Bangladesh economic development sectors 2026.

Executive Summary

Bangladesh stands at a critical juncture in its economic trajectory. As the world’s second-largest apparel exporter and a manufacturing hub for over 170 million people, the nation has achieved remarkable growth over three decades. However, the upcoming graduation from Least Developed Country (LDC) status in November 2026 presents a watershed moment that demands urgent structural diversification and competitiveness improvements. With 82% of export earnings concentrated in the Ready-Made Garments (RMG) sector, Bangladesh faces potential annual export losses of $8 billion as duty-free trade preferences expire. This comprehensive analysis examines Bangladesh’s seven key economic engines—RMG, pharmaceuticals, information and communication technology (ICT), agro-processing, light engineering, infrastructure development, and renewable energy—evaluating their current performance, growth trajectories, competitive positioning, and strategic imperatives for post-LDC transition.

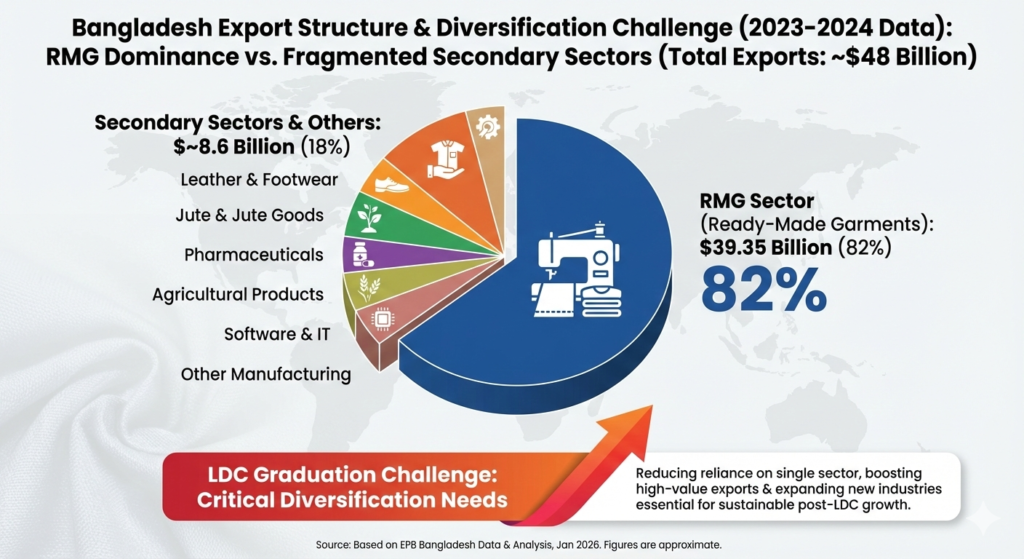

Bangladesh’s RMG sector dominates exports at $39.35 billion, representing approximately 82% of total merchandise exports. Secondary sectors remain fragmented, highlighting critical diversification needs ahead of LDC graduation

Bangladesh’s export portfolio reveals extreme sectoral concentration. The RMG sector generates $39.35 billion annually (8.84% growth in FY2024-25), dwarfing all alternatives. However, emerging sectors demonstrate substantially higher growth rates, with renewable energy achieving 38.6% CAGR, agro-processing 16.6%, and ICT 12.99%, signaling where future economic dynamism may lie.

1. Ready-Made Garments: Dominance Under Pressure

Sector Overview

The RMG sector remains Bangladesh’s economic anchor, generating $39.35 billion in FY2024-25 exports—a growth of 8.84% despite substantial headwinds including political instability during the fiscal year and subsequent recovery. Within this aggregate, knitwear contributed $21.16 billion (9.73% growth) while woven garments reached $18.19 billion (7.82% growth), reflecting sustained demand across product categories. The sector employs approximately 4 million workers, predominantly women, representing the largest formal employment base for female workers in South Asia. Bangladesh economic development sectors

Market Concentration and Geographic Dependency

Bangladesh’s RMG exports demonstrate geographic concentration that amplifies vulnerability. The European Union absorbs 50.1% of total RMG exports ($19.71 billion), the United States 19.18% ($7.54 billion), the UK 11.05% ($4.35 billion), and Canada 3.31% ($1.30 billion). This 83% concentration in just four markets creates significant exposure to individual market policy changes and demand shocks. Year-on-year growth rates reflect this concentration risk: EU exports grew 9.10%, USA 13.79%, and Canada 12.07%, while UK growth remained modest at 3.68%.

Encouragingly, Bangladesh has begun penetrating non-traditional markets, which now represent 16% of RMG exports ($6.44 billion with 16.36% market share). Turkey demonstrated 25.62% growth, India 17.39%, and Japan 9.13%, indicating successful market diversification efforts. However, this 16% share of non-traditional markets demonstrates the opportunity cost of geographic concentration: the global non-traditional apparel market reached approximately $150 billion in 2024, with Bangladesh capturing only 6% of this opportunity—suggesting substantial untapped potential.

Operational Challenges and Competitiveness Erosion

The RMG sector faces multiple structural headwinds that threaten its historical cost-competitiveness advantage. Factory capacity utilization has deteriorated substantially, with many facilities operating at 40-50% below normal production levels and most operating 20-30% below capacity. This underutilization reflects weak order pipelines as global retailers facing consumer budget constraints have shifted purchasing strategies. Simultaneously, competitors have intensified competition: Chinese and Indian exporters disadvantaged in the US market (facing up to 50% reciprocal tariffs under potential new US policies) have redirected production and orders toward European markets, directly competing with Bangladesh.

Environmental, Social, and Governance (ESG) compliance presents an emerging vulnerability. Bangladesh currently has fewer than 15% of apparel units certified under global ESG standards, compared with Vietnam’s 20%+ compliance rate. As international buyers increasingly prioritize green-certified suppliers due to EU Corporate Sustainability Due Diligence Directive requirements, Bangladesh risks being sidelined without substantial sustainability investments.

Labor cost advantages have begun eroding. Regional peers including Vietnam and India are implementing strategic labor market reforms (India’s recent amendment allowing women to work night shifts in RMG units, for instance) that enhance productivity and reduce per-unit labor costs. Bangladesh’s wage advantage, historically the sector’s primary competitive lever, continues diminishing relative to other LDC-status nations with lower wage bases.

LDC Graduation Impact

Bangladesh’s November 2026 LDC graduation will trigger tariff increases that directly threaten RMG competitiveness. Currently, 78% of Bangladesh’s exports enjoy duty-free or reduced-tariff access in 38 countries under LDC schemes. Post-graduation, the European Union—accounting for half of all RMG exports—will impose Most Favored Nation (MFN) tariff rates of approximately 12% on apparel products, eliminating the current zero-tariff regime. This tariff increase could reduce the net prices received by exporters, adversely affecting export performance given the price elasticity of global apparel demand. Japan’s tariff will rise to 7%, while the United Kingdom has committed to maintaining Enhanced Preferences with zero tariffs post-graduation, providing a rare bright spot in market access.

Bangladesh will retain LDC benefits for an additional three-year grace period until November 2029 in some markets, providing a window for competitiveness adjustments. However, attempts to qualify for the EU’s Generalized System of Preferences Plus (GSP+) scheme—which would offer duty-free access for 66% of EU tariff lines—are complicated by non-diversification criteria. The GSP+ scheme requires that eligible countries possess diversified economies with apparel representing less than a threshold percentage of total exports. Bangladesh’s 80%+ concentration in RMG exports disqualifies it from GSP+ benefits, ensuring that apparel will face MFN tariffs.

Combined, tariff increases on RMG exports could precipitate annual losses exceeding $8 billion by 2029 if export volumes remain constant. This calculus assumes no supply-side adjustments (e.g., price reductions through cost-cutting or productivity improvements), but such adjustments are constrained by limited capacity for further labor cost reduction in capital-intensive facilities and rising raw material costs driven by global supply constraints.

2. Pharmaceuticals: From Domestic Champion to Export Momentum

Sector Overview and Market Position

Bangladesh’s pharmaceutical industry exemplifies successful industrial policy in a developing economy. The sector produces 98% of domestic medicine demand locally—a dramatic transformation from the post-independence era when multinational corporations dominated 95% of the market. This domestic production capacity supports a population of 170 million while generating export earnings of $213 million in FY2024-25, representing 4% growth from $205 million the prior year.

The industry spans 295 allopathic manufacturers producing annual medicines and raw materials worth approximately BDT 46,985 crore ($5.7 billion at current exchange rates), supported by 172 Ayurvedic, 500 Unani, 29 herbal, and 28 homoeopathic manufacturers. This industrial diversity provides multiple pathways for value creation and employment generation across different therapeutic segments and market preferences.

Export Trajectory and Geographic Reach

Bangladesh pharmaceutical exports have demonstrated consistent growth, more than doubling from $100 million to $213 million over seven years despite global supply chain disruptions. This expansion reached 166 export markets spanning Asia (32% of exports), Africa (24%), Commonwealth Independent States/Central Asia (15%), Middle East (12%), Latin America & Caribbean (8%), Europe (6%), and North America (3%).

Bangladesh’s pharmaceutical exports have grown from $89M (FY2016-17) to $213M (FY2024-25), demonstrating consistent momentum. Industry projections indicate $1 billion in exports by 2029-30 under a 20% CAGR scenario, supported by API localization and market expansion

This geographic diversification—particularly the substantial African and Asian footprint—provides resilience against market-specific shocks and aligns with high-demand, price-sensitive markets for generic pharmaceuticals. Leading exporters including Square Pharmaceuticals (18.8% domestic market share), Beximco Pharma, Incepta Pharmaceuticals, Renata Ltd., and ACI Ltd. have expanded into regulated markets including the United States, European Union, and Australia, validating product quality and regulatory compliance.

Critical Vulnerability: API Import Dependency

The pharmaceutical sector’s Achilles heel remains dependence on imported Active Pharmaceutical Ingredients (APIs). Bangladesh currently imports 85-95% of required APIs at an annual cost of $1.3-1.5 billion, primarily from India and China. This import burden consumes approximately 40-60% of formulation production costs, directly eroding export profitability and creating strategic vulnerability to supply disruptions and currency fluctuations.

This API dependency becomes critical post-LDC graduation. The WTO’s TRIPS (Trade-Related Aspects of Intellectual Property Rights) waiver—which permitted Bangladesh to produce patented medicines for export without patent authorization—expires in 2033. Post-2033, Bangladesh must either produce APIs locally to avoid patent infringement liabilities or negotiate expensive licensing arrangements. Domestic API manufacturing is therefore not merely an export growth strategy but a fundamental requirement for industry sustainability.

Regulatory and infrastructure barriers have impeded API localization. The API Industrial Park at Munshiganj, authorized in 2018, remains incomplete with uncertain electricity connections (delayed to 2025 by multiple accounts). Approval processes for solvent intermediates generate excessive delays, while the Directorate General of Drug Administration (DGDA) faces capacity constraints in processing applications within reasonable timeframes. Industry experts have called for Production Linked Incentives (PLI) schemes, R&D grants, and credit guarantee programs to catalyze investment, alongside a permanent task force coordinating policy across the Finance Ministry, Bangladesh Bank, and Health Ministry.

Growth Projections and Strategic Imperatives

Under a strong-growth scenario with 20%+ compound annual growth rate (comparable to historical performance), pharmaceutical exports could reach $1 billion by 2029 and $1.3 billion by 2030. This projection hinges on three critical developments: (1) domestic API production capacity scaling to 50-60% of demand by 2030, (2) successful market entry into biosimilars and specialized therapeutics (insulin, hormones, anti-cancer drugs, mRNA vaccines), and (3) maintaining export quality and regulatory compliance standards.

Current rankings place Bangladesh 71st globally among medicine exporters, but production capabilities in complex formulations—including insulin, hormones, anti-cancer medications, metered-dose inhalers (MDIs), dry powder inhalers (DPIs), and lyophilized injectables—suggest upgrading potential toward the top 25 rankings by 2030.

Bangladesh pharmaceutical exports reach 166 countries across seven geographic regions, with Asia and Africa representing nearly 56% of export value. This geographic diversity provides resilience against market-specific shocks

3. Information and Communication Technology: Scaling from Freelance Base

Sector Overview and Structural Composition

Bangladesh’s ICT sector has emerged as a government-designated “Thrust Sector,” encompassing over 1 million freelancers (one of the largest global pools) alongside approximately 500,000 IT professionals in formal employment. The sector’s export composition reflects its stage of development: 87% of ICT exports derive from outsourcing and project-based service work, with limited product development or high-value consulting services. This composition indicates both an opportunity (substantial low-cost labor availability) and a constraint (limited differentiation and pricing power).

FY2024-25 witnessed robust sectoral growth, with IT exports reaching $458.18 million (12.99% year-on-year growth) by March 2025, subsequently climbing to $724.6 million by the fiscal year’s close. This trajectory, while positive, remains far below strategic targets: Bangladesh’s $5 billion export target (established by the Bangladesh Association of Software and Information Services) requires the sector to achieve only 14.5% of its stated goal in FY2024-25, a significant gap relative to Pakistan’s $3.8 billion export performance.

Comparative Competitive Positioning

While Bangladesh’s ICT sector is growing faster percentage-wise (15-20% annually) than India (10-12%), the absolute gap remains substantial. Pakistan’s $3.8B export value demonstrates Bangladesh’s current positioning between frontier and established IT hubs

Bangladesh’s ICT sector growth rate (15-20% annually) outpaces India’s (10-12%) and approaches Pakistan’s (20-25%), yet absolute market size disparities remain vast: India’s $250 billion tech industry dwarfs Bangladesh’s estimated $1.3 billion, with Pakistan’s $3.5 billion occupying an intermediate position. These disparities reflect both historical development pathways and structural constraints in Bangladesh’s sector.

The talent pool demonstrates significant quality variation. Bangladesh produces approximately 10,000 IT graduates annually from universities including BUET, Dhaka University, and private institutions, yet quality alignment with industry needs remains problematic due to outdated curricula and limited industry-academia linkages. Within the existing IT workforce, only 60% possess skilled classifications, with the remainder falling into semi-skilled or non-skilled categories. The sector faces a 40% skills gap in specialized domains including Artificial Intelligence, Internet of Things (IoT), and robotics—areas where global demand is accelerating.

Brain drain constitutes a significant competitive constraint. Superior remuneration and work environments in the Gulf states, Europe, and North America attract Bangladesh’s top talent, reducing the pool of entrepreneurs and senior technologists capable of scaling locally-founded companies. India, by contrast, has developed an ecosystem where talent circulates between venture capital-backed startups and multinational service providers, creating density and knowledge spillovers that Bangladesh has yet to replicate.

Policy Environment and Government Support

The interim government’s “Smart Bangladesh 2041” vision provides strategic direction, supported by fiscal measures including 8% cash incentive schemes and 10-year income-tax holidays for qualified exporters. Bangladesh Bank’s recent decision to permit startups less than 10 years old to invest up to $10,000 abroad for legal entity establishment represents incremental progress, though restrictions persist on established IT firms seeking foreign investment capabilities.

Regulatory gaps create operational friction. Unlike India’s robust IT regulatory framework and Pakistan’s government digitalization initiatives, Bangladesh has not established comprehensive sectoral regulation or developed strategic government procurement preferences for local ICT companies. India’s model of prioritizing local companies in critical national projects (toll management systems, national ID infrastructure, treasury operations) has generated substantial scaling opportunities; Bangladesh has not systematically replicated this approach, leaving billions of public procurement expenditures directed toward international vendors.

Growth Potential and Strategic Requirements

Industry analysis suggests Bangladesh’s ICT sector could achieve $5-7 billion in annual exports within the next decade if three conditions align: (1) regulatory reforms enabling business formation and international transactions, (2) investment in STEM education and specialized training programs, and (3) government procurement preferences for local firms on critical digital infrastructure. The market research projection of $12.07 billion by 2030 appears optimistic relative to current trajectory, requiring sustained policy support and investor confidence restoration.

4. Agro-Processing and Food: Scaling Value Addition on Agricultural Foundation

Sector Overview and Export Composition

Bangladesh’s agro-processing sector represents a critical yet underdeveloped export opportunity, leveraging a strong agricultural base (ranking 2nd globally in jute, goat milk, and jackfruit; 3rd in rice and freshwater fish) into higher-value processed products. FY2024 generated $1.03 billion in total agro-exports, of which processed food contributed $341.73 million—demonstrating that 75% of agricultural production remains unprocessed, representing a substantial value-addition opportunity.

The sector has recorded a 13% compound annual growth rate, with processed food exports specifically expanding at 16.6% annually, substantially outpacing agriculture’s broader growth. First-half FY2025 results showed continued momentum, with agro-export earnings reaching $595.51 million (9.3% year-on-year growth), tracking toward the $1 billion annual target.

Market Access and Domestic Market Dynamics

Bangladesh’s agro-processing exports reach 140+ countries, with 52 markets offering duty-free or preferential access including the EU, Gulf Cooperation Council (GCC), and ASEAN regions. This geographic reach supports diversification beyond traditional RMG destination markets, providing alternative growth vectors less exposed to single-market policy changes.

The domestic market presents equally compelling demand dynamics. Bangladesh’s packaged food market—valued at $47.54 billion in 2022 with a population exceeding 170 million and an emerging middle class of 34 million—is projected to grow at 15.01% annually through 2027. The halal food segment specifically grows at 8-10% annually, aligning Bangladesh with the $2.4 trillion global halal market where authentic sourcing and certification carry premium value.

Product Diversification and Specialization

Bangladesh’s agro-export portfolio includes shrimp and frozen seafood, spices (turmeric, chili), fresh and processed vegetables, dry food, tobacco, and emerging categories including jackfruit (exported to UK, Saudi Arabia, UAE, Kuwait, Italy, Germany, USA, Qatar) and specialty dairy products. This product breadth mitigates single-commodity price volatility while positioning the sector to capture diverse demand segments.

Processing capacity remains constrained by infrastructure and investment limitations. Over 1,000 food processors and 250 exporters operate in Bangladesh, primarily SMEs lacking scale economies and sophisticated processing capabilities. Investment priorities identified by government and industry include sustainable cold chain and storage infrastructure, seed technology, climate-smart agriculture, modern packaging and logistics, and digital agri-tech platforms with IoT-led precision farming and traceability technologies.

Strategic Imperatives

The agro-processing sector’s 16.6% growth rate and large domestic market opportunity position it as a key diversification pillar, particularly given its lower capital intensity relative to pharmaceutical manufacturing or semiconductor assembly. Government policy should prioritize investment in rural cold-chain infrastructure, food safety certification systems aligned with international standards (particularly ISO 22000 for food safety management), and export promotion agencies capable of supporting SME-level producers in meeting international regulatory requirements.

5. Light Engineering and Electronics: Overcoming Skill and Technology Deficits

Sector Overview and Industrial Base

Bangladesh’s light engineering sector, centered in geographic clusters including Dholaikhal and Jinjira (containing approximately 7,500 factories, shops, and workshops employing around 60,000 people) alongside 34 clusters spanning 18 districts, contributes nearly 3% of national GDP. Annual sectoral revenues reach BDT 20,000 crore, with approximately 600,000 workers employed across 40,000 companies producing motor parts, bicycles, motorcycles, household appliances, electrical components, and specialized machinery.

FY2022 export performance reached $796 million, with the sector growing at 10% annually. Product diversity spans industrial machinery, spare parts for transport equipment, bicycles and components (representing $167.95 million exports in FY2022), electrical equipment including switches, cables, generators, and compressors, ferrous and non-ferrous castings, and agricultural machinery.

Structural Constraints and Competitiveness Gaps

Despite significant employment and revenue generation, the light engineering sector remains constrained by critical technology and skill deficits. A 33.6% skill gap across the industry reflects inadequate technical vocational education and training (TVET) infrastructure, while dependence on outdated technology and manual labor generates 30-40% resource wastage in production processes alongside serious worker health risks. Skilled manpower shortages directly undermine sector competitiveness: currently, the industry fulfills only 48-52% of domestic demand while capturing less than 1% of global engineering exports—a position far below Bangladesh’s latent productive capacity.

Import competition from China and other nations becomes particularly acute when domestic production costs increase. VAT disparity between imported light engineering products and locally-manufactured alternatives frequently renders imports cheaper despite Bangladesh’s labor cost advantage, demonstrating that cost-competitiveness depends not solely on factor costs but on overall tax policy coherence.

Market Penetration and Export Potential

Global market penetration remains minimal. Bangladesh currently contributes 0.02% ($56 million) to the United Kingdom’s light engineering imports, indicating vast untapped market opportunity in developed economies where quality and compliance certifications command premium valuations. Regional demand from South Asia and Southeast Asia provides more accessible initial markets, where Bangladesh’s geographic proximity and cultural familiarity support market development.

Domestic electronics and appliances manufacturing has achieved greater success, with television production achieving 90% local market share, demonstrating feasible pathways toward domestic market capture and eventual export development. This television manufacturing success reflects coordinated investment in assembly infrastructure, supply chain development, and brand development by enterprises including Walton Hi-Tech Industries.

Strategic Development Framework

The government’s Light Engineering Industry Development Policy 2022 establishes a strategic framework including raw material banking from the shipbreaking industry, tax incentives, buyback management schemes, and a venture capital fund for supporting entrepreneurs. Additional planned industrial parks in Dhaka, Narayanganj, Bogra, Narsingdi, and Gazipur will provide clustered infrastructure supporting scale-ups from workshop production to factory-level manufacturing.

Critical policy initiatives should emphasize (1) technology upgrading through controlled incentives for equipment investment, (2) TVET curriculum alignment with industry skill requirements, (3) quality certification support enabling market access in regulated sectors, and (4) strategic government procurement supporting infant industries in mature production phases.

6. Infrastructure and Construction: Foundation for Economic Transformation

Megaproject Portfolio and Economic Impact

Bangladesh’s infrastructure investment surge represents the largest development expenditure in the nation’s history, anchored by nine government-designated “fast-track projects.” The flagship Padma Multipurpose Bridge—a 6.15-kilometer structure completed at a cost of $3.6-3.868 billion—exemplifies the scale and ambition of this initiative. Operating since June 2022, the bridge carries 15,000+ vehicles daily and generated approximately 800 crore BDT in toll revenues in its first year, while fundamentally restructuring southwestern Bangladesh’s economic geography by reducing ferry transit time from 15-22 hours to approximately 1 hour via the bridge.

The Padma Bridge’s economic impact is anticipated to reach 1.2-2.5% of national GDP growth, with particular benefits accruing to 21 southern districts that were historically isolated from the Dhaka-Chattogram economic corridor. The southwestern region has experienced accelerated business establishment even before bridge completion, with 17 planned economic zones designed to leverage the improved connectivity for industrial development and trade facilitation. Agricultural and seafood sectors particularly benefit from reduced spoilage during transport and improved market access for perishable products.

The broader fast-track megaproject portfolio includes:

- Dhaka Metro Rail (MRT Line-6): $2.8 billion, with 40% completion, addressing critical urban mobility constraints in Bangladesh’s capital

- Rooppur Nuclear Power Plant: $2.12 billion, representing Russia’s role in diversifying Bangladesh’s power generation mix

- Matarbari Coal-fired Power Plant: $710 million, supporting industrial power requirements

- Bangabandhu Railway Bridge: $2 billion, creating dedicated rail connectivity across the Jamuna River

Additional announced projects include the Dhaka-Ashulia Elevated Expressway, Dhaka-Chittagong high-speed rail, Karnaphuli underwater tunnel (first in South Asia at $1.2 billion), and Cox’s Bazar runway extension.

Funding and Geopolitical Implications

Project financing reveals Bangladesh’s diversified international partnerships: China funds three major infrastructure projects (Padma Bridge Rail Link, Payra Coal-fired power plant, and associated projects), Japan finances the Dhaka Metro Rail and Matarbari deep seaport, Russia implements the nuclear facility, while India contributes select projects. This diversified funding approach has enabled Bangladesh to avoid the debt vulnerabilities that plague some BRI (Belt and Road Initiative) participants, while building comprehensive regional connectivity supporting trade with South Asia, Southeast Asia, and beyond.

Infrastructure Development Framework and Future Trajectory

Bangladesh’s infrastructure investment strategy directly addresses historic deficits in transportation connectivity, energy generation capacity, and port facilities that have constrained industrial competitiveness. The Padma Bridge’s incorporation of utilities including high-pressure gas pipes and telecommunication lines signals integrated infrastructure thinking beyond traditional transportation investment.

However, infrastructure development alone cannot catalyze economic transformation without complementary human capital, regulatory, and sectoral development initiatives. Port expansion and enhanced transportation connectivity require corresponding improvements in customs efficiency, dispute resolution mechanisms, and business regulatory frameworks to translate physical infrastructure into improved export competitiveness.

7. Renewable Energy: Necessity and Aspiration Gap

Strategic Imperative and Current Capacity

Bangladesh faces a critical energy security challenge: the country lacks substantial domestic hydrocarbon resources and remains dependent on imported natural gas, with declining domestic reserves requiring increasing LNG (liquified natural gas) imports to meet power generation needs. From 2018-2025, Bangladesh spent nearly $18 billion on LNG imports—funds that could have delivered approximately 22,000 MW of renewable energy capacity. This expenditure trajectory underscores both the urgency of energy transition and the substantial financial opportunity cost of delayed renewable deployment.

Current renewable energy capacity stands at 1,559 MW, with solar energy dominating at 1,265 MW (81% of renewable capacity), followed by hydropower (230 MW) and wind (63 MW). Bangladesh’s geographic position provides substantial solar resource: the country receives average solar irradiance of 5 kWh/m²/day with 300+ sunny days annually, establishing technical foundations for large-scale solar development.

Policy Targets vs. Implementation Reality

Bangladesh has established ambition renewable energy targets: 20% of electricity generation by 2030 (within the Integrated Master Plan), scaling to 40% by 2041. However, these targets are not currently achievable under business-as-usual scenarios. If current deployment trajectories continue, renewables will represent only 4% of electricity generation by 2030, with solar reaching merely 2.4 GW (compared to ambitious 6-16 GW targets depending on scenario).

Government initiatives including a 10-year tax exemption for renewable energy companies, 3,000 MW rooftop solar initiatives, and tendering for 5,238 MW of solar projects represent genuine policy momentum. The first private-sector solar facility—a 100 MW grid-connected plant financed by the Asian Development Bank at Dynamic Sun Energy Private Ltd in Pabna—demonstrates bankable project economics when policy frameworks provide certainty.

However, project delays and cancellations have shaken investor confidence. In a major setback, the government suddenly cancelled 37 solar Independent Power Producer (IPP) projects totaling 3,000 MW, while rigid pricing caps and policy reversals have rendered many projects economically unviable. These policy inconsistencies create regulatory risk that discourages foreign and domestic private investment essential for scaling renewable deployment beyond government-financed projects.

Financing Gap and Investment Requirements

The financing constraint is not absolute capital availability but rather political commitment to renewable energy prioritization. Development banks including the ADB and World Bank have demonstrated willingness to finance renewable projects at concessional terms, with the ADB’s $121.55 million financing package for Dynamic Sun Energy exemplifying bankable renewable infrastructure. Reallocating even a portion of the $18 billion spent on LNG imports toward renewable capacity would fundamentally transform the energy landscape.

Implementation Priorities

Critical policy measures should include: (1) ensuring bankable power purchase agreements with transparent, cost-reflective tariff-setting mechanisms, (2) implementing fast-track permitting procedures for renewable projects, (3) establishing fiscal incentives (accelerated depreciation, investment tax credits) for renewable energy and battery storage technologies, (4) prioritizing rooftop solar on government buildings as demonstrated in the ongoing solar panel installation program, and (5) exploring innovative land-use approaches including agri-voltaics (combining agricultural production with solar generation) to address land scarcity constraints.

Cross-Cutting Economic Constraints and Macroeconomic Context

Growth Deceleration and Inflation Pressures

Bangladesh’s macroeconomic environment has deteriorated substantially from the 6-7% growth rates achieved in the 2010s. Fiscal year 2024-25 witnessed GDP growth projections of 3.3-3.9% (Asian Development Bank) or 4.0-5.0% (Bangladesh Bank), compared with 4.2% in FY2024 and 1.8% in Q4 2024. This deceleration reflects multiple headwinds: political transition disruptions, weak private and public investment, trade disruptions, and persistent inflationary pressures.

Inflation has emerged as the primary concern for 40% of surveyed economists. Headline inflation reached 9.7% in FY2024, with projections exceeding 10.2% in FY2025. Contributors include Taka depreciation against major currencies (raising import costs), supply chain constraints in wholesale markets, inadequate market information systems, and labor unrest in the RMG sector disrupting production and creating supply shortages.

Private Investment Collapse and FDI Inadequacy

Foreign direct investment, while rebounding to $1.71 billion in FY2024-25 (20% year-on-year growth), remains substantially below levels required to sustain high-growth development. Bangladesh requires approximately $8 billion in annual FDI to achieve 1% incremental GDP growth and progress toward high-income country status; current inflows of $1.5-3 billion fall far short of this requirement. Moreover, much recorded FDI represents reinvestment by existing operators rather than greenfield investment by new entrants, indicating limited business environment attractiveness to fresh investors.

The first quarter of 2025 witnessed FDI surging to $864.63 million—double the previous quarter—driven by sharp increases in intra-company loans and strong equity investments, suggesting that market sentiment may have begun improving following political stabilization. However, this volatility underscores continuing investor uncertainty regarding the overall business environment.

Strategic Imperatives for Post-LDC Transition

Export Diversification as Existential Imperative

Bangladesh’s LDC graduation in November 2026 represents a watershed moment that demands strategic action across all sectors. The sector faces four critical competitive imperatives:

Bangladesh faces substantial tariff increases post-LDC graduation in 2029, with RMG sector facing 7-12% tariffs in major markets except the UK. This transition necessitates urgent competitiveness improvements in cost structure, sustainability compliance, and product value addition

- Tariff Mitigation through Non-Price Competitiveness: The 7-12% tariff increases on RMG exports to major markets cannot be offset through further labor cost reduction. Instead, Bangladesh must advance through sustainability compliance, faster delivery timelines, and sophisticated supply chain coordination. The EU’s Corporate Sustainability Due Diligence Directive requirements necessitate substantial capital investment in factory monitoring, worker welfare programs, and supply chain transparency systems that currently differentiate only 15% of Bangladesh’s apparel units.

- Product Upgrading and Vertical Integration: Current exports concentrate in basic knit and woven apparel categories. Bangladesh must accelerate diversification toward man-made fiber (MMF) products where global demand is shifting, higher-value technical textiles, and integrated supply chains encompassing yarn, fabric, and finished garment production. Vietnam’s competitive success reflects precisely this vertical integration strategy, reducing unit costs through in-house fabric and yarn production.

- Pharmaceutical Self-Sufficiency in APIs: The industry’s continued reliance on imported APIs creates critical vulnerability post-LDC graduation. Urgent investment in API Industrial Park completion, with concurrent regulatory streamlining of solvent intermediate approvals and applied R&D support, is essential. Government commitment to off-take commitments for API products would provide revenue certainty enabling private investment.

- ICT Sector Scaling from Services to Products: Bangladesh’s freelancer base and outsourcing capabilities provide a foundation, but scaling to $5+ billion in annual exports requires coordinated investment in startup ecosystems, government procurement preferences for local digital services, and technical education alignment with emerging technology stacks (AI, cloud architecture, cybersecurity).

Foreign Direct Investment as Growth Accelerator

The FDI deficit represents both a constraint and an opportunity. Bangladesh must systematically improve factors that international investors evaluate:

- Energy security: Address power shortages and grid reliability constraints that deter energy-intensive manufacturing

- Logistics efficiency: Reduce domestic transportation costs and customs processing times that increase production lead times

- Political stability: Demonstrate institutional continuity and rule of law independence from political cycles

- Regulatory predictability: Establish consistent policy frameworks (particularly in renewable energy, pharmaceutical manufacturing, and digital infrastructure) that enable long-term investment planning

- Sector-specific incentives: Target FDI in priority diversification sectors (advanced textiles, pharmaceuticals, electronics) through selective fiscal incentives and infrastructure support in industrial parks

Vietnam’s success in attracting $36 billion in FDI commitments in 2024 and India’s $28 billion achievement, compared to Bangladesh’s $1.71 billion, reflect not superior natural resources but more robust business environment fundamentals and political commitment to investor confidence.

Geographic Market Diversification

Bangladesh’s RMG exports to non-traditional markets (Africa, Middle East, Asia beyond India) represent only 16% of total apparel exports. Strategic bilateral and regional trade agreements—following Turkey’s model of securing preferential access in African and South American markets—could expand market opportunities and reduce dependence on EU tariff policy changes.

Conclusion: Transformation or Stagnation at the Inflection Point

Bangladesh’s economic sectors present a portrait of an economy at an inflection point. The RMG sector that generated 80%+ of export earnings and launched Bangladesh’s industrial development now confronts structural headwinds requiring fundamental competitiveness improvements beyond cost competition. Simultaneously, emerging sectors including pharmaceuticals (targeting $1 billion exports by 2030), ICT (pursuing $5-7 billion export targets), and agro-processing (growing at 16.6% annually) provide pathways toward more diversified, resilient export structures less dependent on single markets or wage-cost arbitrage.

LDC graduation in November 2026 creates urgency: the grace period until 2029 provides a window for competitiveness adjustment before full tariff impacts materialize. Bangladesh’s infrastructure investments—anchored by the transformational Padma Bridge—establish physical foundations for improved regional trade connectivity and southwestern industrialization.

Success requires coordinated policy action spanning energy security (accelerating renewable deployment), export competitiveness (advancing RMG sustainability and product upgrading), sectoral development (completing pharmaceutical API Industrial Park, establishing ICT regulatory framework), and investment climate (improving business environment attractiveness). The historical data confirms Bangladesh’s capacity for structural transformation: the RMG sector grew from negligible base to 8% of global apparel trade over four decades; pharmaceutical industry evolved from multinational dominance to 98% domestic self-sufficiency in two decades.

The question confronting Bangladesh’s policymakers is whether these historical lessons can be accelerated and replicated across priority sectors before the tariff cliff of 2029 eliminates the margin for strategic adjustment.

official bangladesh government websites

| Bangladesh Export Promotion Bureau | Bangladesh Export Promotion Bureau |

| Bangladesh Investment Development Authority | Bangladesh Investment Development Authority |

Read more country case studies done before this.

| Qatar | Qatar |

| iran | iran |

| china | china |

| Indonesia | Indonesia |

| hong kong | hong kong |

| japan | japan |

| sinagpore | singapore |

| taiwan | taiwan |

| uAE | UAE |

| vietnam | vietnam |

| saudi arbia | saudi arbia |

| Malaysia | Malaysia |

| india | india |

| south korea | south korea |

Okfungame is good, I enjoy playing game in okfungame. Site have many game for you to choose. If you want try, visit at: okfungame