India’s Technology

India IT and fintech growth 2026.

India stands at the inflection point of a profound economic and technological transformation. Over the past five years, the country has evolved from a primarily services-driven economy into a diversified, technology-enabled ecosystem spanning artificial intelligence, fintech, e-commerce, renewable energy, electric vehicles, and emerging sectors like AgriTech and cybersecurity. This comprehensive case study examines the structural drivers, sectoral dynamics, competitive positioning, and forward trajectory of India’s technology econ

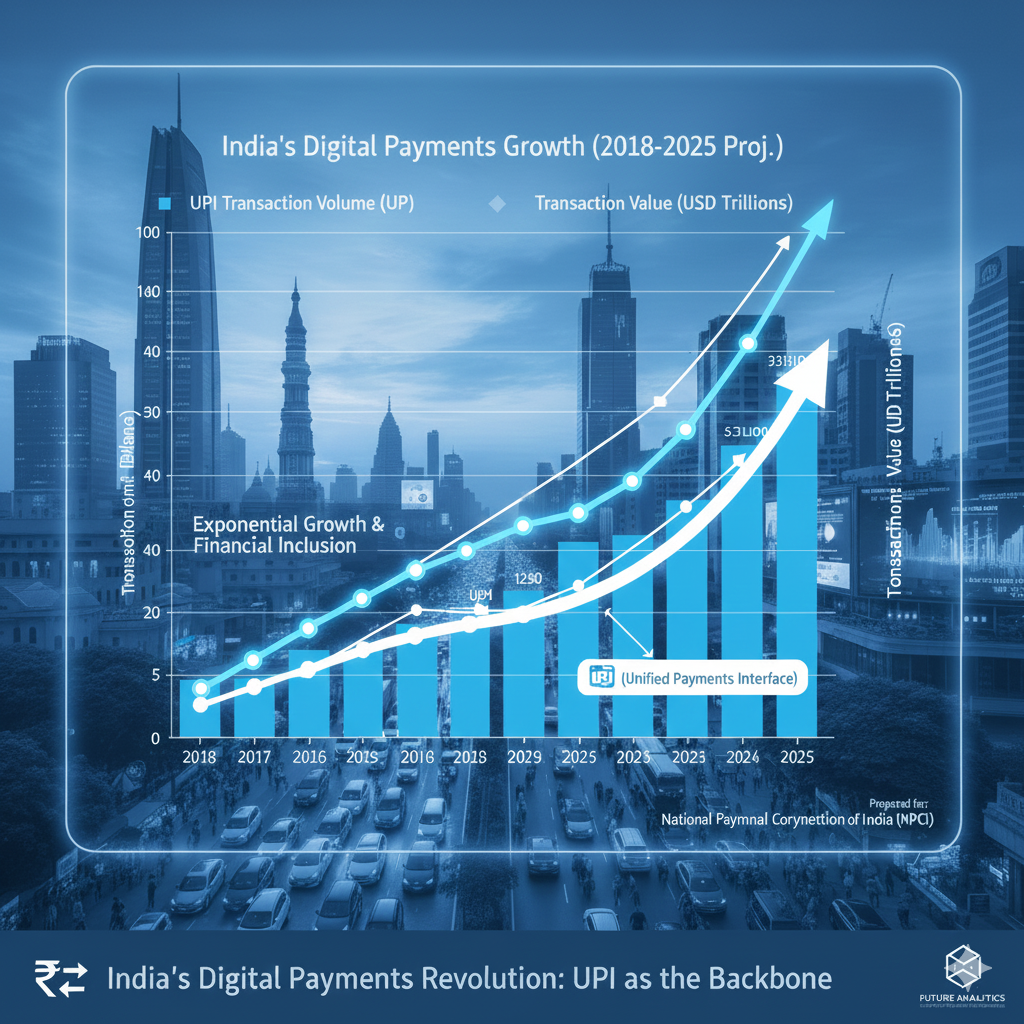

India Digital Payments Revolution: UPI as the Backbone

India’s digital payments ecosystem represents the most mature and globally influential component of its technology infrastructure. The Unified Payments Interface (UPI), launched in 2016, has become the dominant force in Indian financial transactions, commanding 85% of all digital payment volumes while representing only 9% of transaction value—a pattern indicating its use in high-frequency, small-value transactions.

The growth trajectory is extraordinary. UPI processed 21.63 billion transactions worth ₹27.97 lakh crore (approximately $33.6 billion USD) in December 2025, representing 29% volume growth and 20% value growth year-over-year. Monthly average daily transactions reached 698 million by December 2025, the highest ever recorded. The RBI Digital Payments Index surged to 493.22 in March 2025 (a fourfold increase since the base of 100 in March 2018), reflecting rapid expansion in payment infrastructure, merchant acceptance networks, and QR code-based payments.

The broader digital payment ecosystem is expected to expand dramatically: PWC forecasts digital transaction volumes will grow from 206 billion in FY25 to 617 billion by FY30, while transaction value will rise from ₹299 trillion to ₹907 trillion—a threefold increase in value over five years. This growth is driven by government initiatives (Digital India, PIDF extending financing for 14+ lakh POS devices and 4 crore QR codes), smartphone penetration (80.65 per 100 people in 2022, rising to 600+ million active mobile internet users), and fintech innovation.

Offshore remittances to India from diaspora communities total $100+ billion annually, creating a global use case for real-time payments. Singapore’s UPI-to-PayNow integration demonstrated the system’s international viability, enabling frictionless cross-border payments that rival traditional SWIFT transfers in speed while offering significantly lower fees.

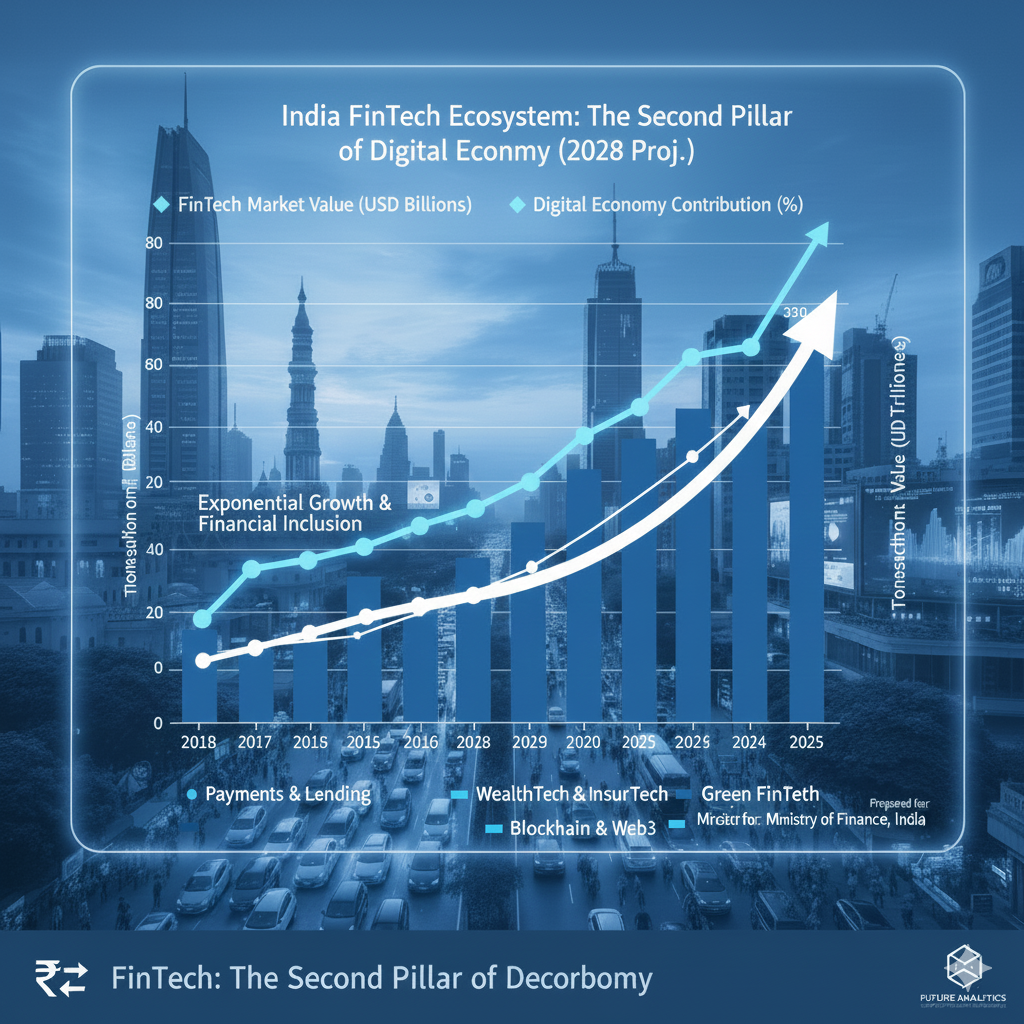

india FinTech: The Second Pillar of Digital Economy

India’s fintech ecosystem has matured substantially, with 29+ regulated fintech entities and a broader ecosystem of 520+ fintech companies in 2024. The sector encompasses digital banking, lending platforms, insurance technology, wealth management, and embedded finance—creating a comprehensive financial services alternative to traditional banks.

India’s fintech landscape continues to evolve, driven by technological advancements and increasing consumer demand for accessible financial services. With the integration of digital solutions, the sector has fostered financial inclusion for previously underserved populations, significantly enhancing economic participation. Additionally, the regulatory framework has adapted to support innovation while ensuring consumer protection, further solidifying India’s position as a global leader in fintech development. As the sector expands, it is poised to play a pivotal role in shaping the future of the country’s digital economy.

Fintech funding, while facing challenges (down 17% year-over-year in 2025 due to RBI’s tighter regulations on digital lending and KYC norms), still commanded 32% of all startup funding in 2024. Major fintech unicorns including Razorpay (payment processing), CRED (credit card rewards), and BharatPe (merchant payments) have achieved substantial scale and profitability milestones. However, a 75% failure rate among venture-backed fintech startups in 2025 indicates sector correction toward sustainable business models rather than growth-at-any-cost paradigms.

The critical distinction is between fintech for urban consumers and fintech for financial inclusion. While urban fintech faces consolidation, solutions targeting underbanked and unbanked populations in tier-2/3 cities and rural areas continue attracting capital. This bifurcation reflects India’s dual economy: high-income, digitally native urban populations coexisting with vast underserved rural markets.

india FinTech: The Second Pillar of Digital Economy

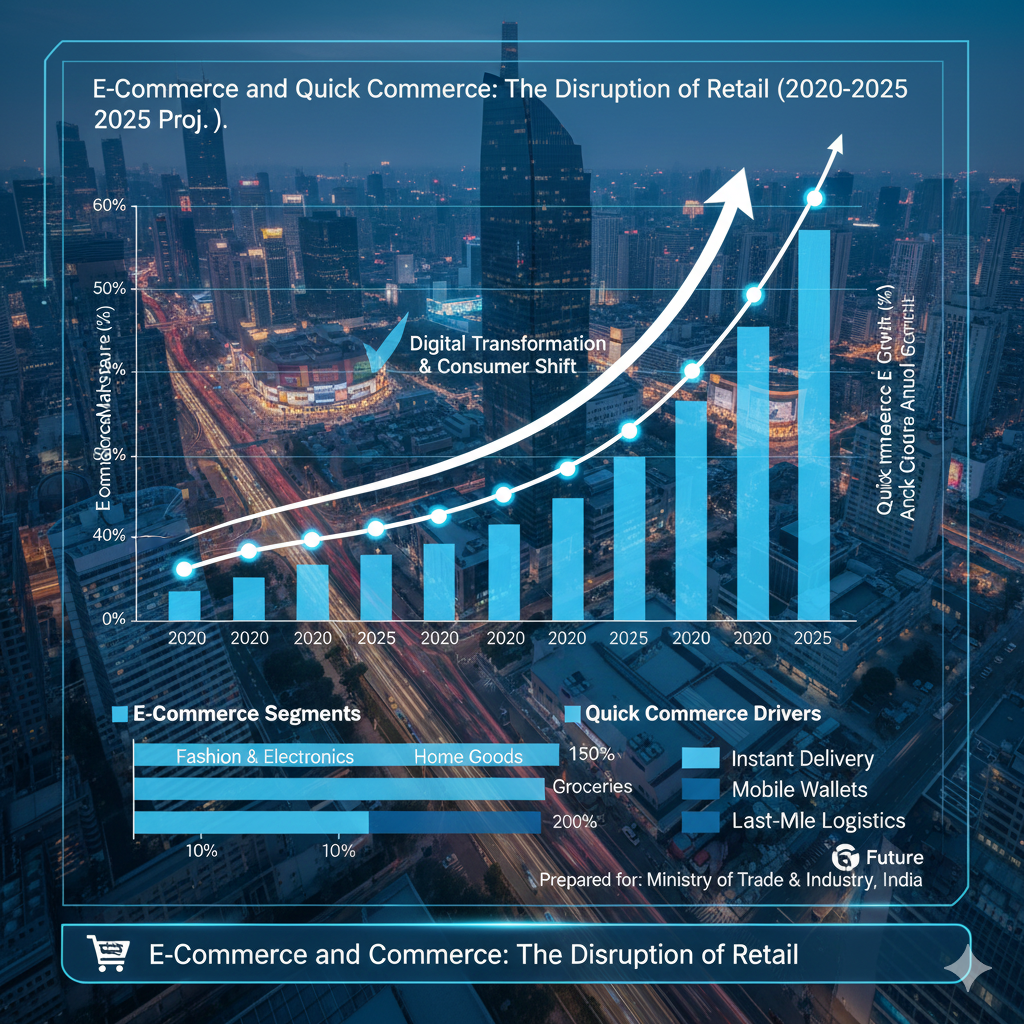

India’s e-commerce market, while not fully displacing traditional retail, has achieved transformative scale. The sector accounts for 10% of all e-retail spending (estimated $110-120 billion annually), with extraordinary growth in quick-commerce—delivery of groceries, snacks, and essentials within 10-30 minutes.

E-Commerce and Quick Commerce

Quick-commerce represents the most dynamic retail innovation. The sector grew from negligible volumes in 2022 to $6-7 billion GMV in 2024, capturing two-thirds of all e-grocery orders. Market projections suggest 40% annual CAGR through 2030, driven by category expansion beyond groceries (beauty, electronics, pharmacy) and deeper penetration into tier-2/3 cities.

Blinkit (Zomato subsidiary) achieved >50% market share by September 2025, up from ~46% in late 2024, with Zepto as the fast-growing second player and Swiggy Instamart, Flipkart Minutes, and BB Now competing aggressively. Blinkit achieved adjusted EBITDA profitability in March 2024 and has begun scaling sustainably, validating the quick-commerce business model.

The infrastructure underpinning quick-commerce growth—dark stores (densely distributed micro-warehouses), AI-driven inventory management, last-mile logistics optimization, and mobile-first consumer acquisition—represents a technology moat difficult for traditional retailers to replicate. The largest quick-commerce operators manage predictive analytics for “fast-moving SKUs” (stock keeping units like rice, paracetamol, USB cables) with 90-second pick paths, leveraging real-time rider synchronization and customer tracking through proprietary applications.

However, concerns about long-term viability persist. Industry experts warn that quick-commerce’s growth may be ephemeral, limited by unit economics outside major metropolitan areas, fierce competition compressing margins, and eventual consolidation into a smaller player set. The 40% CAGR projection assumes successful expansion beyond metros—a challenge not yet definitively solved.

india Artificial Intelligence: From Research to Application

India’s AI startup ecosystem has emerged as a global center of gravity. Over 150 native AI startups collectively raised $1.5+ billion since 2020. The sector spans infrastructure (TrueFoundry, others), enterprise applications (Observe.AI in customer service, $214M+ raised), healthcare diagnostics (Niramai in breast cancer detection, SigTuple in pathology automation), and emerging language models (SarvamAI developing Indic LLMs, selected by the government to build India’s sovereign LLM under the IndiaAI Mission in April 2025).

AI funding surged in 2024-2025. Computer services exports (AI-driven) grew 30% since ChatGPT’s November 2022 introduction, compared to 10% growth in overall services exports. This 3x differential underscores AI’s outsized economic impact. Global VC funding in AI exceeded $19 billion in Q2 2025, with India capturing a growing share through both domestic startups and multinational R&D centers expanding Indian operations.

Artificial Intelligence: From Research to Application

The IndiaAI Mission, launched by the central government, represents a strategic commitment to building indigenous AI capabilities. Ten cutting-edge Indian startups received prestigious support for advanced AI development in October 2025, signaling government prioritization beyond traditional IT outsourcing toward AI research and development.

India’s AI advantage rests on three foundations: (1) software engineering talent depth (5M+ trained engineers capable of AI implementation); (2) vast datasets for training models (India’s digital economy generates petabytes daily); and (3) unique use-cases addressing underserved populations (Indic language processing, healthcare diagnostics for resource-constrained settings, agricultural optimization for smallholder farms). The sector’s challenge is transitioning from application and implementation services toward proprietary model development—an area where India has begun making genuine progress.

india Artificial Intelligence: From Research to Application

India is undergoing an unprecedented renewable energy expansion aligned with its 2030 target of 500 GW non-fossil fuel capacity and 2070 net-zero goal.

As of January 2025, India’s total non-fossil capacity had reached 217.62 GW (46.3% of total installed capacity), with record-breaking 24.5 GW solar and 3.4 GW wind additions in 2024—representing 2.8x and 1.21x increases respectively from 2023. FY 2024-25 saw 29.52 GW of new renewable capacity added, with solar contributing 23.83 GW.

India has officially surpassed Japan as the world’s third-largest solar energy producer. Installed solar capacity reached 105.65 GW by March 2025 (including 81 GW utility-scale, 17 GW rooftop, and 4.74 GW off-grid). Wind capacity grew to 50 GW (up from 47.3 GW in 2024, with projections to 100 GW by 2030). The PM Surya Ghar: Muft Bijli Yojana residential rooftop program achieved 7 lakh installations within ten months of 2024 launch, demonstrating rapid household adoption. Off-grid solar increased 182%, adding 1.48 GW for rural electrification and energy access.

Electric Vehicles represent the complementary pillar: India’s EV market, at $54.41 billion in 2025, is projected to double to $110.7 billion by 2029 (19.44% CAGR). EV sales surged from ~4,700 units annually (pre-2020) to nearly 100,000 in 2024, with government targets of 17 million annual units by 2030 and 30% EV penetration across all vehicles. Two-wheelers dominate at 50%+ of sales, followed by three-wheelers (36%), and passenger cars (11% of market but growing 20% YoY despite global EV slump).

Public EV charging infrastructure expanded nearly fivefold from 5,151 stations (2022) to 26,367 by early FY25 (72% CAGR). Battery electric vehicle (BEV) production is expected to surge 140.2% in 2025, reflecting manufacturing focus on pure electric vehicles over hybrids.

The EV transition is supply-chain driven: India aims to develop indigenous battery manufacturing capabilities, reduce import dependence, and capture downstream value. Success requires solving three critical constraints: (1) battery manufacturing scale-up (India currently sources 70-80% of battery cells from China); (2) charging infrastructure density in smaller cities and highways; and (3) affordable models (most current EVs target premium segments; sub-$10,000 EVs remain scarce despite government goals).

E-Commerce’s Transformation of Consumer Behavior

India’s e-commerce market demonstrates the complex interplay of technology adoption and traditional commerce persistence. The sector comprises an estimated $110-120 billion in GMV annually, with growth concentrated in quick-commerce, fashion, and electronics—while groceries remain 65-70% cash-based nationally (though 70%+ digital in metros).

The 2025 e-retail landscape reflects a critical shift: merchants are moving from price-based competition to value-added services (free returns, easy EMI options, faster delivery) and category diversification. Tier-2/3 city growth outpaced metros for the first time, driven by smartphone proliferation, improved 4G/5G coverage, and normalized digital payment adoption among non-cosmopolitan populations.

Mobile commerce dominance is absolute: 99.7% of Indian internet users access services via smartphones, making app-based retail the de facto default distribution channel. This mobile-first architecture, while advantageous for acquisition and engagement, creates dependencies on app store algorithms and requires continuous investment in user experience optimization to combat churn.

india HealthTech and Telemedicine: Bridging Rural-Urban Healthcare Divides

HealthTech startups raised $7+ billion across 800+ deals since inception, with 8.4% of total startup funding in 2024. The sector encompasses telemedicine (Practo, 1mg, Pharmeasy), AI diagnostics (Niramai, SigTuple), and digital health management, addressing India’s vast healthcare infrastructure gaps.

HealthTech and Telemedicine: Bridging Rural-Urban Healthcare Divides

India’s healthcare system is characterized by extreme regional variation: urban centers have world-class tertiary care facilities alongside massive underserved rural populations with limited primary healthcare access. HealthTech solutions address this asymmetry by enabling remote diagnostics, prescription delivery, and health monitoring for geographically dispersed patients. The market has achieved meaningful scale: telemedicine consultations reached millions monthly by 2024, while digital prescription delivery demonstrated strong adoption in tier-1 cities.

However, HealthTech faces structural challenges: (1) reimbursement complexity (insurance coverage remains limited; most transactions are out-of-pocket); (2) regulatory uncertainty (telemedicine rules vary by state, creating compliance burden); (3) trust deficits (consumers remain skeptical of diagnoses without in-person examination in certain demographics); and (4) profitability pressures (customer acquisition costs remain high, margins compressed). The 80% failure rate among venture-backed HealthTech startups in 2025 reflects brutal correction toward sustainable business models.

EdTech: From Pandemic Boom to Sustainable Correction

EdTech exemplifies the boom-bust cycle afflicting several Indian startup sectors. The education technology market reached $29 billion (2024 valuation) with 10,000+ companies operating in India, supported by 30,000+ crores invested in the sector. Byju’s, Unacademy, and Vedantu became household names, raising hundreds of millions in venture capital.

However, 2024-2025 revealed structural weaknesses: when schools reopened post-pandemic, demand for learning apps collapsed. The 60% failure rate among EdTech startups reflects this correction. Surviving companies have pivoted toward B2B models (selling to schools and institutions), skills-based learning, and regional language content—moving away from consumer-direct mass-market strategies.

The sector’s challenge is addressing India’s chronic quality-of-life education gap: 260+ million students of school age, but only 300-400 million formal seats, creating demand for supplementary education. However, monetizing this demand proves difficult given low average incomes in tier-2/3 cities and parental skepticism toward education technology.

AgriTech: Innovation Meets Scale Challenges

India’s agricultural sector employs 250+ million people, generates $400+ billion in annual output, yet remains largely unmechanized and data-deprived. AgriTech startups—leveraging AI, IoT, and data analytics to optimize crop yields, reduce input costs, and improve supply chain efficiency—have attracted substantial capital.

Over 160 agritech startups collectively raised $2.4 billion since 2014, with $1.6 billion raised in 2024 alone. Growth-stage startups dominated, raising $1.59 billion across 60 deals, while early-stage ventures attracted $500M+ through 186 seed/angel deals. Delhi-NCR leads the funding landscape (40.6% of agritech funding), followed by Bengaluru (26.25%), Chennai, Pune, and Mumbai.

Despite historical growth, 2025 revealed significant headwinds. Agritech funding collapsed to $182 million in 2025 (from $390.52 million in 2024 and $498.28 million in 2023)—a 53% year-over-year decline signaling market correction. Challenges include: (1) technology adoption barriers among smallholder farmers with limited literacy and English proficiency; (2) seasonal cash flow constraints limiting ability to pay for digital services; (3) regulatory barriers (land titling, credit access); and (4) consolidation pressure reducing viable competitors.

However, sub-segments like dairy-tech maintained investor interest due to daily consumption patterns and clear business model viability. Government support through AgriSURE ($90 million fund launched 2024), Innovation and Agri-Entrepreneurship Development Programme (RKVY RAFTAAR, providing ₹5-25 lakh grants), and Agri Udaan continue supporting early-stage ventures, offsetting private market slowdown.

Logistics and Supply Chain Tech: Modernization at Scale

India’s logistics sector was valued at $310.2 billion in 2024 and is projected to reach $668.2 billion by 2033 (8.9% CAGR). The sector is undergoing rapid digitalization through IoT-enabled tracking, AI-driven route optimization, blockchain-based transparency, and automated warehousing.

Freight transport remains the core (63.07% of market), but courier, express, and parcel services are growing fastest at 10.72% CAGR. The e-commerce boom has catalyzed last-mile delivery innovation: platforms now achieve 95%+ on-time performance through AI-driven route orchestration, addressing urban congestion. Manufacturing logistics demand supports just-in-time inventory models and reverse-logistics capabilities. Road transport dominates at 70.22% of freight volumes but faces labor scarcity and fuel cost volatility—drivers for fleet electrification pilots and vehicle scrappage incentives.

Emerging opportunities include cold chain logistics (pharmaceuticals, perishables), 4PL (fourth-party logistics coordinating multiple carriers), and cross-border logistics (enhanced by India’s port expansion under Sagarmala and inland waterway modernization).

Cybersecurity: From Afterthought to Strategic Priority

India’s cybersecurity sector has emerged as a high-growth, strategically important domain. Over 400 startups and 650,000 professionals power a $20 billion industry (2025), with 18.33% projected CAGR through 2030. India ranked among the world’s top cybersecurity product developers, with Indian cybersecurity product revenue reaching $4.46 billion in 2025 (34% CAGR since 2020).

Solutions dominate market revenue (65.2% of market share), with network security, cloud-workload protection, and identity-access management as core offerings. Cloud-based security is growing fastest at 22.3% CAGR, reflecting infrastructure migration trends. Large enterprises hold 70.4% of market share but SMEs are expanding rapidly at 20.1% CAGR as tiered SaaS pricing models reduce adoption barriers.

Startups (PingSafe, Safe Security, Indusface, Quick Heal) address India-specific pain points—multilingual phishing, Aadhaar-linked fraud, regional threat landscapes—gaining traction through government support and channel partnerships. India reported 147 ransomware incidents in 2024, with CERT-In’s coordinated response demonstrating importance of indigenous cyber defense capabilities as geopolitical tensions intensify.

Government initiatives including the Cyber Mission, data localization requirements, and support for indigenous cybersecurity product development have created favorable conditions for startup growth and M&A (2025 cybersecurity M&A exceeded $9.2 billion across 120 deals globally).

Competitive Landscape and Global Positioning

India’s technology ecosystem has moved beyond cost arbitrage toward genuine innovation and IP creation. The country is increasingly positioned as a preferred destination for global companies seeking to locate AI research centers, innovation labs, and talent concentration.

Strengths:

- Talent depth across software engineering, data science, and product management

- Proven ability to scale operations and manage complex projects

- Cost advantage (40-60% labor savings) combined with English fluency

- Large domestic market enabling rapid experimentation and iteration

- Government policy consistency and increasing regulatory clarity

- Diverse venture ecosystem with strong exit track record

Weaknesses:

- Product innovation limited relative to Western competitors; India excels in implementation rather than originality

- Regulatory uncertainty in emerging sectors (fintech, crypto, AI governance)

- Infrastructure gaps (power, water, broadband in non-metro areas) constraining manufacturing scale

- Skill-job mismatch persisting despite demographic dividend

- Brain drain of top talent to Western technology companies

Opportunities:

- AI-driven services commanding premium valuations and attracting global capital

- Green technology leadership (renewable energy, EVs) aligning with global decarbonization

- Fintech/payments dominance enabling financial inclusion at scale

- Emerging market-focused solutions (languages, affordability, distribution) creating defensible niches

- Government “AtmaNirbhar Bharat” and “IndiaAI Mission” creating tailwinds for indigenous technology

Threats:

- Global economic slowdown reducing venture capital flows to emerging markets

- Regulatory backlash against data localization and AI governance creating compliance burden

- Consolidation of Indian startups by Western and Chinese acquirers, reducing indigenous innovation

- China’s lower-cost competition in hardware manufacturing and emerging sectors

- Geopolitical tensions (US-China trade war) potentially restricting India’s technology exports

Conclusion: At the Threshold of Transformation

India’s technology economy stands at a pivotal juncture. The country has successfully demonstrated capability in digital infrastructure (UPI leadership), services innovation (IT outsourcing), and emerging sector development (quick-commerce, renewable energy, AI). The next decade will test whether India can transition from implementation and services toward genuine innovation leadership and IP creation.

The macro-level indicators are encouraging: 8.2% GDP growth (highest in six quarters, FY26), digital payments reaching 493.22 index points (fourfold increase from 2018), and 150+ AI startups raising $1.5B+ demonstrating ecosystem maturation. However, structural challenges—persistent youth unemployment, education-job mismatch, geographic concentration of opportunity in metros, and regulatory uncertainty in emerging sectors—constrain broader prosperity realization.

Success hinges on four critical transitions: (1) translating technological sophistication into sustainable profitability and unit economics; (2) expanding opportunity beyond metros to tier-2/3 cities while maintaining economic viability; (3) developing indigenous IP rather than remaining primarily implementation-focused; and (4) managing geopolitical headwinds from US-China tensions while maintaining openness to global capital and talent.