Israel’s

Israel has engineered one of the world’s most remarkable economic transformations: a nation of 9.7 million people has become the “Startup Nation,” spawning 90 active technology unicorns with combined valuations exceeding $63 billion, commanding disproportionate share of global venture capital, and establishing technological dominance in cybersecurity, artificial intelligence, fintech, and defense technology. This case study examines the structural foundations of Israel’s innovation economy, the unique military-university-startup nexus that accelerates R&D commercialization, and the geopolitical factors that simultaneously enable and constrain future growth.

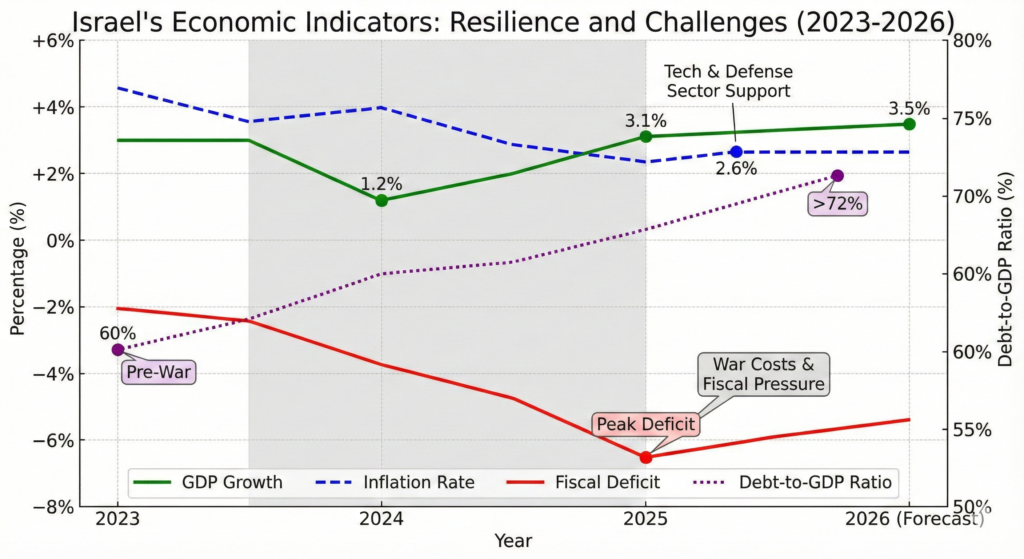

isreal Economic Performance: Resilience Despite Conflict

Israel’s macroeconomic trajectory through 2024-2025 demonstrates remarkable resilience amid sustained conflict with Hamas and Hezbollah—a geopolitical context that would paralyze most economies yet appears largely contained within defense spending while high-tech sectors continue expanding.

2024 Performance: Real GDP grew 1.0% in 2024, significantly below historical averages (Israeli long-term average: 3-4% annually), reflecting the economic drag from military mobilization, reserve duty obligations, and regional instability. This represents the weakest year since the October 2023 Hamas attack, suggesting the economy’s vulnerability to sustained conflict.

2025 Recovery: The picture shifted materially in 2025. Q1 registered 3.4% annualized growth, with Q3 reaching a dramatic 12.4% annualized expansion (revised upward)—the strongest quarterly performance since Q1 2024 and reflective of accelerating high-tech sector activity. Full-year 2025 growth forecasts ranged from 3.1% to 3.3%—substantially higher than 2024 but below pre-conflict trend.

The OECD projects 4.9% growth in 2026, contingent on continued geopolitical stability and absence of major escalation. However, this forecast carries substantial uncertainty: risks include renewed conflict with Hezbollah, potential Iran escalation, or broader Middle East instability.

Inflation Context: Inflation remained sticky above the Bank of Israel’s 1-3% target, reaching 3.6% by April 2025, constraining monetary policy flexibility. Defense spending surges and supply-chain disruptions created pricing pressures despite global disinflation trends. However, the high-tech sector—Israel’s growth engine—remains largely insulated from inflation impacts through global pricing power.

The Startup Ecosystem: “Startup Nation” at 90 Unicorns

Israel’s startup ecosystem achieved historic scale by 2025: 90 active technology unicorns with $63 billion+ combined valuation, 3,006 registered startups, and $12.2 billion in annual funding (up 31% year-over-year in 2024). This concentration of innovation is extraordinary relative to population—roughly 9 unicorns per 1 million inhabitants, far exceeding global averages.

Unicorn Concentration: The ecosystem demonstrates clear sectoral concentration:

- Cybersecurity dominance: Wiz ($12 billion valuation) represents 19% of total unicorn value, with 40+ cybersecurity unicorns collectively valued at ~$22-25 billion (39% of ecosystem).

- Enterprise software/infrastructure: DriveNets ($2.5B), Hibob ($2.4B), and similar platforms comprise ~25% of ecosystem value, addressing workflow automation and data infrastructure.

- Blockchain/cryptography: StarkWare ($8 billion) and related firms represent emerging high-value segment reflecting Web3 capital concentration.

- Fintech: Multiple unicorns (Earnix $2B+, Simply $1B+) address payments, risk assessment, and insurance technology.

- AI-native companies: AI21 Labs ($1.4B), Hailo ($1.2B semiconductor inference), and emerging AI security firms show growing sector.

- Gaming/consumer: Moon Active ($5B) demonstrates consumer-focused outlier in enterprise-heavy ecosystem.

Funding Dynamics (2024): Israeli startups raised $12.2 billion in 2024, with cybersecurity alone commanding $3.8 billion (31% of total startup funding) despite representing only 7% of ecosystem companies by count. This disparity reflects cybersecurity’s outsized strategic importance, pricing power, and mature business models. Corporate-backed funding represented 24% of all 2024 investments, with 83% of Tel Aviv startups receiving corporate partnership investment.

2025 Trends: The most dramatic 2025 development was cybersecurity funding’s new record of $4.4 billion, up 9% from 2024, with funding rounds jumping 46% to 130 deals total. This acceleration reflects dual drivers: (1) existential geopolitical threats elevating cybersecurity priority globally, and (2) AI-driven demand for threat detection, response automation, and AI-system security.

AI security emerged as the dominant new seed-stage formation category in 2025, with 12 companies raising capital specifically in AI security and 11 in risk automation—signaling market recognition of AI-specific threats and opportunities.

isreal Cybersecurity: Israel’s Flagship Sector

Cybersecurity represents Israel’s most distinctive technological achievement and global competitive advantage. The sector is not merely large but structurally positioned at the intersection of geopolitical necessity, enterprise demand, and emerging AI threats.

Market Scale and Growth: The Israel cybersecurity market reached $1 billion in 2025 and is projected to reach $1.5 billion by 2030 (8.5% CAGR). Global context: Israeli cybersecurity companies raised private funding in 2024 equal to 40% of the total U.S. market, despite the U.S. having 30+ times Israel’s population.

Ecosystem Structure: 150+ active cybersecurity companies operate in Israel, with 40%+ of new startups (2022-2024) focusing on AI-enhanced cybersecurity. This represents a maturing market segmenting into:

- Traditional defense: Threat detection, vulnerability assessment, endpoint protection

- AI-augmented security: Machine learning-driven anomaly detection, autonomous response, behavioral analytics

- AI-system protection: Securing generative AI models, LLM safety, prompt injection defense, data pipeline integrity

- Identity and access: Machine-identity governance, Zero Trust frameworks, permissions management

Geopolitical Underpinning: Israel’s cybersecurity dominance rests partly on unique advantage: sustained, acute cyber threats from nation-state actors (Iran, Syria, Hezbollah, Hamas) requiring continuous innovation in threat detection and response. This “pressure cooker” environment accelerates product development cycles and validates technologies in real-world combat conditions—a brutal but undeniable competitive advantage unavailable to Western vendors.

Government support through the Innovation Authority, military R&D spillovers, and talent pipeline from military service create structural advantages competitors struggle to replicate.

Sector Leaders: Wiz (cloud security), Cato Networks (network security), Transmit Security (identity), Silverfort (authentication), Aqua Security (container security), and dozens of emerging AI-security startups dominate headlines and attract global VC capital.

isreal Fintech: Digital Finance at Scale

Israel’s fintech market reached $1.016 billion in 2024 and is projected to reach $3.812 billion by 2033 (16.7% CAGR). The sector addresses digital payments, risk analytics, insurtech, wealthtech, and blockchain—sectors where Israeli companies bring both technological sophistication and geopolitical advantages in secure financial infrastructure.

Regulatory Innovation: Open banking adoption, fintech licensing frameworks, and collaboration between central banks and startups created favorable conditions. Fintech platforms increasingly serve as core infrastructure for global financial institutions, not peripheral suppliers.

AI-Driven Risk and Fraud: Israeli fintech specialization in AI-driven fraud detection, transaction intelligence, and risk scoring creates defensible moats. Companies leverage military-grade data science talent to build proprietary threat-detection models that capture market share through superior accuracy and speed.

Global Integration: March 2025 developments highlighted Israeli fintech platforms expanding partnerships with global financial institutions around AI-driven fraud analytics, risk scoring, and transaction intelligence—deepening integration into global financial architecture rather than competing for consumer market share.

isreal Artificial Intelligence: Emerging Leadership

While Israel trails the U.S. in large language model research, the country has positioned itself as a leader in applied AI, specialized models, and AI security—sectors often undervalued relative to foundational AI research but generating substantial commercial value.

AI Investment Trends: Early-stage angel investing in AI doubled in 2024, with TBD VC launching a $35 million fund in April 2025 specifically for Deep Tech Israeli founders at pre-seed and seed stages.

AI21 Labs ($1.4 billion valuation): The company represents Israel’s most prominent AI research and commercialization effort, developing instruction-following models (“Jurassic” family) and AI-powered applications. Though smaller than OpenAI or Anthropic, AI21 demonstrates that Israel can build substantial AI companies through focused engineering and specialized models.

Hailo ($1.2 billion): Semiconductor design for efficient AI inference at the edge, addressing latency and power constraints of on-device AI—a specialized niche where Israeli firms excel.

AI-Security Convergence: The most exciting 2025 development is Israeli companies (Zenity, Noma Security, Prompt Security, Pillar Security, Twine Security) pioneering AI security—tools to manage identity, permissions, and misuse risks in generative AI systems. This emerging sector, barely recognized 18 months ago, has become a primary seed-stage category, suggesting Israel is positioning itself as a leader in a genuinely new market.

isreal Deep-Tech Infrastructure and Specialized Sectors

Beyond consumer-facing sectors, Israel excels in deep-tech infrastructure, specialized semiconductors, and industrial automation—sectors requiring sustained R&D and capital intensity but commanding premium valuations.

Semiconductors and Silicon Design: Next Silicon ($1.5B, AI accelerators), Hailo (inference chips), and specialized design houses work with TSMC on custom silicon for specific applications (AI, storage, networking). Israel’s strength lies in algorithm-to-silicon translation—designing optimal chip architectures for specific workloads.

Energy Storage: StoreDot ($1.5B, backed by Samsung and BP Ventures) represents Israel’s most advanced deep-tech company, developing extreme fast-charging batteries (100% charge in under 10 minutes) through electrochemistry and materials science. The company exemplifies Israeli deep-tech: solving physics-hard problems through sustained R&D, securing strategic corporate partnerships, and building defensible IP moats.

Agritech (Not Yet Major Sector): Israel’s water scarcity and advanced farming techniques created competitive advantage in precision agriculture, irrigation optimization, and crop analytics—sectors with global relevance as climate change stresses agriculture. However, agritech remains relatively small compared to cybersecurity or fintech.

The Military-University-Startup Nexus: Unique Competitive Advantage

Israel’s startup ecosystem benefits from a distinctive institutional structure unavailable to most competitors: a 3-year military service requirement (for most citizens) that funnels young talent into cutting-edge technology development (cyber units, signals intelligence, AI research), followed by transition to civilian startup ventures with accumulated expertise.

Military R&D Spillovers: Israel’s defense spending (approximately 5% of GDP, driven by security threats) funds extensive research in cybersecurity, signals processing, autonomous systems, and advanced materials. Much of this defense research gets commercialized through military veterans founding startups or acquiring technologies developed in defense contexts.

Top Academic Institutions: Hebrew University, Tel Aviv University, Technion (Israel Institute of Technology), and Ben-Gurion University conduct world-class research in computer science, engineering, and materials science. These institutions, despite more limited resources than US equivalents, produce entrepreneurs and researchers who frequently found or join startups.

Talent Density and Ecosystem Effects: The concentration of talent—military veterans, university researchers, successful serial entrepreneurs—in Tel Aviv and other tech hubs creates network effects, knowledge spillovers, and social capital enabling rapid startup formation and scaling.

Geopolitical Constraints and Strategic Vulnerabilities

Israel’s innovation economy faces substantial geopolitical constraints:

Military Spending Diversion: Defense spending absorbs capital and talent that might otherwise flow to civilian innovation. The October 2023 conflict resulted in 360,000+ reserve mobilizations, creating temporary labor shortages and productivity loss. Extended conflict could materially constraint growth.

Regional Instability Risk: Renewed conflict with Hezbollah, Iran escalation, or broader Middle East instability could devastate the innovation ecosystem through capital flight, talent departure, and investor risk aversion toward Israeli assets.

Brain Drain: Top Israeli talent, particularly in AI and semiconductors, frequently relocates to the U.S. (Silicon Valley, NY) or Europe for larger companies, higher valuations, and perceived safety. The ecosystem must continuously regenerate talent to sustain dominance.

Export Dependence and Geopolitical Leverage: The high-tech sector represents 20% of GDP and 53% of exports—extraordinary concentration. This dependence means geopolitical events directly impact economic growth. Conversely, it gives the U.S. and allies strategic leverage to restrict Israeli technology exports if policy conflicts emerge.

Venture Capital Ecosystem: Global Connections with Local Innovation

Israel’s VC landscape demonstrates exceptional depth: Insight Partners, Bessemer Venture Partners, Sequoia Capital, Pitango, and Aleph appear repeatedly across unicorn portfolios, with corporate investors (Samsung, Intel, BP, Salesforce) embedding strategic investment alongside pure financial VCs.

Investor Concentration: The top five investors back 30%+ of unicorns, indicating ecosystem maturity with established patterns of founder-investor relationships and successful exits creating returnful vintages that attract new capital.

Early-Stage Dynamics: 2024 saw angel investment double, suggesting ecosystem foundation strengthening through increased seed-stage capital. This is critical for long-term ecosystem health: without robust early-stage investment, the pipeline of future unicorns contracts.

Exit Market: Acquisition remains the dominant exit (11% of cybersecurity companies acquired), while IPO remains rare (1% of cyber companies). This reflects global tech trends (private-equity consolidation, strategic M&A) and Israel’s smaller domestic capital market. Most Israeli unicorns lack path to IPO unless they achieve $10B+ valuations or relocate HQs to larger markets.

Conclusion: Peak Innovation Amid Geopolitical Uncertainty

Israel has achieved a remarkable economic transformation: a nation of 9.7 million with existential security threats has built a technology ecosystem rivaling much larger economies in scale, sophistication, and output. The 90 unicorns, $63 billion valuation, and $4.4 billion cybersecurity funding in 2025 represent authentic economic achievement and global competitiveness.

Yet this very success rests on precarious geopolitical foundations. The military-university-startup nexus that generates continuous innovation depends on sustained national mobilization, relative peace for entrepreneurship, and investor confidence in political stability. Extended conflict, regional escalation, or geopolitical isolation would rapidly unwind these advantages as talent departs, capital flees, and ecosystem network effects dissolve.

The 2025 Q3 GDP surge (12.4% annualized) and record cybersecurity funding suggest the startup nation’s resilience and the global demand for Israeli technology remain intact. However, the 2026 forecast deceleration to 3.3% growth and OECD cautions about geopolitical risks underscore the fragility underlying this strength.

For Israel, the next five years present a strategic choice: lean into technological dominance in cybersecurity, AI, and deep-tech to achieve economic resilience that reduces dependence on regional stability, or risk being trapped in a cycle where geopolitical volatility perpetually constrains growth despite technological prowess.

Government Services & Information

| ovExtra | GovExtra |

| Ministry of Foreign Affairs | Ministry of Foreign Affairs |

| Ministry of Finance | Ministry of Finance |

| Ministry of Interior | Ministry of Interior |

| Ministry of Communications | Ministry of Communications |

| Ministry of Tourism | Ministry of Tourism |

| Ministry of Health | Ministry of Health |

| Official Government of Israel Portal | Official Government of Israel Portal |

Read more country case studies done before this.