Qatar

Qatar investment and diversification strategy 2026.

Executive Summary

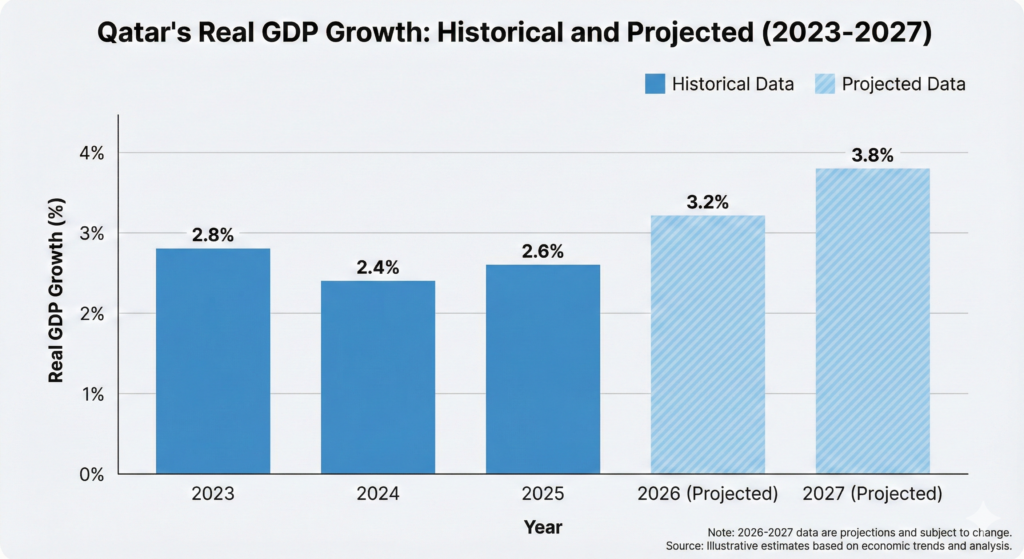

Qatar stands at an inflection point in its economic evolution. Simultaneously executing one of the world’s largest LNG expansion projects (the North Field megaproject worth $40+ billion) while systematically building non-hydrocarbon economic pillars, the nation is pursuing a dual-track strategy that defies conventional wisdom about resource-dependent economies. Real GDP growth is projected to accelerate from 2.4% in 2024 to 6.8% by 2027, driven initially by hydrocarbon capacity expansion but increasingly anchored by tourism, logistics, financial services, manufacturing, and knowledge-based sectors. Non-hydrocarbon sectors now constitute 65.6% of GDP and are growing at 3.4-5.3% annually, demonstrating substantive economic rebalancing beyond rhetoric.

This transformation is not accidental but meticulously orchestrated through Qatar National Vision 2030, the Third National Development Strategy (2024-2030), strategic infrastructure investment, and institutional alignment. The outcome is a high-income, resilient economy poised to sustain relevance beyond hydrocarbons—a model worthy of examination for other resource-rich nations.

Part 1: The Hydrocarbon Engine Re-Ignited—The North Field Expansion

Project Scale and Strategic Rationale

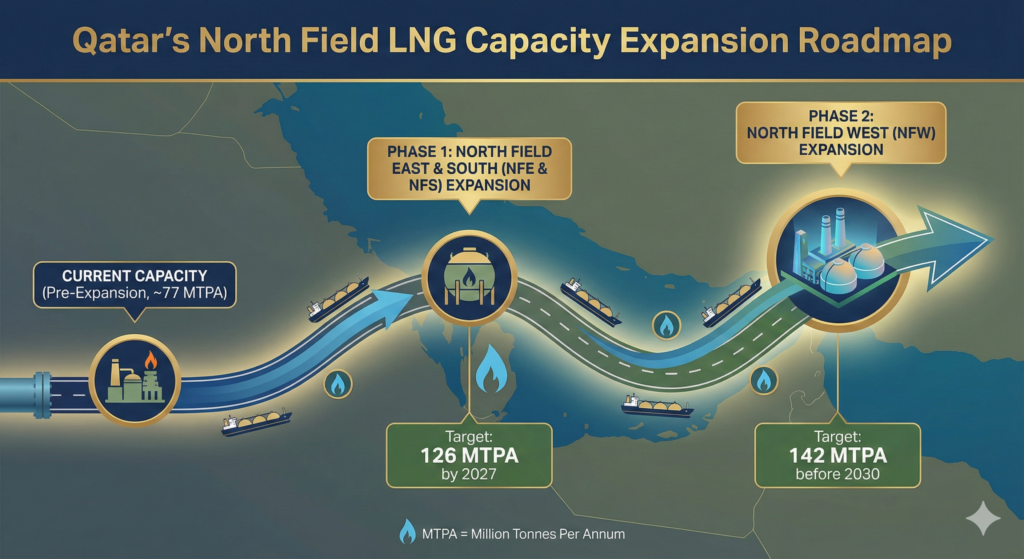

In February 2024, Qatar formally sanctioned the full North Field expansion program, ending a two-decade self-imposed moratorium on major LNG capacity additions. The decision represents a calculated bet that despite global energy transition, natural gas demand will remain robust for decades, particularly given geopolitical fragmentation and Europe’s pivot away from Russian gas.

The North Field East (NFE) expansion, the first phase, increased Qatar’s LNG production capacity by 43%—from 77 Mtpa to 110 Mtpa. Three subsequent phases (NFE, NFS, NFW) will push capacity to 142 Mtpa by 2030, representing an 85% increase from the baseline. The combined investment across all phases exceeds $40 billion, with first production from NFE confirmed for mid-2026.

Qatar’s North Field LNG Capacity Expansion Roadmap

The scale of this expansion ensures continued supply to long-term contracted buyers and positions Qatar to capture upside from geopolitical supply disruptions. Long-term sales agreements have been signed with major utilities and energy companies across Asia (China’s CNPC and Sinopec), Europe (Germany), and South Asia (Bangladesh), locking in future revenues with multidecade visibility.

Economic Ripple Effects and Ecosystem Development

The North Field expansion’s direct employment impact is substantial—thousands of engineers, construction workers, project managers, and supply chain professionals. The indirect effects cascade through ancillary sectors: shipping and maritime services, advanced project management consulting, specialized engineering services, port operations, customs clearance, transshipment logistics, warehousing, and financial services (project finance, working capital financing, trade finance, treasury solutions). Qatar investment and diversification strategy 2026.

QatarEnergy’s partnerships with international oil majors (Shell, ExxonMobil, ConocoPhillips, Eni, TotalEnergies)—who collectively hold 25% equity stakes worth $7+ billion—bring technology transfer, operational expertise, and capital that strengthen the project and Qatar’s institutional capacity. Construction contracts awarded to Samsung C&T, Técnicas Reunidas, Wison, Technip Energies, and Consolidated Contractors employ hundreds of multinational firms and subcontractors, generating economic activity across the supply chain.

Environmental Integration and Carbon Management

A distinctive feature of the North Field expansion is its carbon management infrastructure. The project will incorporate the world’s largest carbon capture and storage (CCS) facility for an LNG project, with plans to increase CCS capacity by 400% by 2035. An 800 MW solar power plant under construction will power onshore liquefaction facilities, reducing operating carbon intensity and demonstrating integration of renewable energy into hydrocarbon operations.

This technological sophistication reflects Qatar’s positioning alongside global climate policy evolution—decoupling LNG expansion from narratives of unchecked carbon growth and demonstrating that hydrocarbon extraction can coexist with serious emissions mitigation.

Part 2: Non-Hydrocarbon Diversification—The Strategic Pillars

Sector Diversification Performance and Momentum

Qatar’s Real GDP Growth: Historical and Projected (2023-2027)

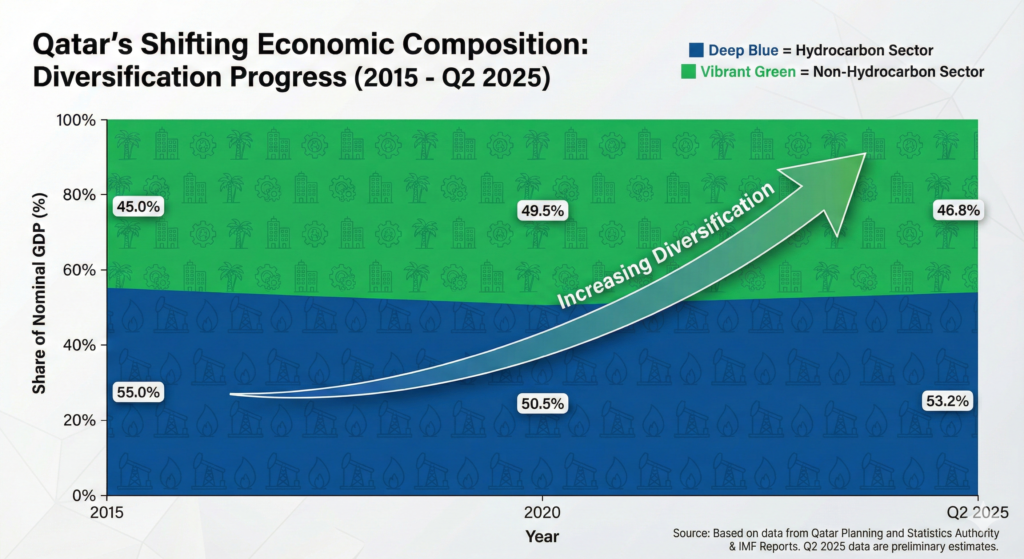

Qatar’s non-hydrocarbon economy reached 65.6% of real GDP in Q2 2025, up from 60.6% in Q1 2024—a 5-percentage-point improvement in just 18 months. This structural shift reflects both intentional policy and genuine sectoral momentum. Real growth in non-hydrocarbon activities accelerated to 5.3% in Q1 2025 and sustained 3.4% in Q2 2025, outpacing population growth and demonstrating productivity-based expansion.

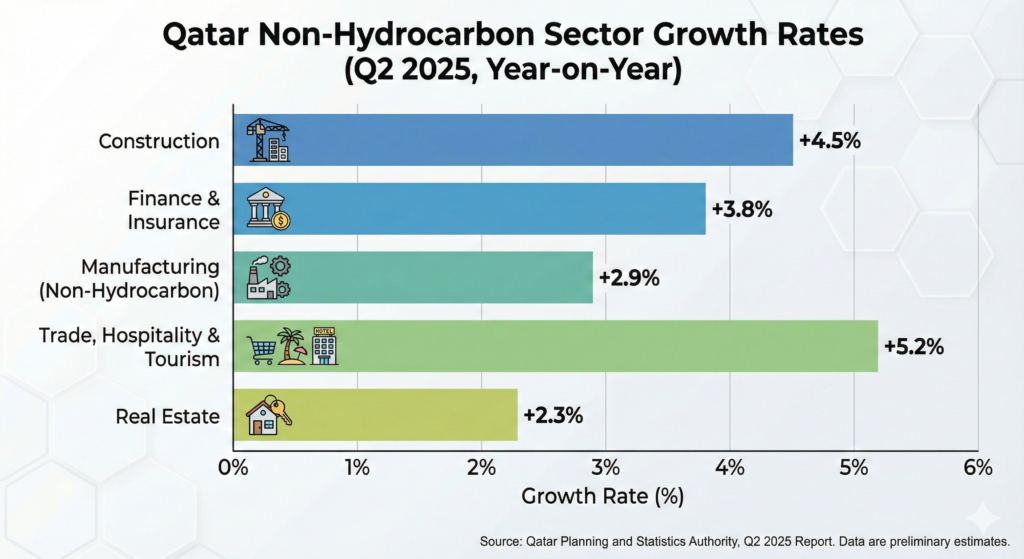

Qatar Non-Hydrocarbon Sector Growth Rates (Q2 2025)

Within the non-hydrocarbon economy, service-oriented sectors demonstrated exceptional vitality. Accommodation and food services grew 13.4-13.8%, reflecting sustained tourism momentum from the FIFA World Cup 2022 infrastructure legacy and the government’s deliberate event-driven tourism strategy. Wholesale and retail trade expanded 8.8-14.6%, indicating robust domestic demand and functioning consumer markets. Construction rebounded to 8.7-9.1% growth after a post-2022 slowdown, signaling renewed capital project execution and urban development. Professional, scientific, and technical activities grew 7.2%, reflecting demand for specialized services as the economy modernizes.

Qatar’s Shifting Economic Composition: Diversification Progress

Tourism and MICE: From Event Destination to Year-Round Hub

Strategic Positioning Post-World Cup

The 2022 FIFA World Cup was transformational for Qatar’s tourism infrastructure but nearly catastrophic for subsequent visitor flows if the nation had failed to establish a year-round event calendar. Rather than allowing infrastructure to depreciate, Qatar’s government (through Visit Qatar) orchestrated a comprehensive events portfolio spanning sports, culture, entertainment, and business MICE activities designed to maintain consistent visitor inflows and justify sustained hospitality and services sector investment.

2025-2026 Events Calendar and Economic Impact

The unified Qatar Calendar 2025-2026 encompasses major sporting events (Formula 1 Grand Prix at Lusail Circuit, FIFA tournaments including the U-17 World Cup, confederations cup, T100 Triathlon Championships), cultural festivals (Doha Tattoo military music festival, Qatar International Food Festival, Katara Cultural Village programming), and entertainment featuring international and regional artists. This diversity targets multiple tourist demographics—sports enthusiasts, culinary tourism, cultural heritage tourism, business travelers for MICE, and leisure tourists.

The Qatar Travel Mart (QTM) 2025-2026 functions as a strategic marketing platform, connecting global travel industry professionals with Qatar’s hospitality providers, destination management companies, and tourism boards. By positioning Qatar as a leading MICE destination alongside UAE and Saudi Arabia’s competing hubs, the event generates bookings, increases awareness, and validates Qatar’s credentials for hosting large-scale international conferences and exhibitions.

Accommodation and food services recorded 13.4% YoY growth in Q2 2025, the fastest growth among all non-hydrocarbon sectors, directly attributable to tourism momentum. This sustained expansion supports a cascading ecosystem: hotels require staff, food suppliers, laundry services, maintenance, and IT infrastructure; tourists spend on retail, transportation, entertainment, and dining; foreign visitors bring foreign exchange. Multiplier effects strengthen competing non-energy sectors. Qatar investment and diversification strategy 2026.

Strategic Infrastructure Assets

Qatar’s tourism competitiveness rests on infrastructure that few competitors can replicate. Hamad International Airport, consistently ranked among the world’s best for both cargo and passenger services, connects Qatar to global markets with modern facilities and seamless connections. The Doha Metro system, opened post-2015, provides efficient public transit from airport to hotels, stadiums, and entertainment districts. Purpose-built stadiums from the World Cup, now utilized for Formula 1, concerts, and other events, offer world-class facilities unavailable in many competing destinations. Hotels range from budget to ultra-luxury, accommodating diverse visitor segments.

Hamad Port and Logistics: The Global Transshipment Hub Strategy

Port Infrastructure and Regional Role

Hamad Port, inaugurated in 2016, is one of the world’s greenfield port developments and now ranks as the third most efficient container port globally (World Bank/S&P Global 2023-2024 Container Port Performance Index). Designed to handle 7.5 million TEUs annually, the port has evolved from serving primarily as a national gateway to functioning as a regional transshipment hub, with transshipment now representing nearly 50% of total container volumes handled (January-November 2025).

This transshipment transformation is economically significant. Regional cargo flows between Asia-Middle East-Europe passing through Qatar can optimize routing: rather than lengthy transits on major shipping lanes, vessels can offload at Hamad, consolidate cargo, and redispatch with faster turnaround times and lower per-unit costs. Shipping lines operating east-west corridors increasingly prioritize Qatar as a connectivity hub, driving cargo volumes and port revenues.

Logistics Ecosystem Development

The port’s success generates spillover benefits across logistics and services. QTerminals, the port operator, has expanded internationally, acquiring stakes in ports across the Eastern Mediterranean and Europe, positioning Qatari logistics as a regional player with global connectivity. Domestic logistics firms (such as GWC—Gulf Logistics Worldwide) operate complementary land transport, warehousing, and customs services, creating an integrated logistics value chain.

Qatar’s free zones (at Hamad Port and elsewhere) offer attractive regulatory and tax benefits, incentivizing warehouse operations, light manufacturing, and re-export businesses. Combined with strategic geographic positioning (midway between major Asian and European trade zones) and world-class infrastructure, Qatar has positioned itself as an essential node in global supply chains, particularly for companies seeking alternative routing to avoid congestion at Suez or Strait of Malacca chokepoints.

Transport and storage sector growth moderated to 3.5% in Q1 2025 (from 9% in H1 2023), reflecting normalization after high-growth phases, yet remains solidly positive and integral to broader economic activity.

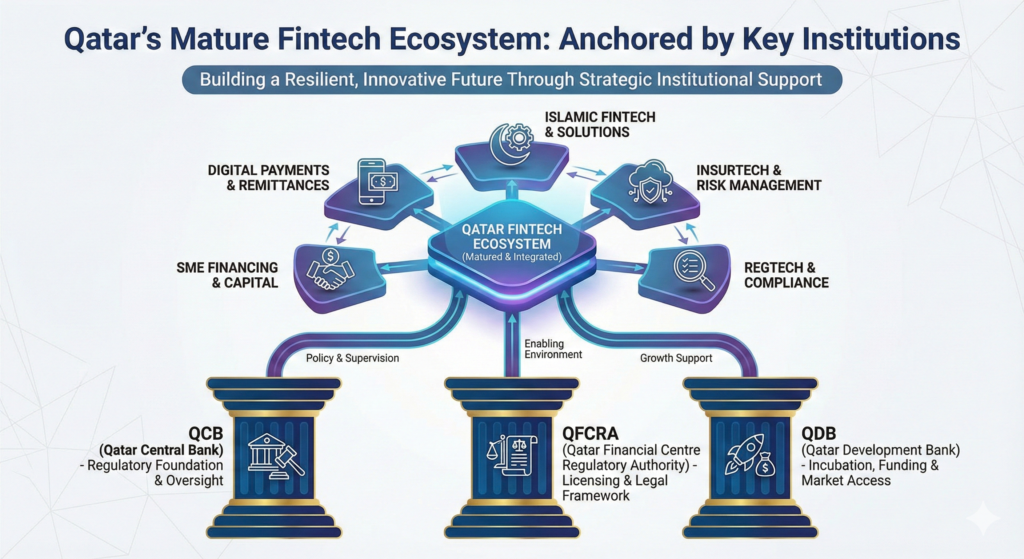

Financial Services and Fintech: Building a Regional Hub

Qatar Financial Centre (QFC) as Regulatory Platform

The Qatar Financial Centre, established through legal and regulatory autonomy, has attracted over 3,000 registered companies in finance, IT, tax, and consulting. Unlike traditional banking regulators, the QFC functions as an autonomous jurisdiction offering 100% foreign ownership, profit repatriation, and tax incentives—positioning it as an attractive registry for financial technology companies, insurers, and asset managers seeking regional presence with regulatory clarity.

This institutional design reflects a competitive strategy: whereas traditional banking sectors are consolidated and heavily regulated, the QFC provides regulatory flexibility and speed-to-market that appeals to fintech innovators and international financial services firms. Companies can establish operations, obtain regulatory sandbox approval, and launch pilots within months rather than years.

Fintech Market Development and Strategic Partnerships

Qatar FinTech Hub (QFTH): A dedicated institution providing incubation, acceleration, and regulatory sandbox services. Over 50 fintech startups have graduated from QFTH programs, with combined portfolio valuations reaching $500 million. The hub has committed $16 million in pre-seed investments (2020-2028) targeting early-stage companies. This capital commitment, while modest by global standards, is substantial for a regional hub and demonstrates sustained institutional backing for innovation.

Partnership Framework: In November 2025, the QFC Authority and Doha Bank signed a memorandum of understanding to accelerate fintech growth through joint research, prototype development, technical guidance, streamlined account opening, and structured quarterly engagement. This partnership directly addresses a critical pain point for fintech startups—access to banking relationships—by institutionalizing collaboration rather than leaving connections to ad-hoc networking.

Islamic Fintech Growth: QFC projects the Islamic fintech market to reach QAR 16.1 billion by 2028 at 10% CAGR, reflecting both global Islamic finance growth and Qatar’s institutional strengths in Sharia-compliant financial products. Partnerships between major banks (Qatar Islamic Bank, Commercial Bank Qatar) and fintech firms (QPay, the nation’s largest fintech) demonstrate product innovation in remittances, contactless payments, and micro-lending.

Digital Asset Development: The QFC’s Digital Assets Lab has over 20 companies in its regulatory approval pipeline, positioning Qatar to become a leading jurisdiction for blockchain-based financial services, stablecoins, and digital asset infrastructure.

Central Bank Leadership: The Qatar Central Bank’s National Fintech Strategy and wholesale central bank digital currency (CBDC) project underscore institutional commitment to financial innovation and digital transformation.

Islamic fintech and digital assets represent emerging verticals where Qatar has competitive advantages (institutional expertise in Islamic finance, regulatory clarity through QFC, capital availability) and can compete for regional market share against Bahrain’s Islamic banking hub and UAE fintech centers.

Education: Knowledge Economy Foundation

Qatar Education Market Growth Projection

Education represents a foundational pillar of Qatar National Vision 2030, underpinning the transition to a knowledge-based economy. Qatar’s education market is projected to grow from approximately $8.5 billion in 2025 to $13 billion by 2034 at 6.5% CAGR.

Education City: Flagship Platform

Education City, a 2,500-acre development, houses six American university branch campuses (Cornell University with Weill Cornell Medical College, Carnegie Mellon, Texas A&M, Georgetown, Northwestern, Virginia Commonwealth University) alongside the Qatar Science & Technology Park. This integration creates a “triple helix” model where academic research, industry collaboration, and government funding align to accelerate innovation commercialization.

Weill Cornell Medical College Qatar exemplifies the institutional depth: it offers medical education at international standards, conducts biomedical research addressing Qatar’s health challenges (diabetes, obesity, cardiovascular disease, cancer), and provides clinical services. The institution translates research into public health policy, creating pathways from bench to bedside to population health. Qatar investment and diversification strategy 2026.

Universities are now expanding graduate programs and deepening industry partnerships, moving beyond undergraduate instruction toward applied research and innovation. These developments strengthen the knowledge economy by retaining high-skilled graduates domestically and creating conditions for technology commercialization.

Education Market Drivers

Growth is driven by: (1) sustained government investment prioritizing quality and international competitiveness; (2) rising expatriate population (85%+ of Qatar’s workforce), creating demand for international school capacity; (3) private and international school expansion capturing market share; (4) accelerated EdTech adoption, with online and blended learning models expanding across K-12, higher education, and professional training.

Qatar Science & Technology Park (QSTP): Incubating the Knowledge Economy

Institutional Design and Free Zone Status

QSTP, established in 2009 at $800+ million investment by Qatar Foundation, functions as a technology-focused economic zone offering 100% foreign ownership, tax and duty exemptions, and integrated university access. This positioning attracts multinational technology firms (initial tenants included EADS, ExxonMobil, GE, Microsoft, Rolls-Royce, Shell, Total) and incubates local startups.

The park employs 1,000+ staff and operates the XLR8 flagship accelerator program, providing mentorship, funding, and industry connections to early-stage tech companies. By co-locating with Education City universities, QSTP facilitates university spin-outs, direct industry-academic collaborations, and recruitment of university talent into commercial ventures.

Focus Areas and Innovation Pathways

1. Information Technology & AI: Companies like Kanari AI (Arabic speech recognition and text-to-speech) and Tashan Technology (AI-driven robotics) represent Qatar’s ambition to develop language and automation technologies adapted to regional markets where global solutions underperform.

2. Healthcare & Biomedical Research: Biotech research, medical device innovation, and clinical informatics address Qatar’s health challenges while creating exportable intellectual property and medical technology businesses.

3. Energy & Sustainability: Clean energy solutions, environmental monitoring, and waste management technologies support both Qatar’s climate commitments and export market demand.

4. Emerging Technologies: Quantum computing partnerships and digital innovation initiatives position Qatar for future-generation technology leadership.

Impact and Ecosystem Metrics

Over 50 fintech startups have been supported through QFTH (housed within QSTP’s broader innovation ecosystem), with combined valuations of $500 million. While modest by Silicon Valley standards, this represents substantive tech ecosystem maturation for a regional hub. The Qatar Investment Authority is establishing a $1 billion venture capital fund of funds, investing in emerging technologies through venture and venture studio funding—a structural commitment to patient capital that supports technology development across geographies.

Healthcare: Positioning as a Regional Medical Destination

Qatar’s healthcare system ranks in the world’s top five for quality of care. Strategic initiatives target conversion of this institutional strength into medical tourism revenue and biomedical research leadership.

Biomedical Research Infrastructure: Weill Cornell Medical College Qatar, partner research institutions, and government-backed programs conduct bench-to-bedside research addressing Qatar’s prevalent health challenges (diabetes, obesity, cardiovascular disease, cancer). This research, combined with clinical delivery capacity, positions Qatar as a regional center of medical excellence.

Medical Tourism Development: Initiatives to attract international patients seeking specialized care (cardiology, oncology, pediatrics) are expanding. Partnerships with international healthcare providers, integration of digital health platforms, and marketing through medical tourism channels create new revenue streams.

Workforce Development: Training programs for physicians, nurses, and specialized healthcare professionals ensure local capacity while creating employment in a high-value sector.

Manufacturing and Industrial Diversification

Manufacturing sector growth reached 5.6% in Q1 2025, reflecting progress in industrial diversification away from petrochemical commodity production.

Blue Ammonia Production: Qatar is developing the world’s largest blue ammonia plant, integrating carbon capture and sequestration (CCS) technology. Blue ammonia—ammonia produced with minimal carbon emissions—addresses growing demand from European fertilizer manufacturers and cleantech supply chains. This represents downstream value-addition on hydrocarbon feedstocks with differentiated environmental attributes.

Petrochemical Value-Addition: Rather than exporting crude hydrocarbon feedstocks, Qatar increasingly focuses on downstream processing—lubricants, specialty chemicals, refined products—capturing greater value-added margin.

Parts and Equipment Manufacturing: Industrial parts manufacturing, electrical equipment, and machinery assembly support both domestic infrastructure needs and regional export markets.

Part 3: Economic Performance and Growth Trajectory

Qatar’s Real GDP Growth: Historical and Projected (2023-2027)

Qatar’s macroeconomic performance in 2024-2025 reflects the early stages of LNG expansion impact. Real GDP grew 2.4% in 2024, with Q4 2024 showing robust 6.1% YoY growth as industrial production ramped. Quarterly data for 2025 shows volatility (Q2: 1.9%, Q3: 2.9%) reflecting seasonal patterns and project-specific fluctuations, with full-year 2025 estimated at 2.8%.

However, the IMF’s forward guidance is decisive: real GDP growth is projected to reach 5.3% in 2026 and peak at 6.8% in 2027 as the North Field East production ramps to full capacity. This acceleration—more than tripling growth rates from 2024—reflects the megaproject’s economic impact.

The acceleration is not merely hydrocarbon-driven. Non-hydrocarbon real growth has accelerated to 5.3% in Q1 2025 and 3.4% in Q2 2025, with 11 of 17 economic activities recording positive growth. This broad-based diversification increases economic resilience and reduces vulnerability to global energy price volatility.

Inflation remained subdued at 1.07% in 2024, thanks to price controls and the pegged QAR-USD exchange rate, providing a stable macroeconomic anchor for business planning and household finances.

Part 4: Structural Drivers of Transformation

National Vision 2030 and Strategic Alignment

Qatar National Vision 2030 provides the foundational blueprint, articulating four pillars: (1) economic development (responsible hydrocarbon use, diversification, private sector leadership); (2) human development (education, healthcare, social progress); (3) environmental development (sustainable growth, climate action); (4) governance (institutional strength, accountability).

The Third National Development Strategy (NDS3) 2024-2030, launched in January 2024, operationalizes this vision with specific targets: 4% annual GDP growth (higher than previous 3% target), prioritization of three economic sectors (manufacturing, logistics, tourism), and explicit transition toward private sector-driven growth.

This strategic continuity—consistent over two decades—enables institutional alignment and long-term investment horizons. Private businesses can plan multi-year expansion strategies with confidence that government policies will remain coherent. This contrasts with policy-whipsaw in countries lacking multi-generational strategic commitment.

Public-Private Partnership Model

Rather than nationalizing economic development, Qatar deploys strategic public investment and partnerships to catalyze private sector activity. The North Field expansion reflects this model: QatarEnergy (majority state-owned) partners with Shell, ExxonMobil, and other majors (25% stakes); Hamad Port is operated by QTerminals with private sector participation; the QFC provides regulatory platform for private fintech firms; QSTP incubates private companies with government facilities.

This hybrid approach leverages state capital and policy coordination while preserving private sector efficiency and incentives.

Infrastructure as Competitive Advantage

Qatar’s infrastructure investments—Hamad International Airport, Hamad Port, Doha Metro, purpose-built MICE venues—create defensible competitive advantages. Competitors cannot quickly replicate such assets. This infrastructure enables business-friendly operations (efficient logistics, accessible venues, modern transportation), attracting regional and international companies to establish operations.

Global Integration and Positioning

Qatar strategically positions itself within global supply chains and financial networks rather than pursuing autarky. The North Field expansion prioritizes long-term contracts with Asian, European, and South Asian buyers, integrating Qatar into global energy markets. The QFC attracts international financial firms seeking regional footprint. Education City universities bring international academic standards and networks. This integration creates economic dynamism but also external dependencies requiring skillful geopolitical management.

Part 5: Challenges and Risk Factors

Hydrocarbon Price Volatility and Contract Uncertainty

Approximately 75% of the new North Field expansion LNG output remains uncontracted as of December 2025. QatarEnergy must navigate global LNG markets with pricing and volume uncertainty. A sustained period of low gas prices would compress margins and reduce project economics, although the long-term contracts already signed at premium prices provide downside protection and establish reference pricing for additional volumes.

Labor Market Structure and Expatriate Dependence

Qatar’s workforce is approximately 85% expatriate, creating structural dependencies on migrant labor availability and labor cost dynamics. The nation has implemented labor reforms improving worker protections, but reliance on temporary visa workers limits the development of multigenerational human capital. Upskilling citizens through education and training—critical to sustaining a knowledge economy—requires sustained effort to overcome cultural preferences and educational gaps.

Private Sector Maturation and Business Environment Competition

Transitioning from public sector-led growth to private sector-driven development is institutionally challenging. The IMF notes that Qatar’s key challenge is fostering a “more conducive business environment” and “boosting productivity,” reflecting recognition that private sector dynamism cannot be simply mandated. Competition with UAE (particularly Dubai’s diversified services and logistics) and Saudi Arabia (Vision 2030 investment scale) creates pressure to continuously improve business environment competitiveness.

Geopolitical and Regional Stability

Qatar’s geographic position in the Persian Gulf exposes it to regional conflicts, sanctions, and trade disruptions. The 2017-2021 blockade imposed by neighboring states demonstrated vulnerability to geopolitical isolation. While relations have normalized, structural regional tensions persist, creating uncertainty for long-term business planning.

Energy Transition and Long-term Hydrocarbon Demand

Global decarbonization trajectories raise questions about long-term natural gas demand, particularly if hydrogen, renewables, and storage technologies accelerate faster than projected. This uncertainty underlies the strategic emphasis on diversification—reducing dependence on a single energy source that may face structural demand headwinds beyond mid-century.

Conclusion: A Transformation in Progress

Qatar’s economic transformation is neither complete nor risk-free, but it is substantive. Hydrocarbon re-investment through the North Field expansion ensures near-term revenue visibility and infrastructure-enabled growth through 2030. Simultaneously, systematic development of tourism (driven by mega-events and MICE infrastructure), logistics (Hamad Port’s transshipment role), financial services (QFC’s fintech ecosystem), knowledge economy (Education City and QSTP), and manufacturing capabilities is creating a diversified, more resilient economy.

Non-hydrocarbon sectors now constitute two-thirds of GDP and are growing faster than hydrocarbon sectors. This rebalancing, combined with world-class infrastructure, strategic positioning within global networks, and long-term institutional commitment to National Vision 2030, positions Qatar for sustained economic relevance beyond its hydrocarbon reserves.

The transformation is facilitated by financial capacity (oil and gas wealth), institutional quality (coherent long-term strategy), and strategic asset deployment (education, research, logistics infrastructure). For other resource-rich nations, Qatar’s model offers lessons: sustained commitment to diversification over political cycles, strategic infrastructure investment to create competitive advantages, integration into global value chains rather than protectionist isolation, and institutional partnerships (public-private, international academic, industry collaboration) that leverage state resources while preserving market-driven efficiency.

Whether Qatar’s diversification proves sustainable and whether private sector-driven growth genuinely displaces public sector dependence remain open questions. But the trajectory—both in data and strategic positioning—demonstrates a nation-state seriously attempting to transcend rentier capitalism and build a modern, knowledge-based economy. The results, though early, are promising and merit continued observation as a case study in deliberate, state-guided economic transformation.

official Qatar government websites

| Qatar National Vision 2030 | Qatar National Vision 2030 |

Read more country case studies done before this.

| iran | iran |

| china | china |

| hong kong | hong kong |

| japan | japan |

| sinagpore | singapore |

| taiwan | taiwan |

| uAE | UAE |

| vietnam | vietnam |

| saudi arbia | saudi arbia |

| Malaysia | Malaysia |

| india | india |

| south korea | south korea |

For lottery players, lottuse has some interesting options. Worth checking out if you want to try your luck. Good luck: lottuse