Tehran city

Iran technology and digital transformation 2026.

Executive Summary

Iran represents a paradox of simultaneous economic stagnation and digital innovation. Despite facing near-zero GDP growth (0.6% projected for 2025) and soaring inflation (42.4%), the country is building one of the Middle East’s most dynamic startup ecosystems, driven by a young population, high digital penetration, and government-backed innovation initiatives. With 3,728 active startups, an 80-million-person domestic market, and rapidly expanding sectors in fintech ($716.66M in 2024), e-commerce ($3.03B), healthtech, agritech, and renewable energy, Iran presents a high-risk, high-reward investment thesis for forward-looking stakeholders willing to navigate geopolitical and regulatory complexity.

This case study examines the structural factors enabling innovation in Iran’s constrained environment, the role of domestic venture capital, sector-specific opportunities, and critical success factors for scaling businesses in a sanctioned, cash-strapped economy.

Part 1: Macroeconomic Context—The Paradox of Constraint and Growth

iran Economic Performance and Currency Crisis

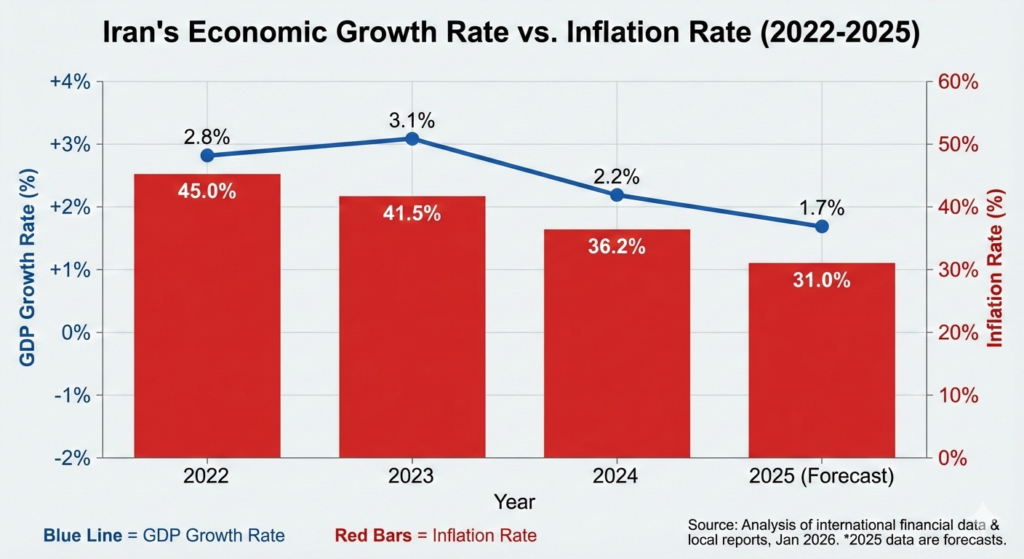

Iran’s macroeconomic environment in 2025 presents a stark disconnect between nominal growth and real economic deterioration. The International Monetary Fund (IMF) projects just 0.6% real GDP growth for 2025, a precipitous decline from 3.7% in 2024 and 5.3% in 2023. Simultaneously, official inflation has reached 42.4% annually, eroding purchasing power and pushing large swaths of the middle class into effective poverty.

Iran’s Economic Growth Rate vs. Inflation Rate (2022-2025)

The Iranian rial has experienced catastrophic depreciation, losing approximately 37% of its value against the US dollar in 2024 alone, with the black market rate reaching 1,126,000 rials per dollar by September 2025—a collapse that reflects deep-seated loss of confidence in monetary policy and currency management. This devaluation creates a dual crisis: it raises the cost of imported inputs for manufacturers and technology companies while simultaneously making Iran’s labor and local services exceptionally cheap by regional and global standards.

The nominal GDP is expected to fall below $400 billion USD in 2025-2026, down from historical highs around $500 billion, a reflection of combined effects of sanctions, oil revenue constraints, and structural misallocation. Unemployment stands at 9.2% officially, though youth unemployment (ages 15-24) persists at approximately 26%, with disproportionate impact on university graduates—a critical dynamic explored below.

Sanctions-Induced Structural Adaptation

The cascade of international sanctions since 2018 has reshaped Iran’s economic strategy fundamentally. Rather than forcing economic collapse (as initially predicted), sanctions have paradoxically accelerated the shift toward domestic innovation and self-reliance, particularly in technology sectors. This represents a form of “defensive innovation”—the necessity to create local alternatives when foreign sources dry up.

In manufacturing, sanctions have destroyed traditional export-oriented industries while simultaneously spurring domestic production of previously imported goods. Industrial production growth, which averaged 13% annually between 2002 and 2012, has since dropped to below 1% annually as technology gaps widen, but the sector has developed resilience through supplier diversification and new regional markets. This reorientation created immediate demand for technology solutions: e-commerce platforms, logistics software, payment processing, and AI-driven procurement tools emerged not as aspirational innovations but as direct substitutes for sanctioned imports.

Part 2: The Digital Demographic Advantage

Youth Bulge and Educational Output

Iran’s demographic structure represents perhaps its greatest long-term economic asset. Approximately 57% of the 80-million-strong population is under age 30, and the country produces 335,000 STEM graduates annually—the fifth-highest absolute output globally. This enrollment is heavily skewed toward engineering (approximately 50% of all university graduates), with 77% of all Iranian tertiary students pursuing STEM disciplines, a concentration far exceeding that of China (18.6% engineering among international students) or India (36% among international students). Iran technology and digital transformation 2026.

The tertiary gross enrollment rate has reached 71.9%—higher than Italy, Japan, or the United Kingdom, and more than double the global average. Yet this educational massification has created a structural labor market mismatch: while supply of graduates has soared, job creation has not kept pace. Official data indicate that more than 40% of the unemployed hold university degrees, and approximately 25-26% of youth aged 15-29 are classified as NEET (Not in Education, Employment, or Training), according to World Bank/ILO standardized estimates.

This paradox—excess education with constrained employment—has directly catalyzed the startup ecosystem. Unable to secure traditional employment, young graduates have founded ventures targeting their peers’ unmet needs: digital payment solutions, e-health platforms, agricultural productivity tools, and AI-driven business services. The surplus of low-cost, high-skilled technical talent has thus become the ecosystem’s engine.

Internet Penetration and Digital Adoption

Digital connectivity has penetrated deeper and faster in Iran than typically observed in comparable developing economies. Internet penetration stood at 79.6% in January 2025, representing 73.2 million users. Critically, mobile internet dominates: 93.1% of mobile connections now operate on 3G/4G/5G networks, and median mobile download speeds reached 38.88 Mbps in early 2025, representing a 22.2% year-on-year increase.

This mobile-first infrastructure has been transformative for commerce and fintech adoption. E-commerce transactions are predominantly conducted via mobile devices (approximately 70% of digital transactions), and over 90% of online payments flow through locally-operated payment gateways such as ZarinPal—a critical dependency that has isolated Iran’s digital economy from Western financial rails but simultaneously created space for indigenous fintech innovation.

The combination of young demographics, high digital literacy, and mobile-native behavior patterns has created a market environment where frictionless digital commerce encounters minimal legacy infrastructure resistance (unlike developed economies where incumbent retail and banking infrastructure slow innovation adoption).

Part 3: The Startup Ecosystem—Scale, Structure, and Resilience

Quantified Ecosystem Size and Funding Dynamics

As of 2025, Iran’s startup ecosystem comprises approximately 3,728 active startups that have collectively raised over $676 million in funding. While this pales compared to global tech hubs, it represents a mature, self-reinforcing system: the average funding per startup ($181,000) reflects seed-stage capital dominance, yet the ecosystem supports 162 accelerators (90% privately operated) and 45+ science and technology parks with over 600 innovation centers.

Iran’s domestic venture capital market is projected to reach $28.13 million in 2025, a modest figure that obscures critical institutional developments: the establishment of dedicated VC firms (Sarava Pars, Hamrah-Aval, Shenasa, Aftabnet) has created a professional capital allocation function previously absent. These firms have deployed capital into sectoral themes (fintech, healthtech, logistics, SaaS) with demonstrable portfolio discipline, despite the absence of liquid exit markets.

Government-backed funding mechanisms operate through multiple channels:

- Iran National Innovation Fund (INIF): Provides low-interest loans and grants specifically targeting fintech, blockchain, and AI startups

- Innovation & Prosperity Fund: Supports knowledge-based companies with R&D grants and loans, contingent on certification by the Vice Presidency for Science and Technology

- Iran National Development Fund (NDFI): Offers government-backed loans up to $500,000 (in local currency) with long-term repayment structures

These programs have effectively substituted for sanctioned foreign investment, creating a closed-loop funding ecosystem where domestic capital, angel networks, and government grants provide the entire funding stack for early-stage ventures.

The Pardis Technology Park Ecosystem: Iran’s Innovation Anchor

The Pardis Technology Park, established in 2005 and headquartered east of Tehran, functions as Iran’s primary innovation district. It hosts over 450 registered knowledge-based companies in advanced technologies (ICT, biotechnology, nanotechnology, mechanical engineering, automation) and has become the administrative and social center of the country’s startup culture.

The flagship Azadi Innovation Factory, a converted 18,500-square-meter industrial facility opened in 2017, represents the ecosystem’s physical and institutional hub. The factory supports 150+ active startups, operates nine specialized accelerators, and employs over 3,500 entrepreneurs, engineers, and support staff. It offers mentorship from diaspora experts, access to investor networks, and co-working infrastructure—services that would normally require significant private capital but are subsidized or provided by government entities.

According to the head of Pardis Technology Park, the ecosystem has generated approximately $1 billion in foreign currency savings through import substitution and localized production. The park’s integrated model—combining university research partnerships, government support, and private capital—has reduced startup failure rates significantly by ensuring continuity of support beyond the acceleration phase, addressing a persistent weakness in many global innovation hubs.

Notable Startup Case Studies

Snapp: From Ride-Hailing to Regional Super-App

Snapp, founded in 2014 (initially as Taxi Yaab), exemplifies how Iranian startups have captured market value through local adaptation. Beginning as a simple ride-hailing application competing against international entrants like Uber, Snapp pivoted to a “super app” model incorporating food delivery, hotel booking, flight reservations, package delivery, and telemedicine—services that Uber and Lyft were not offering in Iran due to sanctions restrictions on cross-border payment systems. Iran technology and digital transformation 2026.

The company has achieved unicorn-equivalent valuation (estimated at $1.4-1.7 billion), with South African telecommunications company MTN acquiring a 43% stake. Snapp currently processes over 1.2 million orders monthly through a domestic payment ecosystem (partnered with Irancell) and SnappPay digital wallet, and employs approximately 10,000 drivers across Iranian cities. The venture’s success illustrates how constraints (unavailable international services, local payment infrastructure requirements, vast untapped market) created defensible competitive moats that prevented foreign competitors from entering effectively.

ZarinPal: Fintech as Economic Necessity

ZarinPal, founded in 2009, has become Iran’s largest payment gateway, processing over 3 million transactions monthly and serving more than 1 million merchants. The company emerged directly from Iran’s need for domestic payment processing after international payment processors (PayPal, Stripe) became inaccessible due to sanctions.

ZarinPal’s evolution illustrates fintech maturation in constrained environments: it has layered services to include installment-based payment solutions, cross-border cryptocurrency payment options, and marketplace infrastructure for small businesses. Its merchant dashboard, fraud-control systems, and API infrastructure have become foundational to the country’s e-commerce stack. The company has positioned itself as an indispensable element of digital commerce infrastructure, creating high switching costs and sustained revenue visibility despite macroeconomic volatility.

Dr. Next and Telemedicine Scaling

Dr. Next, a telemedicine platform, secured $3 million in funding—exceptional for Iran-based healthcare ventures—by solving a genuine infrastructure gap: rural areas of Iran lack adequate physician density, and transportation costs prohibit frequent specialist consultations. The platform aggregates licensed physicians, integrates IoT medical devices, and provides video consultations, generating revenue through per-consultation fees and corporate wellness contracts.

The venture illustrates how healthtech startups in Iran are succeeding by addressing structural healthcare deficiencies (rural access, specialist scarcity, cost) rather than competing on premium consumer experiences. This problem-driven approach has proven more sustainable than consumer-centric business models in economically constrained markets.

Part 4: Sectoral Deep-Dives—Opportunities and Dynamics

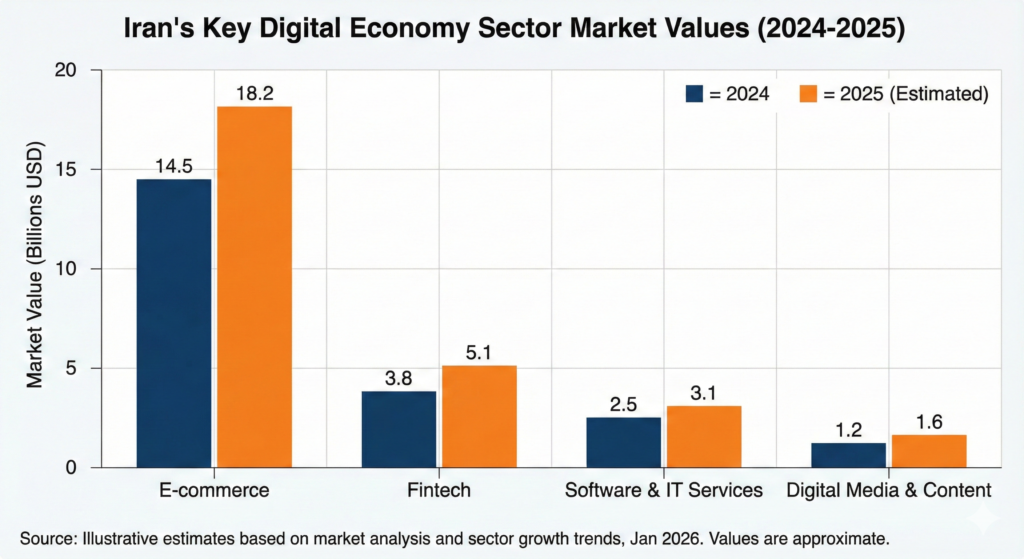

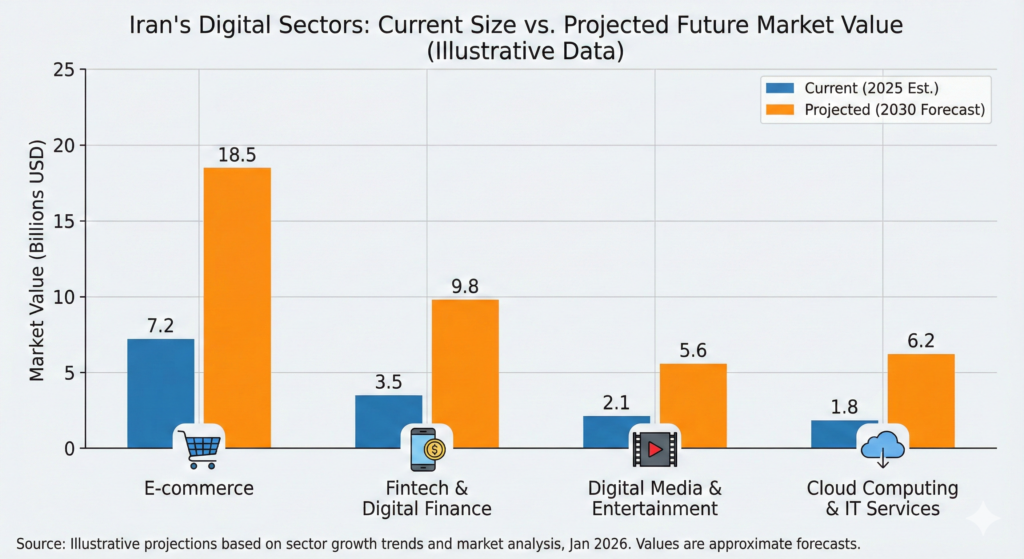

Digital Sector Market Values and Growth Trajectories

Iran’s Key Digital Economy Sector Market Values (2024-2025)

Iran’s Digital Sectors: Current Size vs. Projected Future Market Value

Iran’s digital economy encompasses multiple rapidly expanding sectors. The combined fintech, e-commerce, and healthcare technology markets represent approximately $19 billion in annual economic activity as of 2024-2025, with annualized growth rates ranging from 4% to 16% across sectors.

Fintech: Market Size, Competition, and Regulatory Sandbox

Iran’s fintech market reached $716.66 million in 2024 and is projected to expand to $2.69 billion by 2033, a 15.82% compound annual growth rate. This explosive growth trajectory reflects three drivers: (1) the shift from cash-based to digital payments (approximately 85% of financial transactions are now digital), (2) the rise of mobile-first banking alternatives to legacy banking infrastructure, and (3) demand for alternative payment and capital solutions from SMEs unable to access traditional credit due to banking sector dysfunction.

The fintech ecosystem has stratified into three layers: (1) Digital Payment Infrastructure such as ZarinPal and SnappPay, which process day-to-day transactions and have achieved scale through merchant commission models; (2) Alternative Finance and Lending platforms like Bahamta (peer-to-peer payments) and Tooseh (micro-lending under Islamic finance principles), serving unbanked populations; and (3) AI-Driven Analytics and Compliance startups building fraud detection, credit scoring alternatives, and automated regulatory reporting solutions.

The Central Bank of Iran (CBI) has approved a regulatory sandbox framework allowing fintech startups to test innovations under controlled oversight before market-wide deployment. This framework, while nascent, represents a critical institutional development: it lowers execution risk for startups and permits the CBI to gather data on emerging risks before they systemically impact the financial system.

Challenges remain severe: capital controls, multiple exchange rates, and frequent regulatory changes create operational uncertainty. Many fintech startups register offshore entities (in UAE or Turkey) to access international capital while operating domestically, a workaround that reduces compliance overhead but introduces tax and legal risks.

E-Commerce: Market Bifurcation and Logistics Innovation

Iran’s e-commerce market generated $3.03 billion in revenue in 2024 and is projected to reach $3.84 billion by 2029 (5.5% CAGR). More aggressively, the B2C e-commerce market is valued at $17.13 billion, with projections reaching $21.65 billion by 2029 (4.9% CAGR), suggesting significant definitional variance in market sizing across sources.

E-commerce in Iran has bifurcated into two distinct market segments: (1) Large-Scale Marketplaces such as Digikala (Iran’s Amazon equivalent), which processes over 1.2 million orders monthly, has expanded into groceries and books, and plans subscription-based premium memberships; and (2) Social Commerce and B2B Marketplaces targeting underserved segments—direct farmer-to-consumer sales, business-to-business wholesale markets, and social media-integrated shopping.

Electronics represent 24% of online retail revenue, but growth categories include fresh produce, home goods, and digital services—reflecting the consumer base’s shift toward essential and online-native categories amid inflation and purchasing power contraction.

Healthtech: Government-Backed Ambition and Market Readiness

Iran’s broader health and wellness market is valued at $15.22 billion and projected to reach $22.71 billion by 2033 (4.08% CAGR). Within this, healthtech (digital health, telemedicine, AI diagnostics, health information systems) is the fastest-growing subsegment, with digital health alone projected at 9.38% CAGR.

The government has articulated an explicit ambition: use AI integration to reduce healthcare costs by up to 40% while improving clinical outcomes. With total health expenditures projected to rise 30% by 2030, the capacity constraints are acute, making technology adoption not optional but strategically necessary.

Key healthtech companies and approaches include: (1) Telehealth Infrastructure such as Barakat E-Health Company (BEHCo) and Pezeshket, which serve rural populations and chronic disease management through integration with state health insurance systems; (2) AI-Driven Diagnostics from companies like CardioCan and AIMedic, developing machine-learning models for medical imaging analysis; and (3) Hospital Interconnectivity solutions like ASA Digital Health, building integrated digital health ecosystems connecting hospital systems.

Investment has been domestically funded due to sanctions, with the Iran National Innovation Fund (INIF) and angel networks from the medical and technology sectors providing capital. The regulatory environment has improved modestly, with clearer pathways for medical device classification and telehealth licensing, though ambiguity around data governance and patient privacy remains.

Agritech: Supply Chain Optimization and Resource Efficiency

Iran’s agricultural sector employs approximately 1.3 million workers and contributes significantly to non-oil exports (estimated at 8-10% of total exports). Agricultural startups number approximately 60, concentrated in three value chain segments: pre-farm (15 startups), on-farm (13 startups), and post-farm (32 startups).

Notable ventures include: (1) Massive Hydroponics, which develops home and commercial hydroponic systems integrated with IoT sensors and machine learning algorithms to optimize vegetable yields while reducing water consumption and pesticide usage; and (2) Jalizan, a technology platform offering comprehensive farm management integrated with online marketplaces for direct producer-to-buyer sales, eliminating intermediary markups that historically capture 30-40% of farm revenue.

The agritech ecosystem has received explicit government support through the Ministry of Agriculture’s “startups’ project,” aiming to create a dynamic agricultural entrepreneurship environment within a 10-year horizon. The challenge lies in farmer adoption: agricultural startups consistently report that low digital literacy, capital constraints for equipment upgrades, and cultural resistance to technology change slow uptake, even when ROI is demonstrable.

Renewable Energy: Government-Driven Capacity Targets and Private Sector Participation

Iran’s Renewable Energy Capacity Expansion Roadmap

Iran’s renewable energy capacity reached 2,550 MW as of October 2025, with an aggressive government roadmap targeting 5,000 MW by March 2026, 20 GW by 2027, 10 GW solar specifically by 2030, and 50 GW by 2031. These targets appear ambitious given execution constraints, but recent acceleration suggests momentum: Iran installed 600 MW of solar capacity in the fiscal year ending March 2025, a fourfold increase over historical annual averages.

The government has issued construction permits for nearly 100 GW of solar projects to catalyze private sector participation, though officials estimate only 15% conversion to operational capacity, reflecting typical implementation challenges (financing, technical capacity, land disputes). Private sector proposals total 38,000 MW of renewable capacity—far exceeding government targets, indicating strong commercial appetite for participation.

Key drivers and mechanisms include: (1) Electricity Demand Gap of approximately 23,000-24,000 MW that renewables can meaningfully reduce during peak demand periods; (2) Industrial Incentive Structure where facilities generating partial electricity via renewable sources are exempt from mandatory load reduction measures since 2023; (3) Residential Incentive Programs enabling households to sell excess rooftop solar generation at approximately 3,700 tomans/kWh; and (4) Cost Competitiveness with renewable equipment imports exempt from customs duties and national electricity tax, combined with optimal solar insolation (4+ kWh/m²/day) making Iran’s costs globally competitive.

The renewable energy transition is reshaping industrial electricity economics. Companies embracing efficiency and on-site renewable generation will face lower long-term electricity costs than those dependent on grid supply, creating a structural incentive for manufacturing decentralization and efficiency modernization.

Part 5: Structural Challenges and Risk Factors

Macroeconomic Instability and Currency Risk

The central vulnerability in scaling operations in Iran is currency devaluation and capital controls. The rial’s 37% depreciation in 2024 inflates input costs for imported materials, research equipment, and technology while simultaneously eroding consumer purchasing power. Startups with revenue in rials but costs in dollars face margin compression in every growth cycle.

Firms have adapted through three mechanisms: (1) pricing power—passing cost increases to customers, feasible for essential services but not for discretionary products; (2) offshore registration—holding revenue in USD through UAE, Turkey, or other intermediary jurisdictions, reducing remittance exposure but introducing tax and compliance complexity; (3) barter and alternative settlement—increasingly, startups invoice each other and suppliers in cryptocurrency or stablecoins to bypass currency controls, a fragile workaround that the Central Bank is actively attempting to restrict.

The Central Bank’s recent crackdown on rial-based stablecoins and cryptocurrency gateways, while motivated by legitimate concerns about capital flight, risks displacing transactions onto unregulated peer-to-peer venues, exacerbating systemic opacity and financial instability.

Capital Constraints and Limited Exit Pathways

Iran’s startup ecosystem has not produced a venture-scale exit in over a decade. The most recognized “unicorns” (Snapp at $1.4-1.7B, Digikala with comparable valuations) are largely domestic acquisitions or strategic investments by regional entities (MTN, Irancell). Without liquid public markets or demonstrable precedent for institutional-scale liquidity events, venture investors face extended holding periods and ambiguous exit scenarios.

This dynamic has several consequences: (1) VC firms must accumulate patient capital, creating competitive disadvantage relative to global VCs with limited partner pressures; (2) founder compensation structures lean toward employee equity rather than founder buyouts, concentrating wealth and potentially limiting serial entrepreneurship; (3) attracting institutional capital from global pension funds and endowments remains nearly impossible, constraining capital pool size.

Regulatory Ambiguity and Compliance Risk

While the Iranian government has articulated support for tech entrepreneurship through tax exemptions, innovation funds, and improved licensing procedures (now largely digitized), regulatory ambiguity remains pervasive. Key vulnerabilities include: (1) Shifting Sanctions Enforcement that changes unpredictably, creating sudden legal exposure for startups using cloud services or payment channels; (2) Data Sovereignty and Content Restrictions requiring local data hosting and content compliance that create complexity for consumer platforms; and (3) Financial Regulation dysfunction and periodic shifts in foreign exchange policy creating operational uncertainty.

Companies have responded by ensuring domestic-only operations, building custom infrastructure to avoid reliance on foreign providers, and maintaining redundant financial channels. These adaptations raise costs but reduce regulatory exposure.

Human Capital Development and Brain Drain

While Iran produces 335,000 STEM graduates annually, the mismatch between supply and productive employment opportunities drives sustained brain drain. Highly skilled engineers, researchers, and entrepreneurs leave for North America, Europe, and the Gulf—a pattern that has persisted for decades and continues despite recent economic downturns in traditional emigration destinations.

Startups therefore must compete for domestic talent against the global opportunity set, offering equity and opportunity-driven compensation to retain top performers. This works at seed and Series A stages but becomes prohibitively expensive at later stages, when equity grants lose motivational power and cash compensation becomes necessary.

Part 6: Investment Thesis and Strategic Positioning

Why Iran’s Startup Ecosystem Matters

Despite macroeconomic deterioration, Iran’s startup ecosystem warrants institutional attention for three reasons:

Defensibility Through Constraint: Sanctions and capital controls have created defensible local champions in e-commerce (Digikala), fintech (ZarinPal), mobility (Snapp), and other sectors. These companies have established network effects and customer switching costs that international competitors cannot easily overcome through late market entry.

Demographic and Skill Advantages: The concentration of young, technically skilled workers willing to accept below-market compensation (due to constrained domestic options) creates conditions for building capital-efficient software and services companies at competitive cost structures unavailable in global hubs.

Optionality on Regional Expansion: Several Iranian startups (Torob, Snapp, fintech platforms) have begun expanding to neighboring markets in the Middle East and Central Asia, where regulatory environments may be less restrictive but technology adoption trails Iran’s. The companies’ experience navigating Iranian constraints may prove advantageous in adjacent markets.

Investor Risk-Return Profile

Investment in Iran’s startup ecosystem should be structured as a high-risk, patient capital deployment with a 7-10 year time horizon. Risk factors include geopolitical escalation (further sanctions, conflict), macroeconomic volatility (currency crises, banking sector stress), and regulatory uncertainty. Return scenarios depend heavily on geopolitical de-escalation and potential sanctions relief—conditions outside investor control.

For investors with geopolitical conviction (e.g., those assuming eventual normalization of Iran-Western relations), exposure through carefully selected portfolio companies in resilient sectors (fintech, healthtech, logistics, B2B SaaS) offers optionality. For others, the risk-return profile remains prohibitive without explicit thematic conviction about regional geopolitical evolution.

Conclusion: Innovation Despite Constraints

Iran presents a study in how constraint and necessity can catalyze innovation at scale. The combination of a large, young, digitally native population, government-backed innovation infrastructure (Pardis Technology Park, INIF funding), and acute domestic market needs (payment processing, healthcare access, agricultural efficiency, electricity generation) has created an entrepreneurial ecosystem with genuine scale (3,728 startups, $676M in cumulative funding) and demonstrable successes (Snapp, ZarinPal, Digikala).

Yet this ecosystem remains fragile, sustained by domestic capital sources and vulnerable to macroeconomic shocks. The path to regional significance—and eventual global relevance—depends on geopolitical stabilization, currency stabilization, and sustained government commitment to innovation-focused industrial policy.

For strategic investors, entrepreneurs, and policymakers, Iran’s startup story demonstrates both the power of bottom-up innovation in response to structural constraints and the limits that macroeconomic instability imposes on growth trajectories. Understanding Iran’s tech ecosystem is therefore not merely a regional interest but a case study in how geopolitical constraint reshapes entrepreneurial dynamics globally.

official iran government websites

| Government of Iran | Government of Iran |

Read more country case studies done before this.

| china | china |

| hong kong | hong kong |

| japan | japan |

| sinagpore | singapore |

| taiwan | taiwan |

| uAE | UAE |

| vietnam | vietnam |

| saudi arbia | saudi arbia |

| Malaysia | Malaysia |

| india | india |

| south korea | south korea |

Yo, what’s up? Just downloaded 98winapp and digging the mobile experience. Pretty slick design and loading times are quick. Makes betting on the go a breeze. Definitely recommend giving it a download if you’re always on the move. Get the app here 98winapp.