementation progress measurable, and available capital massive. However, returns depend entirely on executing execution across multiple dimensions simultaneously.

Optimal investor positioning:

- Sector-specific thesis: Investors with expertise in specific sectors (tourism hospitality, automotive manufacturing, renewable energy engineering) can benefit from Saudi Arabia’s capital commitment and market growth. Sectors with demonstrated demand (tourism, gaming, tech startup ecosystems) carry lower execution risk than greenfield sectors (mining, advanced manufacturing).

- Partnership rather than pure equity: International firms benefit more from joint ventures and partnerships with Saudi entities (potentially PIF subsidiaries) than from pure external investment. These partnerships provide capital advantages, regulatory access, and market knowledge that overcome Saudi Arabia’s informational disadvantages for outsiders.

- Risk management: Investors should hedge against oil price and geopolitical shocks through diversified global portfolios. Saudi Arabia-specific exposure should be weighted based on risk tolerance and sector expertise.

For Saudi Policymakers: Critical Priorities for 2025-2030

- Fiscal Consolidation with Growth: The divergence between Vision 2030’s capital requirements ($1.2+ trillion) and available fiscal resources (government revenues ~$250 billion annually at current oil prices) requires either mega-project prioritization (focusing capital on highest-ROI initiatives) or aggressive private capital mobilization. Current execution attempts both simultaneously, creating financing stress.

- Private Sector Catalyzing: Non-oil GDP growth momentum (4.2%+ annually) is encouraging, but private sector contribution to GDP (47%) must accelerate to 65% by 2030. This requires explicit PIF exit strategies from competitive sectors, clearer regulatory predictability, and reduced government investment in sectors where private competition is viable (retail, hospitality, logistics).

- Labor Market Rebalancing: Saudization quotas have achieved employment objectives but at productivity cost. Calibration should shift toward skills-based hiring (merit within Saudi employment frameworks) rather than fixed quotas, reducing wage premiums and improving competitive positioning.

- Education Pipeline Acceleration: Vocational training expansion (STEM, construction trades, logistics management) must be prioritized through curriculum reform, instructor training, and employer partnerships. The current approach—expanding university enrollment—is misaligned with labor market demands.

- Geopolitical Hedging: Diversification strategy should include explicit hedges against oil price weakness through (a) non-oil revenue growth acceleration, (b) sovereign wealth fund return enhancement, and (c) foreign capital attraction (requiring regulatory clarity improvements).

Conclusion: Transformation in Progress, Success Not Guaranteed

Saudi Arabia’s Vision 2030 represents one of the most ambitious economic transformation programs globally—rivaling historical programs like South Korea’s industrialization, UAE’s diversification, or Singapore’s economic pivot. Nine years of implementation demonstrate both genuine progress and persistent challenges.

Achievements are substantial:

- Non-oil GDP growth accelerating (4.2-4.7% annually)

- Employment targets achieved ahead of schedule (7% unemployment by 2024, target not until 2030)

- Tourism explosive growth (116 million visitors, nearly 2x pre-Vision baseline)

- Technology ecosystem emergence ($5.3% of GDP, targeting 13%)

- Mega-project pipeline operational (NEOM construction, Red Sea resorts, Riyadh Metro execution)

- Capital mobilization unprecedented ($940+ billion PIF assets, $1.2 trillion Vision investment)

Critical risks persist:

- Fiscal sustainability dependent on oil prices above $85/barrel, with current prices at $60-65

- Foreign direct investment significantly below $100 billion annual target

- Private sector development lagging (47% of GDP target, 65% goal by 2030)

- Labor market structural mismatches (education-employment disconnect, wage expectations, Saudization costs)

- Mega-project execution risk at $1.5 trillion scale simultaneously

- Geopolitical uncertainty (U.S.-Saudi tensions, Iran dynamics, regional conflicts)

The verdict at the midpoint of Vision 2030 is neither triumph nor failure, but promising progress against a difficult strategic challenge. If the Kingdom can navigate the fiscal constraints (perhaps through higher oil prices, accelerated non-oil revenue growth, or successful private capital mobilization), it stands to achieve a genuinely diversified economy with reduced oil dependency by 2035-2040.

However, if oil prices remain depressed, execution delays mount, or private sector engagement disappoints, the vision could decelerate into slower, more modest diversification that reduces oil dependency but does not achieve the transformational ambitions articulated. In either case, Saudi Arabia’s economic trajectory over the next five years will substantially reshape regional power dynamics, investment flows, and geopolitical positioning across the Middle East and beyond.

official Vietnamese government websites

| Ministry of Finance | Ministry of Finance |

| Ministry of Economy & Planning | Ministry of Economy & Planning |

| Ministry of Commerce | Ministry of Commerce |

| Ministry of Health | Ministry of Health |

| Ministry of Interior | Ministry of Interior |

Read more country case studies done before this.

| china | china |

| hong kong | hong kong |

| japan | japan |

| sinagpore | singapore |

| taiwan | taiwan |

| uAE | UAE |

| india | india |

| south korea | south korea |