Kuwait’s

Kuwait non-oil economy growth 2026.

Executive Summary

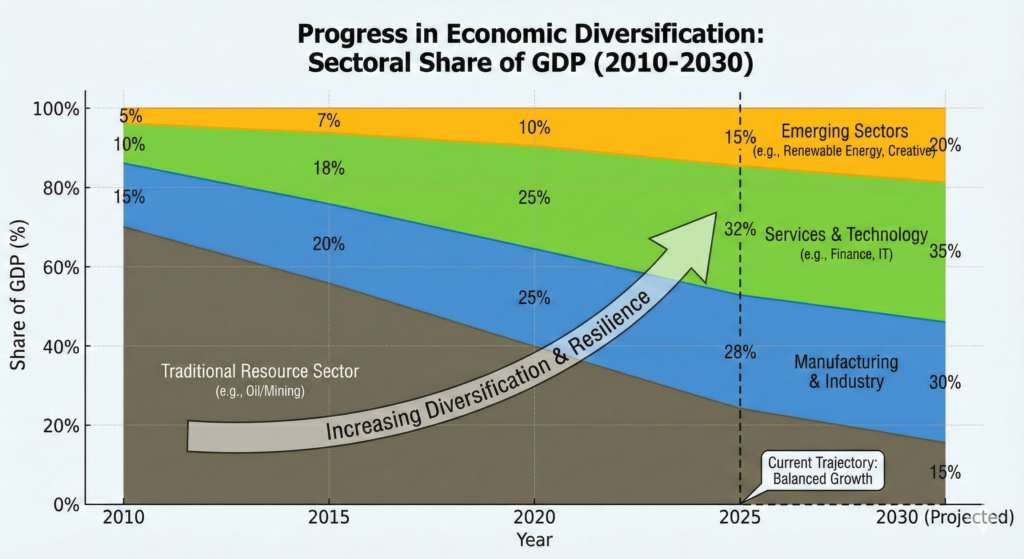

Kuwait stands at a pivotal inflection point in its economic transformation. The country has transitioned from an oil-dominated economy (90% of exports, 90% of government revenue) to a more balanced structure where the non-oil sector now comprises 56.6% of GDP—a meaningful shift underpinning Vision 2035’s diversification agenda. Yet this structural transition masks significant implementation challenges, volatility in foreign investment inflows, and persistent institutional barriers that threaten the pace and sustainability of diversification.

The 2024 economic contraction (-2.9% real GDP, driven by OPEC+ production cuts) and subsequent 2025 recovery (2.6% forecast) underscore Kuwait’s vulnerability to external commodity shocks and the urgent need to accelerate non-oil sector resilience. While construction, telecommunications, real estate, and financial services are emerging as growth drivers, success hinges on fundamental reforms to governance, labor market incentives, private sector competitiveness, and human capital development—dimensions where Kuwait lags regional and global peers despite high per-capita income.

Kuwait’s Economic Diversification: Multi-Dimensional Progress Across Oil Dependency, Sectoral Growth, Foreign Investment, and Renewable Energy Transition

Part I: Macroeconomic Foundations and Oil Dependency

Persistent Oil Reliance and Fiscal Pressures

Despite decade-long diversification efforts, Kuwait’s economic structure remains fundamentally extractive. Oil revenues account for 90% of government revenue and 90% of exports, with the oil sector representing 43.4% of GDP as of 2024. Current account surpluses (29.1% of GDP in 2024, moderating to 26.5% in 2025) are driven primarily by hydrocarbon exports, not economic diversification. This creates a precarious situation: lower oil prices (IMF assumes $60/bbl medium-term, down from $70/bbl assumptions) threaten fiscal sustainability and constrain the government’s capacity to fund diversification projects themselves.

The fiscal position exemplifies this vulnerability. Kuwait’s fiscal deficit is projected to widen to 7.8% of GDP in FY2025/26 (from 2.2% in FY2024/25) due to lower oil revenues despite non-oil sector growth of 2.7%. Over the past decade, persistent deficits have depleted the General Reserve Fund (GRF)—Kuwait’s crucial liquidity buffer—from $193 billion (FY2014/15) to near-terminal depletion. The government’s largest expenditure items remain wages (public sector payroll), subsidies, and transfers, collectively consuming 80% of total spending, versus averaging 9.9% in peer G7 economies.

This expenditure structure reflects a fundamental challenge: the social contract guaranteeing near-universal public sector employment for Kuwaiti nationals (74% of the labor force) creates structural fiscal rigidity. The public sector wage bill is the highest in the GCC at 2 times the regional average, consuming 19% of GDP versus typical OECD levels of 5-12%. Unless this social contract is materially reformed, the government’s fiscal capacity to invest in strategic diversification initiatives remains constrained, and fiscal sustainability will require either dramatic revenue increases (unlikely given oil market dynamics) or profound spending restructuring (politically difficult).

Mitigating this constraint is Kuwait’s exceptionally strong sovereign wealth position. The Kuwait Investment Authority (KIA), founded in 1953 as the world’s oldest sovereign wealth fund, manages $1.029 trillion in assets (March 2025), ranking fifth globally and representing 534% of GDP in liquid assets over 2025-2028. This provides a multi-decade buffer for government operations and enables counter-cyclical investment in diversification. However, KIA’s assets are increasingly viewed as emergency reserves rather than active engines of economic transformation—a structural inefficiency given the fund’s potential to directly catalyze non-oil growth through strategic investments in targeted sectors.

Part II:kuwait Progress in Economic Diversification

Non-Oil Sector Expansion and Sectoral Dynamics

The non-oil economy expanded 3.1% year-over-year in Q2 2025, representing the fourth consecutive quarter of positive annual gains and a notable acceleration from 2% recorded in Q1 2025. This growth, however, masks significant sectoral unevenness and underlying fragility:

Construction (12.6% YoY) leads non-oil growth, driven almost entirely by government mega-projects: Silk City (Madinat Al-Hareer), the Sheikh Jaber Al-Ahmad Al-Sabah Causeway, Mubarak Al-Kabeer Port, and new housing cities. These projects remain critically dependent on government budget allocations and Chinese consortium partnerships (particularly China Communications Construction Company), not on organic private sector dynamism or foreign commercial investment. Once these projects complete, construction sector growth will face structural headwinds.

Telecommunications (8.0% YoY) benefits from ongoing 5G rollout and digital infrastructure investment aligned with Vision 2035 digital transformation targets. The ICT market was valued at $22.48 billion in 2023 and is projected to reach $39.83 billion by 2029. This sector demonstrates the scalability potential of market-driven non-oil activities, yet growth remains constrained by regulatory frameworks and the need for greater private sector competition.

Real Estate (7.2% YoY) expansion reflects demand from population growth and infrastructure development, though price softening (particularly in residential) suggests potential oversupply in certain segments. Private hospital bed expansion from ~1,000 to 2,800 beds is driving healthcare real estate demand.

Financial Intermediation and Insurance (1.9% YoY) growth significantly lags the historical Islamic banking sector momentum, reflecting both a high base (Islamic banking assets already comprise 50% of total banking sector assets) and subdued private sector credit conditions (5.5% credit growth in May 2025, despite “healthy” levels).

Collectively, these growth rates, while positive, mask a troubling reality: non-oil growth is concentrated in government-directed sectors (construction, infrastructure) and defensive services (healthcare, education), not in globally competitive, productivity-enhancing activities like manufacturing, advanced services, or technology. The IMF forecasts non-oil growth will stabilize at 2.7% medium-term—below the 3-4% growth rates needed to generate meaningful employment for an expanding labor force and reduce public sector dependency.

Key Opportunity Sectors

Financial Services and Islamic Finance: Kuwait hosts the world’s second-largest Islamic bank (Kuwait Finance House, with $120.6 billion in assets as of Q3 2023), and Islamic banking now represents 50% of total banking sector assets, up from 45.5% in H1 2022. Islamic banking is growing at 12% annually and is projected to reach $27 billion in assets. The Central Bank of Kuwait has issued sustainable finance and ESG guidelines, positioning Kuwait to capitalize on the global expansion of Islamic finance (projected to reach $5 trillion by 2025). However, capital markets development lags peers: foreign participation in Kuwait Stock Exchange trading stood at 7.8% of activity in 2024, up from 5.8% in 2021—suggestive of growing but still modest international investor engagement.

Capital markets reforms launched in 2025 include introduction of central counterparty clearing frameworks, digital infrastructure for ETFs and fixed-income instruments (sukuk and bonds), and sub-account numbering for transparency. These reforms are positioning Kuwait to leverage Islamic finance as a genuine regional competitive advantage, but execution risk remains high given the need for legislative implementation and international regulatory alignment.

Digital Transformation and Technology: The fintech market is projected to reach $9.5 billion by 2026. The Central Bank of Kuwait has implemented a Regulatory Sandbox Framework (similar to UAE and Bahrain’s models) to encourage fintech adoption, and digital government services are being expanded. However, fintech regulation remains slower than in regional competitors, reflecting institutional capacity gaps and conservative regulatory posture.

Healthcare and Medical Tourism: Kuwait’s healthcare sector is undergoing significant digital transformation (detailed below), with private hospital bed expansion and adoption of AI-enabled diagnostics, electronic health records, and telemedicine. However, the sector remains heavily dependent on expatriate specialists and faces regulatory constraints around private insurance coverage (only a small percentage of the population is covered by private insurance, focusing on high-risk elderly populations).

Logistics and Trade Hub Development: The Mubarak Al-Kabeer Port, part of Silk City Phase 1 ($86 billion investment, 25-year development), is expected to contribute $35 billion annually to GDP once operational. However, the port faces construction delays and execution risks. Agility Logistics, a Kuwaiti multinational, demonstrates the sector’s potential, yet remains an outlier in the Kuwaiti private sector landscape.

Part III: kuwait Mega-Projects and Infrastructure as Diversification Engine

Silk City (Madinat Al-Hareer): Ambitions and Execution Reality

Silk City is Kuwait’s marquee diversification project—a $86-132 billion, 25-year urban development anchored on Boubyan Island in northern Kuwait. The project envisions:

- Mubarak Al-Kabeer Port: Multi-berth deep-water port serving as a regional trade hub (currently under construction, first phase partially complete)

- Sheikh Jaber Al-Ahmad Al-Sabah Causeway: $3 billion causeway connecting northern Kuwait to Kuwait City (completed 2019, operational)

- Burj Mubarak Al-Kabir Tower: Planned 1,001-meter tower surpassing Burj Khalifa

- Free Trade Zone and Logistics Hub: Supporting SME incubation and international commerce

- Residential, Commercial, and Mixed-Use Districts: Targeting 25,000 residents and regional connectivity

- International Airport and Rail Network: Expected to enhance regional connectivity (early phases)

Progress and Challenges: In December 2025, Kuwait signed an engineering, procurement, and construction (EPC) contract with China Communications Construction Company (CCCC) for Phase 1 of Mubarak Al-Kabeer Port, signaling acceleration. However, the project has experienced repeated delays since conception in the early 2010s. Execution risks include: Kuwait non-oil economy growth 2026.

- Chinese Dependency: Reliance on Chinese financing, construction expertise, and operational models raises concerns about long-term sustainability, technology transfer, and alignment with global standards.

- Fiscal Sustainability: The $86 billion Phase 1 cost is substantial; full project financing depends on sustained government budgets and private sector participation—both currently constrained.

- Market Absorption: Projected economic contributions ($35 billion annual GDP once operational) depend on achieving critical mass of trade volume, tenant occupancy, and regional market share—uncertain given competition from UAE and Saudi ports.

- Timeline Realism: A 25-year phased development, even with acceleration, suggests material contributions will be backloaded beyond 2035 Vision targets.

Despite these risks, Silk City remains strategically important: if executed successfully, it positions Kuwait as a regional logistics and trade hub, reducing economic reliance on oil and complementing financial services diversification.

Other Infrastructure: Airport Expansion, Housing, Utilities

Kuwait International Airport expansion ($2 billion project) is underway to increase capacity and modernize facilities, supporting tourism and business travel. New housing cities (South Al-Mutlaa, other planned developments) are being constructed to address housing demand and support construction sector employment. Water and electricity projects are expanding capacity to support growing demand, though these remain subsidized commodities (electricity and water are heavily subsidized, reducing revenue potential and incentive for efficiency).

Part IV: Sectoral Deep-Dives

Healthcare and Digital Innovation

Kuwait’s healthcare sector is a bright spot in digital transformation efforts. Major initiatives include:

- Electronic Health Records (EHR): Royale Hayat Hospital has implemented InterSystems’ Trakcare EHR system with mobile applications. AI is being deployed in surgical guidance, 3D organ visualization, and diagnostic support (e.g., Jaber Hospital’s AI-assisted surgeries and endoscopy).

- Telemedicine and Digital Health: Post-COVID normalization has retained telemedicine adoption; Kuwait Hospital’s 2025 partnership with SAP to deploy cloud-based solutions and real-time analytics exemplifies sector modernization.

- Efficiency Gains: Digital-first hospitals report 50-60% reduction in wait times and 15% cost reductions with 20% higher patient satisfaction scores.

- Infrastructure Expansion: Private hospitals are expanding bed capacity from ~1,000 to 2,800 beds by 2025-2026, driving real estate development and employment.

Constraints: Private health insurance coverage remains limited (primarily high-risk elderly populations), limiting consumer demand for premium private services. Regulatory clarity on insurance coverage, data privacy, and cross-institutional data sharing remains fragmented. However, Kuwait Health Ministry and private hospital partnerships are gradually improving coordination.

Opportunity: With aging demographics and rising non-communicable disease burden (76.5% of deaths attributed to NCDs), healthcare represents a structurally growing sector aligned with Vision 2035’s human capital pillar. Digital innovation is enabling cost management and quality improvement—prerequisites for sustainable sector expansion.

kuwait Financial Services: Islamic Banking and Capital Markets

Islamic Banking: Kuwait Finance House (KFH), the world’s second-largest Islamic bank, exemplifies the sector’s scale and global integration. Islamic banking assets grew to 50% of total banking sector assets by H1 2023, up from 45.5% in H1 2022, indicating accelerating market share capture. Islamic fintech is projected to reach $9.5 billion by 2026.

Green Islamic finance is emerging as a growth vector: the Central Bank of Kuwait issued sustainable finance guidelines in November 2022, and the Capital Markets Authority issued green sukuk guidelines in February 2022. This positions Kuwait to capture Islamic finance flows seeking ESG-compliant investments, particularly as global Islamic finance market is estimated to reach $5 trillion by 2025.

Capital Markets Development: In 2025, the Capital Markets Authority launched reforms including central counterparty clearing frameworks, digital infrastructure for ETFs and sukuk, and enhanced transparency mechanisms. Foreign participation in Kuwait Stock Exchange trading reached 7.8% of activity in 2024 (up from 5.8% in 2021), indicating growing international investor interest, though foreign investor base remains small. The stock exchange processed 69 million share trades in 2024, ranking it among GCC’s most active markets—a positive signal for market development.

Challenges: IPO activity in Kuwait remains subdued compared to regional peers (Saudi Arabia, UAE, Qatar experiencing IPO waves). Market depth remains limited, with retail investor participation concentrated among locals. Regulatory frameworks for alternative assets (private equity, private credit) are nascent. However, the 2025 capital markets reforms are beginning to address these gaps.

Part V: Foreign Direct Investment and Private Sector Competitiveness

FDI Volatility and Sectoral Composition

Kuwait’s FDI trajectory reflects volatile external conditions rather than structural private sector attractiveness:

- 2023: FDI inflows nearly tripled to $2.113 billion (up from $758M in 2022), suggesting response to Vision 2035 reforms and infrastructure project visibility.

- 2024: FDI inflows declined sharply to $614 million, suggesting caution amid economic contraction and lower oil prices.

- FDI Stock: Estimated at $16.648 billion (2023), indicating a modest cumulative foreign investment base.

Sectoral composition reveals the pattern: bulk of FDI flows to oil & gas (government-directed), real estate/construction (mega-projects), and financial services. Non-extractive, tradable-sector FDI remains underdeveloped. Greenfield investments averaged 22 projects in 2024, a reasonable level but below what would be expected for a high-income economy pursuing regional financial hub status.

Business Environment and Regulatory Reforms

Kuwait has undertaken significant business environment reforms in 2024-2025:

- 100% Foreign Ownership: New FDI Law allows wholly foreign-owned entities in technology, ICT, manufacturing, logistics, healthcare, pharmaceuticals, education, and renewable energy sectors—a dramatic liberalization from the previous 51% Kuwaiti ownership requirement.

- Digital Business Services: The Kuwait Business Center now enables company registration within 3-5 business days, with online licensing and real-time application tracking.

- Tax Reforms: Implementation of 15% corporate tax on foreign multinational enterprises with revenues >$750M (targeting ~300 companies, raising ~$825M annually) aligns Kuwait with OECD Pillar Two global minimum tax standards.

- Legislative Modernization: New laws include:

- Decree-Law 60 of 2025 (Financing and Liquidity): Establishes public debt ceiling of KD30 billion, enables financial instrument issuance up to 50 years.

- Digital Commerce Law: Comprehensive regulation of e-commerce (2025).

- Real Estate Developer Law: Streamlines residential and commercial real estate transactions.

- Anti-money Laundering Amendments: Criminalization of alternative remittance systems.

- Capital Markets Reforms: Central counterparty clearing, digital infrastructure for bonds/sukuk/ETFs, and transparency enhancements (2025).

- Foreign Branch Offices: As of January 2024, foreign companies can establish wholly owned branches without local agents—eliminating previous dependency on local representatives.

Impact: These reforms are moving Kuwait’s business environment in the right direction, though global competitiveness rankings remain modest:

- Global Innovation Index: 71st (2024)

- Index of Economic Freedom: 88th (2024)

- Ease of Doing Business: 71st (2024, though trending upward)

The trajectory is improving, but Kuwait remains below peer expectations for a high-income financial hub.

Part VI: Labor Markets and Human Capital

The Kuwaitization Paradox and Public Sector Dominance

Kuwait faces a fundamental labor market paradox: the social contract guaranteeing public sector employment for all nationals has created a 74% public sector employment rate among Kuwaitis—extraordinarily high compared to OECD countries (typically 15-25%). This generates multiple distortions:

- Disincentive for Private Sector Participation: Public sector jobs offer greater security, shorter working hours, generous benefits, and less demanding responsibilities. Consequently, private sector employment among Kuwaitis remains marginal (~30% of Kuwaiti workforce, with 70% of private sector positions held by expatriates).

- Skills Mismatch: Education outcomes are misaligned with labor market needs. Students preferentially pursue humanities and social sciences (targeting guaranteed public sector jobs) rather than STEM disciplines (required in knowledge-economy and manufacturing roles). Only ~30% of university graduates pursue STEM fields, versus demand requirements of 50%+.

- Human Capital Deficits: The World Bank’s Human Capital Index ranks Kuwait 77th out of 157 countries—low for a high-income nation. Children in Kuwait are projected to be only 56% as productive when grown as they could be if they had complete education and full health. Key metrics:

- Preprimary enrollment: 62% (vs. 83% OECD average)

- By age 10, >50% of children cannot read age-appropriate text.

- Lost years of schooling: 4.6 years (learning-adjusted schooling is 7.4 vs. 12-year target)

- Female Labor Force Participation: At 31%, female participation significantly lags male (48%) and global peers. Female youth unemployment (37%) is particularly acute, reflecting occupational segregation and social norms around childcare responsibilities (63% of women cite childcare as a barrier to work).

Reforms Underway

The National Jobs Strategy (in development) and KNDP-3 human capital pillar include:

- Curriculum Reform: Modern curriculum aligned to international standards (grades 1-4, 6-8) to improve critical thinking and problem-solving.

- National Manpower Development Centre: Providing training and skills development for 30,000+ nationals, targeting two-thirds of the labor force for private sector employment.

- Teacher Quality: Professional licensing system for educators, continuous professional development, and selective hiring of foreign teachers (4,500 renewed at 2-year permits; 1,000 new local teachers being hired).

- Kuwaitization Strategy: Attempts to shift private sector Kuwaitization (increasing Kuwaiti employment) while maintaining competitiveness—a delicate balance, as mandated Kuwaitization without corresponding skill development creates wage inflation and reduces private sector profitability.

- Vocational Training: Expansion of technical and vocational institutes to provide practical, job-market-aligned skills.

Progress and Challenges: While reforms are advancing, measurable outcomes remain limited. The cultural preference for public sector employment persists, subsidized public sector wages continue to undercut private sector wage competitiveness, and education quality gaps remain significant. Sustainable change will require multi-year commitment, political willingness to reduce public sector employment, and credible private sector wage and benefit competitiveness—all challenging in Kuwait’s rentier political economy.

Part VII: Energy Transition and Renewable Energy

Current State and Strategic Goals

Kuwait’s renewable energy ambitions are structurally challenged by geography, demographics, and existing energy infrastructure:

- Current Renewable Capacity: <1% of electricity generation (approximately 50 MW solar)

- 2030 Target: 15% renewable energy share (likely to be missed)

- Realistic 2035 Milestone: 11-15% renewable share

Rystad Energy’s analysis suggests Kuwait will achieve only 3.3 GW of renewable capacity by 2030 (7% of generation), falling short of the 15% target. By 2035, renewable capacity is forecast to reach 11 GW, supporting ~20% of electricity generation—closer to realistic targets.

Solar Capacity Trajectory:

- 2025: 50 MW (current)

- 2029: 1.0 GW (forecast)

- 2030: 2.9 GW (forecast)

- 2035: 10.1 GW (forecast)

Enablers: Kuwait benefits from 3,300+ hours of annual sunlight and PV output potential of 4.6-4.9 kWh/kWp/day—excellent conditions for solar deployment. The Shagaya Renewable Energy Park tender (1.1 GW capacity) has attracted six prequalified bidders, indicating competitive interest.

Constraints:

- Regulatory streamlining needed (single-window clearance system for approvals)

- Grid infrastructure upgrades required to handle solar variability

- Energy storage and smart grid investments necessary

- Subsidy structure (electricity heavily subsidized at low consumer prices) dampens private investment incentives

- Net metering policy lacking clarity, reducing residential/commercial solar adoption

Transitional Strategy: Natural gas serves as the transition fuel. Kuwait plans five new large-scale gas-fired power plants (adding 18 GW capacity, bringing total to 32 GW by 2035) and has signed a 15-year LNG agreement with QatarEnergy (3 million tonnes annually). This shift reduces oil consumption in power generation (currently 40%) and frees crude for export—preserving fiscal revenues while gradually increasing renewable energy share.

Assessment: Kuwait’s renewable energy transition is proceeding at realistic pace, even if below aspirational 2030 targets. The strategy appropriately prioritizes reliability and export preservation over aggressive renewable deployment that could destabilize the grid or reduce fiscal revenues. However, energy efficiency and demand-side management receive insufficient policy attention—complementary strategies that could reduce absolute electricity demand and accelerate renewable economics.

Part VIII: Tourism and Hospitality Development

Market Opportunity and Strategic Positioning

Kuwait is positioning tourism as a diversification lever, with significant growth forecasts:

- Revenue Projection (2021-2025): From $522 million to $1.13 billion (21.34% compound annual growth rate)

- Hotel Development: ~8,400 new rooms expected, expanding from ~1,000 to 2,800+ private hospital beds also driving hospitality infrastructure demand

- Mega-Projects: Silk City includes tourism facilities; Failaka Island ($3.3 billion) has tourism components; Winter Wonderland, Al-Sabahiya Park, and Shatea Alblajat beach developments are underway

- Airport Expansion: Kuwait International Airport capacity expansion (from 13 million to 50 million passenger capacity potential) will support tourism growth

- Regional Positioning: Kuwait is aligning with the broader Gulf Tourism Strategy 2023-2030, positioning itself within a regional network

Current State and Challenges

Tourism in Kuwait remains underdeveloped relative to regional peers (UAE, Saudi Arabia, Qatar). Historical barriers include:

- Political Perception: Tourism was historically viewed with cultural ambivalence; recent reforms signal changed attitudes toward tourism’s economic role.

- Market Composition: Historically dominated by business travelers (largely tied to US military operations in Iraq and energy sector). Leisure tourism remains nascent.

- Infrastructure Gaps: Limited world-class hospitality, entertainment, and cultural attractions relative to Dubai, Riyadh, or Doha.

- Regulatory Constraints: Visa processes and tourism regulations remain less liberal than competitors.

Growth Drivers

Recent policy shifts and mega-projects are catalyzing sector development:

- Government Commitment: Tourism sector expansion is explicitly linked to Vision 2035 diversification and job creation (both Kuwaiti and expatriate employment).

- Public-Private Partnerships: Government is actively partnering with private hospitality operators to develop hotels, resorts, and entertainment venues.

- Event Management: Successful Gulf Cup hosting (150,000+ visitors) demonstrates Kuwait’s capacity to attract and manage large-scale events.

- Entertainment and Leisure: New parks, beaches, and entertainment complexes are expanding the tourist offer.

Assessment: Tourism represents a meaningful diversification opportunity—potentially contributing $2-3 billion annually to GDP by 2035 if development trajectory holds. However, current activity remains modest, and success depends on sustained government support, private sector capital allocation, and improved international marketing. Regional competition from Saudi Arabia’s Vision 2030 (investing heavily in tourism infrastructure and entertainment) and UAE’s established brand as a premium destination creates headwinds.

Part IX: Digital Transformation and the Knowledge Economy

ICT Sector Growth and Vision 2035 Alignment

The ICT market is one of Kuwait’s most dynamic diversification vectors:

- Market Size (2023): $22.48 billion

- Projected Size (2029): $39.83 billion

- Growth Rate: ~10% annually (well above broader non-oil GDP growth)

Key Initiatives:

- 5G Rollout: Telecommunications operators (particularly STC Kuwait, with strategic partnerships with Thales and Google Cloud) are advancing 5G networks, enabling smart city applications and digital service delivery.

- Digital Government Services: Kuwait is transitioning toward e-governance, with the Kuwait Business Center providing digital licensing and permit processes.

- Smart City Integration: Infrastructure investments in Silk City and other new developments include smart city technologies (IoT, AI-enabled services, digital platforms).

- Fintech Sandbox: Central Bank of Kuwait’s Regulatory Sandbox Framework encourages fintech innovation in digital payments, lending, and asset management.

E-Commerce and Digital Commerce Law

A 2025 Digital Commerce Law provides comprehensive regulation for online transactions, balancing economic freedom with consumer and data protection. This creates a legal framework for e-commerce platforms, digital marketplaces, and direct-to-consumer businesses—supporting entrepreneurs and private sector digitalization.

Challenges and Opportunities

- Regulatory Maturity: While progress is evident, fintech regulation remains less developed than in UAE or Bahrain—creating a window for Kuwait to leapfrog with comprehensive, balanced regulatory frameworks.

- Skilled Workforce: Technology sector growth is constrained by limited STEM-trained graduates; upskilling existing workforce is critical.

- Infrastructure Investment: Continued investment in broadband, data centers, and cloud infrastructure is required to support sector growth.

- Startup Ecosystem: Government support for startups (through SME development funds, incubators, and venture capital facilitation) is emerging but remains less mature than regional peers.

Assessment: The ICT and digital transformation sector is positioning Kuwait as a regional technology hub, complementing financial services and logistics diversification. Success requires sustained investment in human capital (STEM education), regulatory modernization, and private sector incentivization.

Part X: Constraints, Risks, and Structural Barriers

Institutional and Governance Constraints

- Public Sector Inefficiency and Bureaucratic Inertia: Large public sector employment (74% of Kuwaiti workforce) creates institutional inertia. Decision-making processes are slow; coordination across ministries is fragmented. Administrative procedures for permitting, licensing, and procurement remain cumbersome despite digital reforms—with actual approval times often exceeding official timelines.

- Corruption and Monopolization: Academic analysis identifies corporate governance weaknesses, limited competition enforcement, and corruption as significant barriers to private sector growth. The Competition Protection Authority, while mandated, faces capacity and political constraints in challenging entrenched business interests.

- Social Contract Rigidity: The guaranteed public sector employment and subsidy system creates fiscal inertia. Reforming this requires political consensus that has been difficult to achieve despite fiscal pressures.

- Parliamentary Dysfunction: Kuwait’s Parliament has historically blocked or delayed fiscal and economic reforms. Recent temporary suspensions of parliamentary activities (2024-2025) have enabled some executive reforms (e.g., tax implementation, real estate transparency measures), but long-term sustainability requires legislative support.

Macroeconomic and Fiscal Risks

- Oil Price Vulnerability: Medium-term IMF assumptions of $60/bbl (down from historical $70/bbl) imply sustained fiscal stress. Any further decline would accelerate GRF depletion and force either austerity (politically difficult) or asset sales (limiting long-term fiscal buffers).

- Current Account Dependency: Current account surpluses (21% of GDP medium-term) depend entirely on oil export revenues. Economic diversification has not yet generated sustainable non-oil export sectors or created sufficient private sector dynamism to reduce external imbalances.

- Demographic Pressures: With population growth (~2% annually) and youth entering labor force, public sector capacity constraints are intensifying. Failure to shift employment toward private sector will exacerbate fiscal pressures and create unemployment among Kuwaiti youth.

- Geopolitical Exposure: Border disputes with Iraq and Iran, regional security tensions, and proximity to conflict zones create unpredictable external shocks (exemplified by COVID-19’s impact and historical military expenditures during regional conflicts).

Private Sector Development Constraints

- Kuwaitization Mandate without Matching Productivity: Regulatory requirements to hire Kuwaitis in private sector roles, without corresponding skill development or wage competitiveness relative to public sector, reduce private sector profitability and competitiveness.

- Limited Entrepreneurial Culture: Public sector employment dominance and generous benefits have historically discouraged private sector entrepreneurship. While startup ecosystem support is emerging, cultural shifts are slow.

- Brain Drain and Talent Migration: Skilled Kuwaitis, attracted by public sector security and income, are underrepresented in competitive private sectors. Expatriate-dominated workforces (70% of private sector) create dependency on migrant labor and limit knowledge transfer to Kuwaitis.

- Financing Constraints for SMEs: While government SME development funds exist (e.g., Kuwait National Fund for SMEs), private sector credit for small businesses remains constrained. Bank lending criteria are conservative, and venture capital ecosystem is nascent.

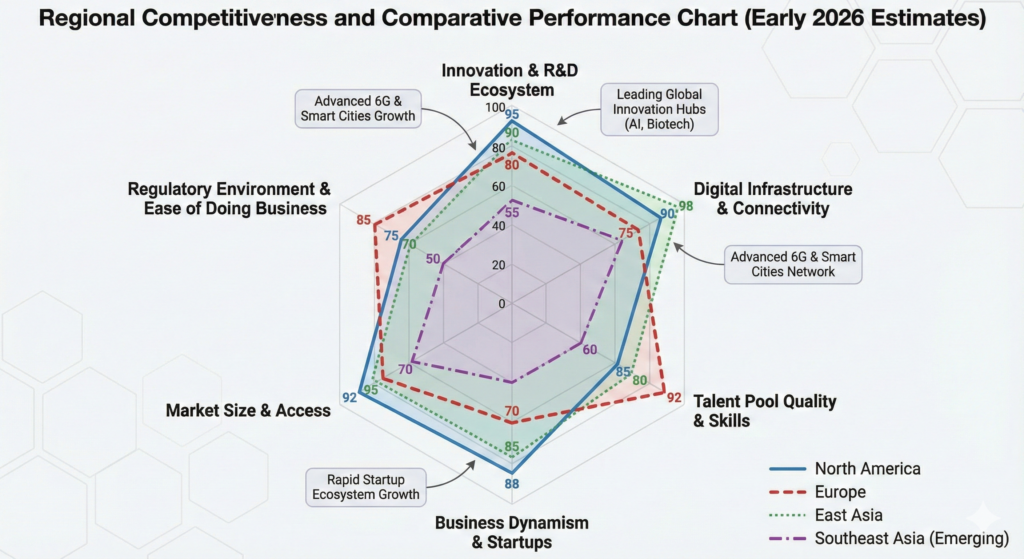

Part XI: Regional Competitiveness and Comparative Performance

GCC Peer Benchmarking

Kuwait’s diversification progress must be contextualized against regional competitors:

| Metric | Kuwait | UAE | Saudi Arabia | Regional Performance |

|---|---|---|---|---|

| Arab Competitiveness Ranking | 12th | 1st (UAE) | 2nd | Kuwait lags by 10+ positions |

| Global Innovation Index | 71st | ~30s | ~40s | Kuwait underperforming peer expectations |

| Ease of Doing Business | 71st | ~15-20s | ~50s | Improving but below peers |

| FDI Stock (2024) | $16.7bn | $200+ bn | $100+ bn | Kuwait’s inward FDI is modest by regional standards |

| Non-Oil GDP Share | 56.6% | ~65% | ~55% | Comparable but UAE leads in diversification breadth |

| Foreign Investor Base | 7.8% stock trading | 40%+ | 30%+ | Limited international investor participation |

Assessment: Kuwait’s diversification progress is real but lags regional leaders. The UAE and Saudi Arabia have advanced further in attracting foreign talent, capital, and companies. Kuwait’s regulatory improvements are moving in the right direction but face execution gaps and political economy constraints (e.g., subsidy reduction, public sector employment reform) that are more entrenched than in regional peers.

Part XII: Vision 2035 Implementation Roadmap and Timeframe

Strategic Pillars Alignment

Kuwait’s Vision 2035 (“New Kuwait”) is organized around seven pillars, each with multiple strategic programs. Progress is tracked through the Third Kuwait National Development Plan (2020-2025) and will continue through successive five-year plans:

- KNDP-1 (2010-2015): Legislative foundation

- KNDP-2 (2015-2020): Infrastructure focus

- KNDP-3 (2020-2025): Private sector engagement (current, being executed)

- KNDP-4 (2025-2030): Knowledge economy emphasis (upcoming)

- KNDP-5 (2030-2035): Smart Kuwait transition

Critical Success Factors and Implementation Capacity

- Fiscal Consolidation and Revenue Diversification: Must implement VAT (under discussion), reduce subsidies, and reform public sector compensation. Without progress, fiscal deficits will constrain investment capacity.

- Labor Market Reforms: Must execute on National Jobs Strategy, improve education-labor market alignment, and incentivize private sector employment among Kuwaitis. Public sector reform (wage rationalization, employment limits) is essential but politically contentious.

- Regulatory Modernization: Must complete legislative updates (commercial companies law, investment law, PPP framework, competition enforcement) and build institutional capacity for consistent enforcement.

- Private Sector Competitiveness: Must reduce barriers to entry, enforce competition rules, and support SME and startup ecosystem development. Monopoly power in certain sectors (real estate, retail, banking) must be addressed.

- Human Capital Development: Must sustain curriculum reform, increase STEM enrollment, improve teacher quality, and shift cultural incentives toward private sector careers.

- Geopolitical Stability and Economic Resilience: Must manage regional security challenges and build economic flexibility to absorb external shocks.

Realistic Timeframe and Scenarios

Base Case (2025-2035): If current reform momentum holds and global oil markets remain stable (~$60-70/bbl), non-oil GDP growth averages 2.7% medium-term, supporting gradual diversification. Oil sector stabilizes at 40-45% of GDP by 2035. Private sector employment among Kuwaitis rises to 40-45% (from current ~30%), supported by education improvements and youth labor force entry. Non-oil exports begin emerging in selective high-value sectors (fintech, logistics, specialized healthcare). This scenario achieves Vision 2035’s core objectives but leaves Kuwait still significantly dependent on oil and regional competitor gaps.

Accelerated Reform Case: If fiscal consolidation (VAT implementation, subsidy reduction, public sector rationalization) and private sector reforms proceed faster, non-oil growth could reach 3.5%+ by 2030, and private sector employment reaches 50%+ of Kuwaiti workforce. FDI inflows accelerate to $3-5 billion annually (supported by improved business environment and mega-project visibility). Diversification breadth increases, with meaningful non-oil exports in 2-3 sectors. This scenario better positions Kuwait as a regional financial and logistics hub.

Reform Stagnation Case: If political economy constraints prevent material reforms (fiscal consolidation, public sector restructuring, labor market change), non-oil growth remains 2-2.5%, oil dependency persists at 45-50% of GDP, and public sector employment stagnates at ~70%. Fiscal buffers deplete, growth stalls, and regional competitiveness gap widens. This scenario represents downside risk and motivates urgent action.

Conclusion: Kuwait at a Diversification Inflection Point

Kuwait has made genuine progress in laying the foundations for economic diversification. The non-oil sector now represents 56.6% of GDP; non-oil growth is positive and accelerating (3.1% in Q2 2025); mega-projects (Silk City, ports, airports) are advancing; Islamic finance is emerging as a competitive advantage; and digital transformation is creating new growth vectors. Capital markets and business environment reforms are moving Kuwait toward greater openness and international integration.

Yet this structural progress masks significant implementation challenges and institutional barriers. Public sector dominance (74% of Kuwaiti employment), fiscal rigidity (80% of spending on wages and subsidies), and labor market distortions (Kuwaitization without skill development) continue to constrain private sector competitiveness. FDI inflows remain modest relative to peer expectations; foreign investor participation in capital markets remains limited. Human capital development lags high-income country standards. Regional competitors (UAE, Saudi Arabia) are advancing faster on multiple diversification dimensions.

Success on Vision 2035’s ambitious 2035 targets—transforming Kuwait into a regional financial, commercial, and logistics hub with a balanced, knowledge-based economy—requires acceleration of reforms across governance, fiscal sustainability, education, labor markets, and private sector competitiveness. The window for strategic action is closing: as oil production normalizes and fiscal buffers deplete, the urgency of structural transformation intensifies.

Kuwait’s strong sovereign wealth position (KIA’s $1.029 trillion in assets) and strategic geographic location provide significant advantages. However, these assets are only effective if deployed strategically alongside institutional and governance reforms. The next five years (KNDP-3, 2020-2025, and early KNDP-4) will prove critical in determining whether Kuwait achieves meaningful diversification by 2035 or remains primarily dependent on hydrocarbons and regional rentier structures.

official Kuwait government website links

| Kuwait Government Online | Kuwait Government Online |

| Council of Ministers | Council of Ministers |

| Ministry of Interior | Ministry of Interior |

| Ministry of Health | Ministry of Health |

| Ministry of Finance | Ministry of Finance |

Read more country case studies done before this.

| china | china |

| hong kong | hong kong |

| japan | japan |

| sinagpore | singapore |

| taiwan | taiwan |

| uAE | UAE |

| vietnam | vietnam |

| saudi arbia | saudi arbia |

| india | india |

| south korea | south korea |