Hong Kong’s

Hong Kong financial services sector 2026.

Hong Kong maintains its position as one of the world’s premier international financial centers, anchored by unparalleled capital market depth, global banking presence, and increasingly, sophisticated fintech innovation. With a nominal GDP of approximately $381.4 billion USD (2024) and a population of 7.5 million, Hong Kong punches far above its weight as a global financial hub—hosting over 70 of the world’s top 100 banks, commanding 20%+ of global offshore Chinese renminbi (RMB) trading, and emerging as Asia’s leading digital assets and fintech center. This comprehensive case study examines Hong Kong’s economic structure, competitive advantages, evolving fintech ecosystem, and trajectory through 2025-2030. Hong Kong financial services sector 2026.

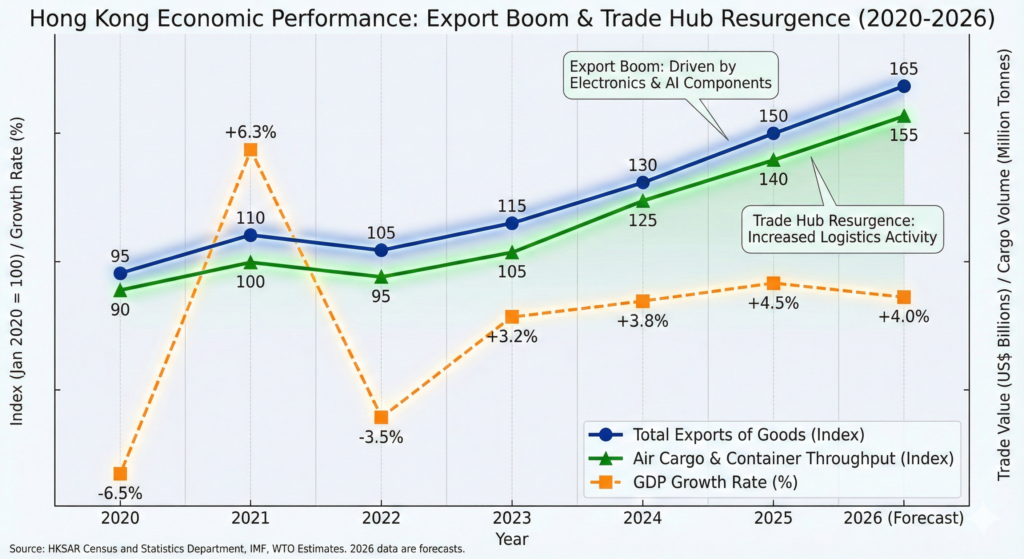

hong kong Economic Performance: Export Boom and Trade Hub Resurgence

Hong Kong’s economic trajectory through 2024-2025 reflects a dramatic reversal from pandemic-era stagnation toward robust expansion, primarily driven by trade dynamics and financial services revitalization.

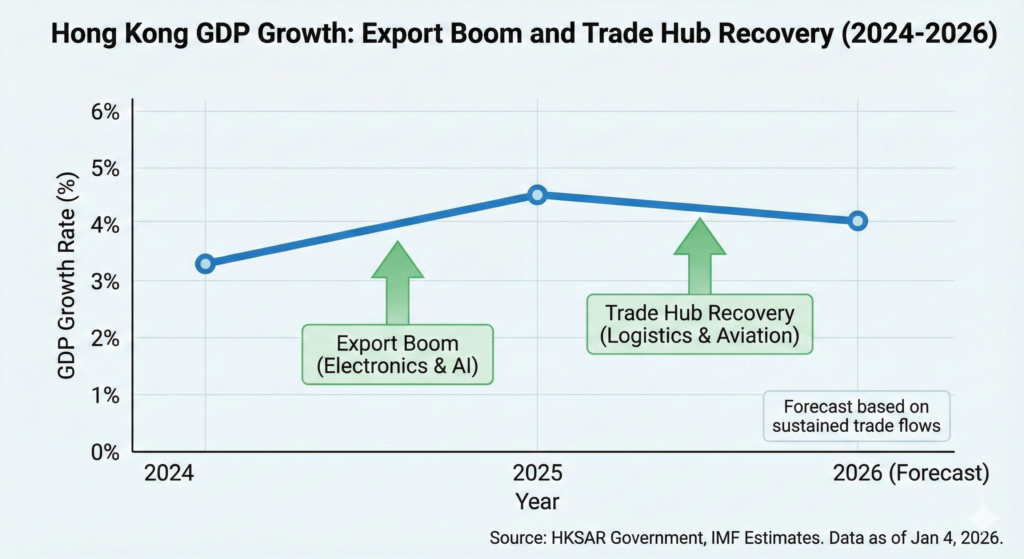

Hong Kong GDP Growth: Export Boom and Trade Hub Recovery (2024-2026)

2024 Performance: Real GDP grew 2.5% in 2024, a respectable pace reflecting recovery from 2023’s weak 2.8% contraction driven by geopolitical tensions and tourism challenges. The year marked Hong Kong’s gradual return to moderate growth as China-Hong Kong tourism normalized.

2025 Acceleration: Hong Kong’s 2025 performance significantly exceeded forecasts. Q1 recorded 3.0% year-over-year growth, Q2 accelerated to 3.1%, and Q3 surged to 3.8%—the fastest quarterly growth since Q2 2021. Full-year 2025 growth has been revised upward to 3.2% (from initial 2%-3% forecast), driven by three factors:

- Export Surge from Rush Shipments: Anticipating US tariffs on Taiwanese and Chinese goods (20% announced for January 2026), importers placed advance orders in Q2-Q3 2025, artificially boosting Hong Kong’s re-export and entrepôt trade volumes.

- Tourism Rebound: Inbound tourism surged as China-US trade tensions temporarily eased and cross-border travel normalized, revitalizing hospitality and retail sectors.

- Financial Services Expansion: Stock market activity rebounded with Hong Kong’s Hang Seng Index performing strongly, and cryptocurrency/digital asset trading volume surged following Hong Kong’s positioning as Asia’s crypto hub.

2026 Outlook: Growth is projected to decelerate to 2.5% as tariff implementation reduces rush-shipment demand and normal trade patterns resume. However, sustained global economic growth and Hong Kong’s structural advantages should prevent sharper contraction.

Structural Economic Composition: Services dominate, representing 93.2% of GDP, with financial services accounting for 17.6%, wholesale/retail for 13.5%, and tourism/hospitality for 8%. Manufacturing represents only 0.9% of GDP, reflecting Hong Kong’s transformation into a pure services and financial hub.

hong kong Financial Services: The Foundation of Hong Kong’s Economic Power

Hong Kong’s global financial centrality is unmatched among Asia-Pacific cities. The city hosts over 70 of the world’s top 100 banks, over 29 multinational bank regional headquarters, and commanding positions in securities trading, asset management, insurance, and derivatives markets.

Banking System Scale: Major banks (HSBC, Standard Chartered, Bank of China, Bank of Communications) maintain substantial operations, with total banking sector assets exceeding $2.5 trillion HKD (approximately $321 billion USD). The banking system’s stability, capital adequacy, and regulatory oversight exceed most global peers, earning AAA sovereign credit rating.

Capital Markets: Hong Kong Exchanges and Clearing (HKEX) operated one of the world’s most liquid securities markets, with the Hang Seng Index incorporating 300+ of Asia’s largest companies. While Shanghai and Shenzhen now handle higher trading volume, Hong Kong remains critical for offshore trading of Chinese equities, convertible bonds, and structured products.

Offshore RMB Center: Hong Kong dominates offshore renminbi trading, clearing 20%+ of global RMB transactions. This strategic position creates stickiness: multinational corporations, asset managers, and central banks conduct RMB transactions through Hong Kong’s banking system, creating network effects difficult for competitors to displace.

Wealth Management and Asset Management: Hong Kong hosts over 2,000 asset management companies managing approximately $2.3 trillion in assets under management. The city’s role as gateway to China, English language proficiency, and regulatory framework position it as the premier wealth management hub for ultra-high-net-worth individuals and family offices focused on Asia.

hong kong Fintech Ecosystem: From “Fintech 2025” to “Fintech 2030”

Hong Kong’s fintech transformation has accelerated remarkably through government strategy, regulatory innovation, and private capital deployment. The Hong Kong Monetary Authority’s (HKMA) “Fintech 2025” strategy (announced June 2021) catalyzed ecosystem development. The recent unveiling of “Fintech 2030” (November 2025) represents a comprehensive long-term vision for the 2025-2030 period.

Fintech Companies and Market Scale: As of July 2024, Hong Kong boasted 1,100+ fintech companies—among the highest globally relative to population. The fintech market is projected to reach $606 billion in revenue by 2032 (28.5% CAGR from 2024-2032)—an extraordinary projection reflecting AI integration, digital banking adoption, and wealth management technology.

Sub-Sector Strength:

- Digital Assets & Cryptocurrency: Hong Kong hosts the highest number of blockchain/digital asset companies globally. The April 2024 launch of spot Bitcoin and Ethereum ETFs, combined with HKEX’s Virtual Asset Index Series (November 2024), positioned Hong Kong as Asia’s leading crypto trading hub.

- WealthTech: With $2.3 trillion in asset management, wealth-tech platforms for portfolio management, robo-advisory, and estate planning have proliferated.

- Payment and Remittance: Digital payment infrastructure (mobile wallets, real-time payment platforms, cross-border remittance) connects Hong Kong to Southeast Asian diaspora communities.

- Green Fintech: Emerging sector addressing ESG finance, sustainable bonds, and green loans, aligning with government climate commitments.

- Insurtech: Digital insurance platforms for micro-insurance, health insurance, and parametric insurance targeting underserved populations. Hong Kong financial services sector 2026.

“Fintech 2030” Strategic Pillars:

The HKMA’s November 2025 announcement outlined four pillars, acronymed “DART”:

- Data (D): Robust infrastructure for secure, efficient, scalable data sharing and cross-border payment connectivity—addressing credit access, trade finance, remittances, and personalized financial services.

- Artificial Intelligence (A²): Comprehensive strategy for responsible AI adoption, development of shared AI infrastructure, and sector-specific models for authorized institutions.

- Resilience (R): Strengthening financial system stability, cybersecurity, and regulatory frameworks.

- Tokenisation (T): Real-world asset tokenization, blockchain-based settlement infrastructure, and Project Ensemble (enabling real-value transactions on blockchain infrastructure).

Regulatory Sandbox and Innovation: The HKMA’s Fintech Supervisory Sandbox permitted 352 fintech initiatives by September 2024, with banks collaborating on 244 trial cases. This creates safe-harbor environment for experimentation while maintaining prudential oversight.

Fintech 2025 Achievements (2021-2025):

- All-banks-go-fintech mandate drove digital transformation across retail and corporate banking

- CBDCs research (mBridge project) positioned Hong Kong as forefront of CBDC development

- Data infrastructure enhancement enabling real-time, secure information sharing

- FinTech-savvy workforce expansion through academic partnerships and training programs

Digital Assets and Cryptocurrency: Asia’s Premier Hub

Hong Kong’s positioning as Asia’s leading crypto and digital asset center reflects deliberate government strategy, regulatory clarity, and infrastructure development.

Regulatory Framework: The Securities and Futures Commission (SFC) announced swift licensing pathways for crypto platforms, distinguishing Hong Kong from restrictive jurisdictions (US, EU, Singapore). By 2025, multiple digital asset trading platforms (including global leaders) obtained SFC licenses, enabling regulated crypto trading at institutional scale.

Exchange-Traded Products: April 2024 spot Bitcoin and Ethereum ETF launches, managed by global firms (Valiant, Bosera, China Asset Management), brought crypto exposure to retail and institutional investors through traditional securities infrastructure. These ETFs, domiciled in Hong Kong and listed on HKEX, combine regulatory clarity with global investor access.

Project Ensemble Tokenization Initiative: The HKMA’s Project Ensemble pilot enables real-value transactions on blockchain infrastructure—tokenizing government bonds, Exchange Fund papers, and corporate securities. This represents breakthrough in combining blockchain efficiency with institutional-grade risk management.

Fintech Connect Platform: October 2024 launch of Fintech Connect (partnership between HKMA and Qianhai Authority) created cross-sectoral sourcing platform connecting financial institutions with fintech solution providers across Hong Kong and Greater Bay Area.

hong kong E-Commerce and Digital Commerce: High-Value but Modest Growth

Hong Kong’s e-commerce market, while smaller than mainland China or Southeast Asia, demonstrates high growth potential driven by affluent consumers, mobile penetration, and cross-border opportunities.

Market Size and Growth: The e-commerce market reached $23.5 billion in 2024 and is projected to reach $30.5 billion by 2027 (7% CAGR). Retail e-commerce (excluding travel, digital goods, etc.) represented $9 billion of the 2024 total.

Cross-Border E-Commerce Dominance: A remarkable 56% of Hong Kong’s e-commerce transactions are cross-border—reflecting Hong Kong’s position as gateway to mainland China, ASEAN, and global markets. This cross-border orientation distinguishes Hong Kong from domestic-focused e-commerce markets, creating opportunity for Hong Kong merchants to serve regional consumers.

Market Characteristics:

- Mobile dominance: 62% of purchases via mobile devices, 75% shop via social commerce

- High average transaction value: ARPU reached $1,381 in 2024, reflecting affluent consumer base

- Payment modernization: 76% digital wallets and card payments; 98% banked population enables digital payment adoption

- Key categories: Electronics, fashion, food, household essentials, beauty

- Platforms: Alibaba, JD.com, Amazon, local player HKTVmall, and Shopify (44.31% market share for independent stores)

Government Support: 2025 initiatives including “Ecommerce Express” program (HKTDC in partnership with major platforms) and enhanced mentorship schemes for SMEs aim to boost e-commerce exports and Greater Bay Area integration.

hong kong AI Integration and Technology Adoption

Hong Kong’s financial sector demonstrates exceptional AI adoption—38% of finance executives have deployed generative AI, exceeding global average of 26%. This early adoption reflects:

- Capital availability for technology investment

- Regulatory encouragement through HKMA’s Fintech Roadmap and AI² strategy (focusing on responsible AI adoption)

- Competitive pressure from blockchain and fintech disruption

- Institutional sophistication of Hong Kong’s financial institutions

AI Applications: Robo-advisory for wealth management, fraud detection and transaction monitoring, customer service chatbots, credit risk assessment, and algorithmic trading dominate AI deployment in Hong Kong’s financial sector. Hong Kong financial services sector 2026.

Shared AI Infrastructure: The government’s commitment to developing shared, sector-specific AI models aims to lower barriers to entry for smaller fintech firms and democratize AI access across the financial ecosystem.

Competitive Positioning and Strategic Advantages

Structural Strengths:

- Global financial hub status: 70+ top-100 banks, 29 multinational bank HQs, leading capital markets

- Legal framework: Common law system, rule of law, contract enforcement aligned with Western standards

- Regulatory clarity: HKMA, SFC, and Insurance Authority provide sophisticated regulatory framework

- Ease of business: Minimal bureaucracy, English language, efficient licensing for financial entities

- Strategic geography: Gateway to China, positioning within Greater Bay Area, regional headquarters hub

- Talent and expertise: Deep pools of financial professionals, technologists, and entrepreneurs

- Fintech ecosystem maturity: 1,100+ fintech companies, established VC networks, regulatory sandboxes

- Digital assets leadership: First-mover advantage in crypto ETFs, regulatory clarity on digital assets

Structural Vulnerabilities:

- Geopolitical uncertainty: Political tensions with China, impact of “One Country, Two Systems” erosion on investor confidence

- Capital outflows: Wealthy individuals and companies increasingly relocating HQs to Singapore, Tokyo, US (citing uncertainty)

- Mainland competition: Shanghai and Shenzhen stock exchanges, payment systems (Alipay, WeChat Pay) challenging Hong Kong’s financial dominance

- Tariff exposure: Rush-shipment demand may be temporary; normalization of trade patterns could deflate export growth

- Population constraints: Smaller population limits domestic market; dependency on external demand and cross-border flows

- Energy and resources: Limited natural resources, reliance on mainland for utilities and food

- Regulatory pressure: Potential restrictions on crypto, fintech regulations becoming more stringent globally

Future Outlook: Opportunities and Challenges

Growth Opportunities (2025-2030):

- AI-powered financial services: AI² strategy positioning Hong Kong as leader in responsible AI adoption in finance

- Tokenized asset ecosystem: Project Ensemble enabling real-world asset trading on blockchain

- Greater Bay Area integration: Cooperation with Shenzhen, Guangzhou, Zhuhai on payments, trade finance, and innovation

- Digital asset trading: Continued expansion as regulatory clarity and institutional adoption accelerate

- Wealth management growth: Asian wealth creation (especially from China/Southeast Asia) flowing to Hong Kong managers

- Green finance: Sustainable bonds, ESG finance, and climate-focused investment products

Strategic Risks (2025-2030):

- Geopolitical volatility: Further erosion of autonomous institutions could drive capital flight and talent departure

- Regulatory crackdown: Global authorities tightening fintech, crypto regulations could constrain Hong Kong’s first-mover advantages

- Shanghai/Shenzhen competition: Mainland financial centers gaining capabilities and market share

- US tariff impacts: Extended 20% tariffs reducing rush-shipment volumes and normalizing 2026 growth downward

- Blockchain sustainability: Crypto market cycles creating volatility and regulatory backlash

- Economic slowdown: Global recession reducing asset management volumes and trading activity

Conclusion: A Sophisticated Hub Navigating Uncertainty

Hong Kong’s economy, built on financial services dominance, global trade centrality, and increasingly fintech innovation, has demonstrated remarkable resilience through 2025. The 3.8% Q3 GDP growth, surge in exports from rush shipments, and record 1,100+ fintech companies reflect genuine economic strength and positioning as Asia’s leading financial and innovation hub.

However, this strength rests on precarious foundations: geopolitical uncertainty regarding Hong Kong’s autonomous institutions, mainland competition eroding financial leadership, and tariff-driven cyclical export dynamics. The 2026 projected slowdown to 2.5% growth signals recognition of these constraints—not temporary cyclical weakness but structural moderation from tariff implementation and normalization of rush-shipment demand. Hong Kong financial services sector 2026.

Hong Kong’s “Fintech 2030” strategy, with $1 billion AI research institute investment and comprehensive fintech roadmap, represents strategic positioning toward technology-driven growth. Success hinges on three factors: (1) sustained regulatory clarity and government support for fintech/digital assets; (2) maintenance of geopolitical stability and investor confidence in autonomous institutions; and (3) successful integration with Greater Bay Area while differentiating from mainland financial centers.

If Hong Kong executes effectively, 2025-2030 could witness the emergence of a transformed financial center—less dominant in absolute banking volume (shifted to mainland) but globally preeminent in fintech innovation, digital assets, and technology-enabled financial services. Conversely, continued geopolitical deterioration and capital flight would rapidly unwind these advantages.

Hong Kong GDP Growth: Export Boom and Trade Hub Recovery (2024-2026)

official Hong Kong government websites

| GovHK – Hong Kong SAR Government | GovHK – Hong Kong SAR Government |

| GovHK – Residents portal | GovHK – Residents portal |

| GovHK – Government Websites | GovHK – Government Websites |

| Hong Kong SAR Beijing | Hong Kong SAR Beijing |

Read more country case studies done before this.