China has undergone a transformative economic shift over the past decade, evolving from a low-cost manufacturing hub into a global powerhouse in high-technology innovation. This transition, driven by deliberate government policy, massive capital deployment, and a vast domestic market, has positioned the nation as a formidable competitor across critical technology sectors including artificial intelligence, electric vehicles, semiconductors, digital payments, and biotechnology. The emergence of 369 unicorn companies—representing 25% of the world’s total—and the concentration of five innovation hubs in the top global rankings underscore the ecosystem’s maturity and dynamism. This case study examines the structural drivers, sectoral achievements, policy mechanisms, and competitive positioning that define China’s technology-driven growth.

china The Architecture of Government-Backed Industrial Transformation

China’s economic modernization reflects a coordinated, whole-of-government strategy anchored in the “Made in China 2025” (MIC25) initiative launched in 2015. Although the branding was de-emphasized after international criticism in 2018, the core objectives persist through alternative frameworks such as the 14th Five-Year Plan and sector-specific directives. The policy framework rests on four foundational pillars: indigenous innovation, technological self-sufficiency, global competitiveness in strategic sectors, and supply chain resilience.

Government financial support has intensified substantially. Tax benefits for innovation surged at an average annual rate of 28.8% between 2018 and 2022, with the proportion of companies enjoying R&D deductions and tax reductions quadrupling from 2015 to 2023. State-guided investment funds (GGFs), which grew five-fold between 2015 and 2020, have become the primary vehicle for channeling capital into priority sectors. The third phase of the National Integrated Circuit Industry Investment Fund (the “Big Fund”), launched in 2024, represents $47.5 billion in capital allocation for semiconductor advancement, while a dedicated $8.2 billion AI investment fund was established in January 2025.

Beyond direct financial instruments, the government leverages preferential tax policies, reduced corporate tax rates for high-tech firms, VAT exemptions, and conditional market access—mechanisms that systematically favor domestic enterprises while pressuring foreign companies to localize production to maintain market access. This combination has created what economists term “soft budget constraints” for state-backed firms, enabling them to sustain losses, scale rapidly, and maintain artificially competitive pricing across export markets.

china Electric Vehicles: Market Dominance and Export Leadership

China’s electric vehicle sector exemplifies the policy framework’s effectiveness in creating competitive advantage within capital-intensive, state-supported industries. The EV market reached $413.4 billion in 2024 and is projected to expand to $1.3 trillion by 2032, representing a compound annual growth rate of 14%.

China EV Market Size Projection (2024-2032)

The sector’s explosive growth reflects both domestic demand and government policy support. EV sales surged to 11 million units in 2024, a 40% increase year-over-year, while capturing 51% of all new car sales in 2025. BYD emerged as the world’s leading EV manufacturer by revenue in 2024, displacing Tesla, while other Chinese manufacturers including Nio and Li Auto established significant market positions. These achievements rest on $230 billion invested in EV development from 2009 to 2023—capital mobilized through government subsidies, favorable credit terms, and procurement mandates.

Global export penetration has accelerated rapidly. China surpassed Japan in 2023 to become the world’s leading vehicle exporter, with electric vehicles constituting approximately 41% of domestic production. Chinese EV manufacturers benefit from a comprehensive ecosystem: advanced battery supply chains (dominated by CATL, a state-supported producer), subsidized charging infrastructure exceeding 5.2 million chargers, government incentives for consumer purchases, and trade policies restricting foreign competition.

china Semiconductor Industry: Ambitious Targets Meet Technical Barriers

The semiconductor sector reveals both the ambitions and constraints of China’s industrial policy. MIC25 targeted 70% self-sufficiency by 2025; actual achievement reached approximately 30%, exposing the gap between policy aspiration and technological reality. This disparity stems from the sector’s extreme technical complexity, where advanced nodes (7nm and below) remain inaccessible to Chinese manufacturers due to US export controls and the capital-intensive nature of foundry development.

China’s Semiconductor Self-Sufficiency: Target vs. Actual (2025)

Despite this shortfall, the sector has advanced meaningfully. China achieved approximately 50% self-sufficiency in semiconductor equipment by 2025 (from 13.6% in 2024), driven by massive state investment and targeted support for domestic champions including Semiconductor Manufacturing International Corporation (SMIC), Yangtze Memory Technologies Corporation (YMTC), and ChangXin Memory Technologies (CXMT). The most dramatic progress occurred in compound semiconductors: China provided 80% of global gallium supplies and dominated SiC (silicon carbide) wafer production, capturing over 50% of global supply in 2024 compared to 5% historically. These materials are essential for electric vehicles and 5G infrastructure, illustrating how strategic self-sufficiency in foundational technologies cascades across downstream industries.

Corporate-backed semiconductor funding reached record levels in early 2025, with 18 chip technology startups receiving funding in February 2025 alone—the highest monthly total in two years. This surge reflects intensified capital deployment in response to US-China trade tensions and the government’s determination to reduce technological dependencies.

china Artificial Intelligence: Rapid Capability Building and Strategic Prioritization

China’s AI sector has emerged as a global competitive force, with investment tripling from 2023 to 2025. Total AI spending reached $98 billion in 2025, up 48% from 2024, with 57% financed directly by the government (¥56 billion or approximately $7.8 billion), demonstrating the state’s central role in capability building.

China’s AI Investment Breakdown by Source (2025, $98B Total)

Major technology companies are reinforcing state investment. Alibaba unveiled a $53 billion three-year capital expenditure plan targeting AI computing infrastructure in February 2025, while Tencent’s capital expenditure nearly quadrupled year-over-year in Q4 2024 to $5.1 billion, substantially redeployed toward AI infrastructure. DeepSeek’s emergence as a cost-efficient alternative to Western AI models energized the ecosystem, signaling that Chinese firms can achieve technological parity through algorithmic innovation rather than purely through semiconductor advantages.

The government allocated specific budgets across AI-related domains: ¥145 billion for the National AI Development Plan (core research and chip development), ¥89 billion for Smart City Infrastructure (urban AI deployment and IoT integration), ¥67 billion for AI Healthcare Initiative (medical AI and drug discovery), and ¥44 billion for Industrial AI Modernization (manufacturing automation and supply chain optimization). This sectoral focus reflects strategic decisions about where AI applications offer the highest economic and security value.

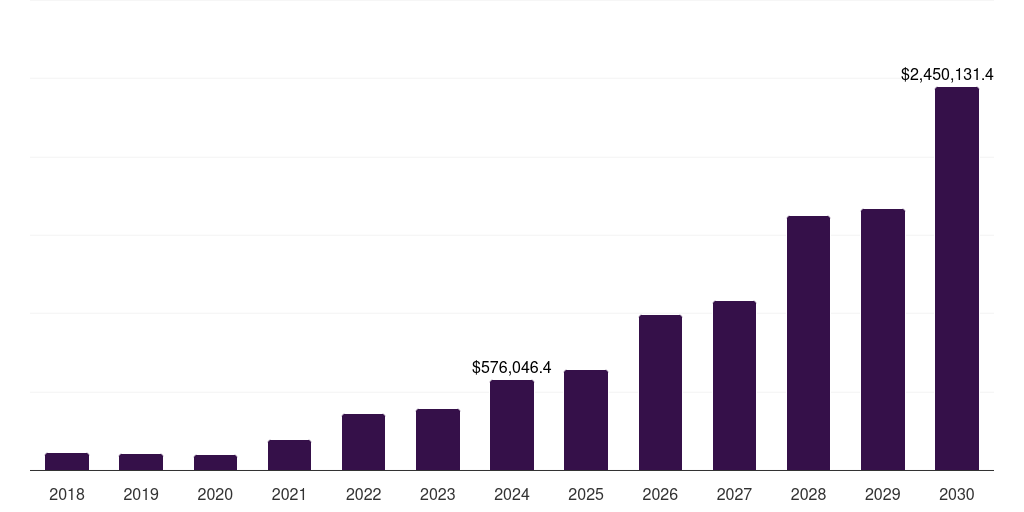

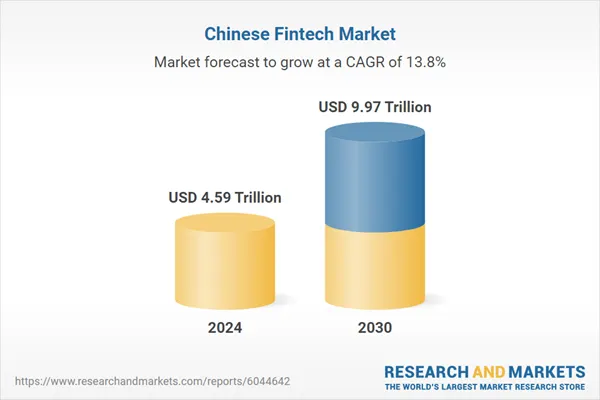

china Digital Payments and Fintech: A Mature Ecosystem at Scale

China’s fintech sector represents a mature, state-of-the-art digital financial ecosystem that has leapfrogged legacy banking infrastructure. The fintech market was valued at $51.28 billion in 2024 and is projected to reach $107.55 billion by 2030 at a CAGR of 13.8%. However, the broader digital payments market—the dominant fintech subsector—dwarfs this figure, reaching $1.53 trillion in 2025 and projected to reach $2.52 trillion by 2030.

China Fintech & Digital Payments Market Growth (2024-2030)

This market scale reflects extraordinary adoption rates. As of June 2023, 943.19 million Chinese adults maintained online payment accounts (an increase from 904.44 million in June 2022), representing an 87.5% utilization ratio among internet users. In 2023, China processed 531.087 billion bank card transactions valued at $153.54 trillion—a 17.51% increase in transaction volume and 7.23% growth in value compared to 2022.

The payment ecosystem’s trajectory demonstrates dominance by integrated mobile wallets. Alipay and WeChat Pay together command the majority of transaction value, with digital wallets accounting for 82% of e-commerce transaction value in 2024 and projected to reach 86% by 2027.

China E-Commerce Payment Method Shift (2024-2027)

The government’s Digital Currency Electronic Payment (DCEP) initiative further advances this infrastructure. By June 2023, digital yuan transactions reached 1.8 trillion yuan ($249.33 billion), up from 360 million cumulative transactions by August 2022, demonstrating official digital currency adoption acceleration.

E-Commerce: Scale, Innovation, and Mobile-First Architecture

China’s e-commerce market epitomizes the convergence of technology infrastructure, consumer adoption, and government policy. The market reached $1.53 trillion in 2025, equivalent to nearly half of global online retail volume, and is projected to grow to $2.52 trillion by 2030. This trajectory reflects sustained 10-11% compound annual growth despite mature market conditions in tier-1 cities (Beijing, Shanghai, Guangzhou, Shenzhen all exceed 99% internet penetration).

Growth is increasingly driven by lower-tier cities and rural expansion. Third- and fourth-tier urban centers recorded 5.8% spending growth in 2024, outpacing tier-1 cities, while rural markets added 304 million internet users and $97.38 billion in annual e-commerce sales, signaling a vast expansion frontier. Cross-border e-commerce remains vibrant, with 2024 import-export volume estimated at $370 billion, supported by consolidated manufacturing clusters in Guangdong, Zhejiang, Fujian, and Jiangsu provinces.

Mobile commerce dominance is absolute: smartphones and tablets captured 68% of 2024 transactions, with 99.7% of Chinese internet users accessing services via mobile devices. This infrastructure advantage—enabled by ubiquitous 5G, 4G networks, and integrated digital wallets—has become a fundamental economic moat. The merchant ecosystem is highly sophisticated, with platforms like Pinduoduo ($715.2 billion 2024 revenue), Alibaba’s Taobao/Tmall ecosystem, and JD.com offering AI-driven recommendation engines, livestream shopping integration, and frictionless transaction experiences.

Biotech and HealthTech: Capital Deployment Toward an Aging Population

China’s biotech and healthcare technology sectors are expanding rapidly, driven by demographic urgency (China’s aging population exceeded 12% of the total by 2020) and strategic government prioritization. The sector attracted multiple unicorn-scale funding rounds in 2025. Notable transactions included Minghui Pharmaceutical’s $131 million pre-IPO round in August 2025, and Abogen Biosciences’ historic $1.4 billion in cumulative funding for RNA-based therapeutics development.

Government investment in AI Healthcare Initiative ($67 billion) and policy measures including fast-tracked drug approval processes and enhanced intellectual property protections have accelerated innovation. Chinese biotech firms have progressed from primarily serving domestic markets toward developing globally competitive candidates. For instance, firms are advancing therapies in oncology, immunology, and infectious diseases, with several candidates receiving IND (Investigational New Drug) approvals in both China and the United States.

However, this sector still lags Western competitors in cutting-edge therapeutics. Overall healthcare startup fundraising declined in 2024 despite government support, reflecting structural challenges in achieving capital efficiency and clinical validation for breakthrough medicines. The sector’s future growth depends on translating government financial support into genuine therapeutic innovation rather than duplicative development efforts.

Innovation Clusters and Global Competitiveness

China has established itself as a global innovation power through the concentration of innovation clusters and rising patent output. According to the 2025 Global Innovation Index, China ranks 10th globally for the first time, becoming the only middle-income economy in the top 10. More significantly, China hosts 24 of the world’s top 100 innovation clusters—more than any other nation—including Shenzhen–Hong Kong–Guangzhou (now ranked 1st globally) and Beijing, both hotspots for patents, science, and increasingly, venture capital activity.

The distribution of global startup ecosystem rankings reflects China’s multi-hub approach. Beijing ranks 5th globally, Shanghai ranks 10th (and is the fastest-growing major hub with 38.4% growth), Shenzhen ranks 17th (gaining 11 positions), Hangzhou ranks 23rd (gaining 13 positions), and Guangzhou ranks 35th (gaining 6 positions).

China’s Global Startup Ecosystem Rankings by Hub (2024-2025)

This geographical decentralization contrasts with Western concentration in single metros (San Francisco, New York) and reflects deliberate government encouragement of regional innovation ecosystems. Local governments in Shanghai, Shenzhen, Chengdu, and Hangzhou implement customized startup packages including seed funding, preferential tax treatment, talent visa facilitation, and R&D subsidies tailored to sector focus.

China leads globally in patent filings, trademarks, utility models, and industrial designs, with patent share gains exceeding 4 percentage points in electric vehicles, new materials, electronics, and robotics. In global publications of scientific output, China’s share increased by an average of 18 percentage points between 2015 and 2023 across most sectors, a trajectory that accelerated following MIC25 adoption. However, analysis of quality-weighted metrics (top-cited publications) reveals that while China has narrowed gaps with Western competitors, the U.S. and European institutions still lead in fundamental research breakthroughs.

Startup Ecosystem Maturity and Capital Flows

The startup ecosystem achieved significant scale. China generated 32 million new business entities in 2024, with 11,500+ registered startups across major technology sectors, and achieved 369 unicorn valuations representing 25% of the global total. Venture capital funding reached $40.2 billion in 2024, substantially exceeding India’s $13.7 billion and reflecting China’s position as the second-largest VC market globally after the United States.

Corporate-backed funding rounds accelerated in early 2025, reaching 374 in February—a 21% increase compared to February 2024. The IT sector captured disproportionate attention, with 34 funding rounds in IT subsectors in February 2025, driven by semiconductor and AI investments. Notably, foreign direct investment cautiously returned through alternative channels (Hong Kong and the Hainan Free Trade Port), after declining during regulatory tightening in 2020-2023.

Private equity and venture capital investors have recalibrated investment criteria toward Series A and B rounds demonstrating clear paths to profitability, reflecting maturation of the investment landscape and lessons learned from previous market cycles characterized by high cash burn and delayed exits.

Policy Framework: Integration of Financial and Regulatory Tools

The government‘s approach extends far beyond direct subsidies to encompass an integrated ecosystem of financial instruments and regulatory mechanisms. These include:

State-Guided Investment Funds (GGFs): These public-private vehicles grew five-fold from 2015 to 2020, channeling capital into MIC25 priority sectors. The evolution from traditional subsidies to indirect guidance through GGFs enabled the government to scale capital deployment while maintaining plausible deniability regarding discriminatory state support.

Tax and Fiscal Innovation: Beyond traditional tax reductions, mechanisms such as the “super deduction of R&D expenses” (allowing firms to claim 200% of qualifying R&D costs as deductions) provided accelerated tax relief for innovation-focused enterprises. The scale of these mechanisms—affecting over 75% of listed companies by 2023—made them economy-wide tools for resource reallocation.

Procurement Mandates and Market Access Conditions: Government and state-enterprise procurement policies explicitly favor domestic suppliers in strategic sectors. Joint venture requirements and technology transfer conditions imposed on foreign firms seeking market access created forced knowledge diffusion from multinationals to Chinese competitors.

Human Capital Acquisition: The “Haigui” (return of sea turtles) initiative provides visa facilitation, residency support, and hiring subsidies for foreign-trained engineers and scientists, enabling rapid talent acquisition. This mechanism has attracted thousands of Chinese scientists working abroad to repatriate and establish ventures.

Intellectual Property Acceleration: Fast-track patent and trademark registration, combined with strengthened enforcement mechanisms, reduced the time-to-protection for Chinese innovators, accelerating commercialization velocity relative to Western competitors navigating slower bureaucratic processes.

Enabling Conditions: Infrastructure, Market Scale, and Competitive Culture

Beyond policy, China’s startup ecosystem benefits from structural conditions that would be difficult for competitors to replicate:

Massive Domestic Market: A population of 1.4 billion provides an unparalleled testing ground for new technologies and business models. Companies can achieve scale without international expansion, enabling rapid iteration and capital efficiency superior to startups dependent on global distribution from inception.

Advanced Digital Infrastructure: 5G and 4G coverage exceeding 99% in urban areas, cloud computing capacity comparable to or exceeding Western providers, and fiber-optic backbone infrastructure create low-latency, high-bandwidth environments for digital services development. Broadband penetration, smartphone adoption (99.7% among internet users), and integrated payment infrastructure reduce friction for digital service adoption.

Supply Chain Integration: Clustering of manufacturing in specific regions (Guangdong electronics, Zhejiang e-commerce, Jiangsu semiconductors) enables cost-effective prototyping and rapid scaling. Battery manufacturing (dominated by CATL, BYD subsidiary companies), semiconductor packaging (JCET), and consumer electronics production create backward-integrated supply chains unavailable to competitors.

Fast Technology Adoption: Chinese consumers rapidly adopt new business models and payment methods. Contactless payments, livestream shopping, and mobile-first service design achieved adoption rates and sophistication levels in China 5-7 years ahead of Western markets, creating a testing ground for innovations that subsequently scale globally.

Venture Capital Ecosystem Growth: While historically lagging the U.S. in private innovation finance, China now ranks 2nd globally in late-stage VC deals and 3rd among top corporate R&D investors, with major tech companies (Tencent, Baidu, Alibaba, Lenovo) deploying corporate venture capital to acquire technologies and startups.

Challenges and Structural Headwinds

Despite achievements, the ecosystem faces material constraints:

Semiconductor Gap Persistence: The 40-percentage-point shortfall between the 70% self-sufficiency target and 30% actual achievement highlights the technical barriers to replicating Western semiconductor capabilities. Advanced node production (5nm and below) remains inaccessible, and US export controls on lithography equipment and design tools have created structural dependencies that cannot be overcome through financial investment alone in a 10-year timeframe.

EV Sector Overcapacity: Generous government support has incentivized excess capacity in EV and battery manufacturing. August 2025 saw EV/hybrid sales growth slow to its lowest in 18 months as price wars intensified and government attempted to regulate the sector toward profitability. This pattern—characterized by overinvestment in capacity followed by brutal margin compression—echoes earlier cycles in sectors including solar panels, steel, and cement.

Regulatory Uncertainty: Sudden policy shifts in education technology (tutoring bans), fintech (lending regulations), and internet platforms (data protection rules) have created significant losses for investors and entrepreneurs, reducing confidence in government predictability. The opacity around national security reviews and technology screening creates additional investment friction.

Founder Stress and Market Maturity: Recent reports indicate that while new startups continue forming at massive scale, founder distress from personal debt obligations and investor disputes has increased, suggesting market maturation and reduced “easy money” conditions. Venture funding availability has contracted from peak 2021 levels, though recent emphasis on AI and semiconductors has partially offset this decline.

Global Backlash and Trade Friction: Rising protectionism from the U.S., EU, and other markets in response to Chinese export surges and perceived technology theft has created barriers to market access. Increased tariffs, investment screening, and technology export restrictions limit the global expansion pathways historically available to Chinese companies.

Comparative Global Position and Future Trajectory

China’s position within the global innovation hierarchy reflects recent rapid advancement. The Global Innovation Index 2025 ranking of 10th represents the culmination of consistent policy-driven investment and execution. More telling, China ranks 1st globally in Knowledge and Technology Outputs, 2nd in business-financed R&D and late-stage VC deals, and 3rd among top corporate R&D investors. These metrics indicate that while China has not yet achieved leadership in all innovation dimensions, its private sector is increasingly driving technological advancement rather than relying exclusively on state subsidies.

The analysis from the Rhodium Group’s assessment of MIC25 reveals that Chinese firms have achieved genuine technological leadership in several domains: electric vehicles (commanding 58% of global sales), solar energy (establishing dominant supply chains), green shipping technology, and LiDAR sensors for autonomous vehicles. However, gaps persist in cutting-edge semiconductors, commercial aircraft, high-end medical devices, and biotechnology, where foreign companies maintain 10+ year leads.

The convergence of strengths in foundational technologies (advanced materials, AI, semiconductor packaging) with applications in downstream industries (robotics, autonomous vehicles, industrial automation) creates a “reinforcing effect” that is accelerating innovation across sectors. This multiplier effect—where progress in AI enables breakthroughs in robotics and autonomous vehicles, which in turn accelerate demand for SiC semiconductors and advanced materials—suggests China’s competitive advantages will deepen over the 2025-2035 period, particularly if supply chain resilience improves.

Conclusion: A Transformed Economic Model

China’s transition from manufacturing hub to technology-driven innovation economy reflects a coordinated, decade-long effort integrating direct subsidies, indirect financial instruments, regulatory barriers, market access conditions, and human capital acquisition. The emergence of 369 unicorns, five globally-ranked innovation clusters, and leadership positions in electric vehicles, digital payments, and artificial intelligence demonstrates the model’s effectiveness at achieving scale and capability in targeted sectors.

Yet the $47.5 billion semiconductor funding gap between targets and actual achievement, overcapacity in EVs, and persistent regulatory uncertainty reveal the model’s limitations. Bleeding-edge technologies—advanced node semiconductors, aircraft engines, cutting-edge therapeutics—remain beyond reach despite massive investment, indicating that industrial policy alone cannot overcome 15-20 year technical and knowledge gaps.

The broader concern from an economic efficiency perspective is that the emphasis on industrial policy has contributed to total factor productivity stagnation, debt-to-GDP ratios exceeding 280%, and structural imbalances favoring producers over consumers. These inefficiencies may eventually constrain growth rates, though near-term momentum in AI, green energy, and electric vehicle exports will likely sustain elevated competitiveness through 2030.

For policymakers and strategists globally, China’s experience offers critical lessons: sustained, coordinated industrial policy can build competitive capability in capital-intensive, scale-dependent sectors where technological maturity permits. However, the model struggles with fundamental research, small-team breakthroughs, and sectors where regulatory capture or monopolistic incumbent power constrains new entrants—characteristics that define cutting-edge innovation. China’s future trajectory depends on whether it can transition from replicating proven technologies to generating novel breakthroughs, a challenge that no middle-income country has yet fully overcome at this scale and complexity level.