Japan Government Official Portal

Japan innovation and tech ecosystem 2026.

Japan stands at a critical juncture in its economic history. As the world’s fourth-largest economy with a nominal GDP of $4.11 trillion (2024), the country faces structural headwinds from demographic decline, persistent deflation psychology, and a debt-to-GDP ratio of 252.6%—among the world’s highest. Yet paradoxically, Japan maintains formidable competitive advantages in robotics, semiconductors, precision manufacturing, and increasingly, artificial intelligence. This case study examines Japan’s technology economy, the resilience of its competitive positioning, and the policy responses designed to sustain economic vitality through the 2025-2032 period.

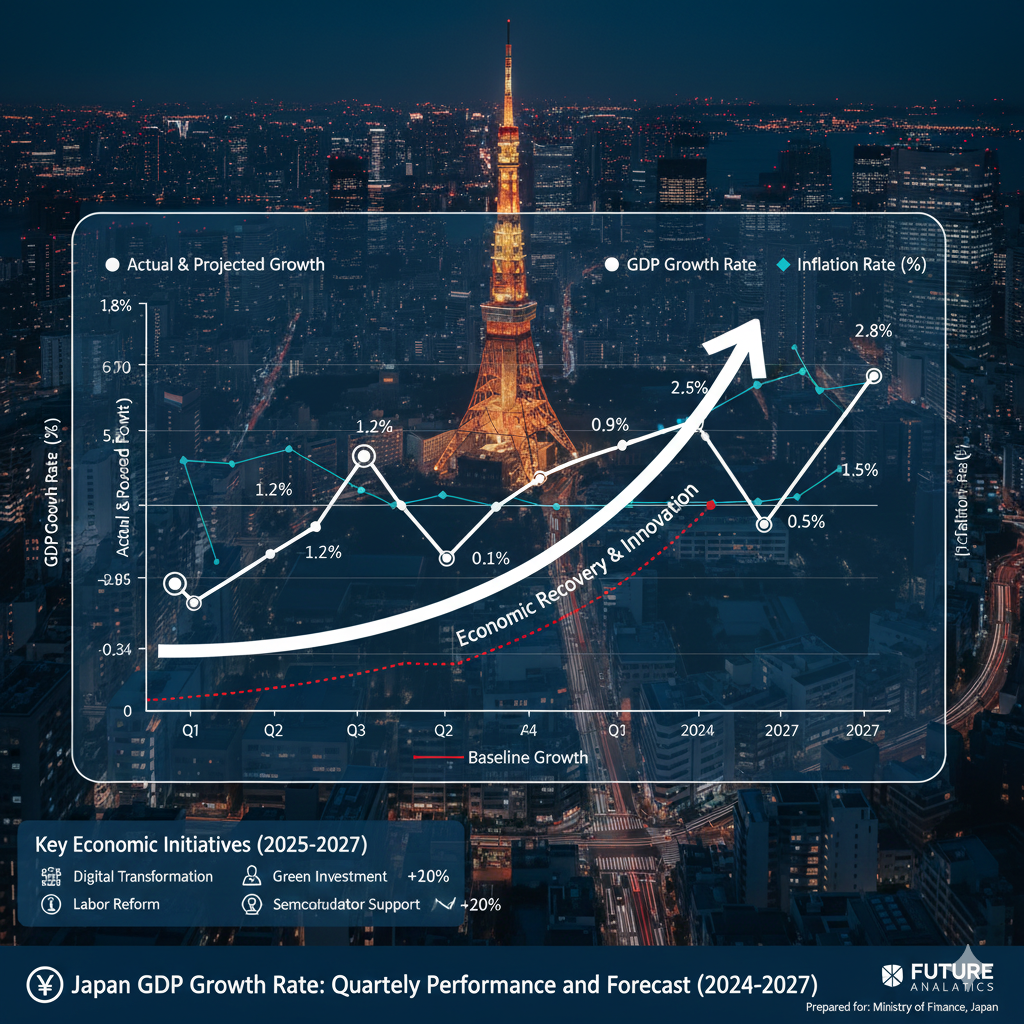

japan Economic Performance: Volatility Amid Structural Challenges

Japan’s economic growth remains stubbornly modest despite nominal GDP expansion of 3% in 2024. Real GDP growth of only 0.1% reflects the persistent challenge of separating nominal (price-adjusted) increases from genuine productive expansion. The 2024-2025 period exemplifies this dynamic: nominal growth masks real stagnation.

Japan GDP Growth Rate: Quarterly Performance and Forecast (2024-2027)

Q2 2025 delivered surprising strength: 2.2% annualized growth (revised upward from initial 1.0% estimate) and 0.5% quarterly expansion, exceeding economist consensus and demonstrating resilience despite intensifying US tariffs. However, Q3 2025 contracted sharply—minus 2.3% annualized (-0.6% qoq)—marking the first quarterly contraction since Q1 2024, with business spending declining for the first time in three quarters.

The Bank of Japan revised its FY 2025-26 growth forecast to 0.6% (up from 0.5%), supported by private consumption growth from robust wage increases and government subsidies for green and digital investment. However, the OECD projects more modest expansion: 0.7% for 2025 and 0.4% for 2026, with long-term projections near 2.0%.

This tepid growth trajectory reflects structural constraints: an aging and shrinking population, deflationary mindsets persisting despite nominal inflation, elevated public debt requiring fiscal restraint, and global trade uncertainty from tariff escalation. Unlike younger, faster-growing economies (India, Southeast Asia), Japan lacks demographic tail winds. Rather, the country must sustain productivity and living standards for a declining workforce, a fundamentally different economic challenge. Japan innovation and tech ecosystem 2026.

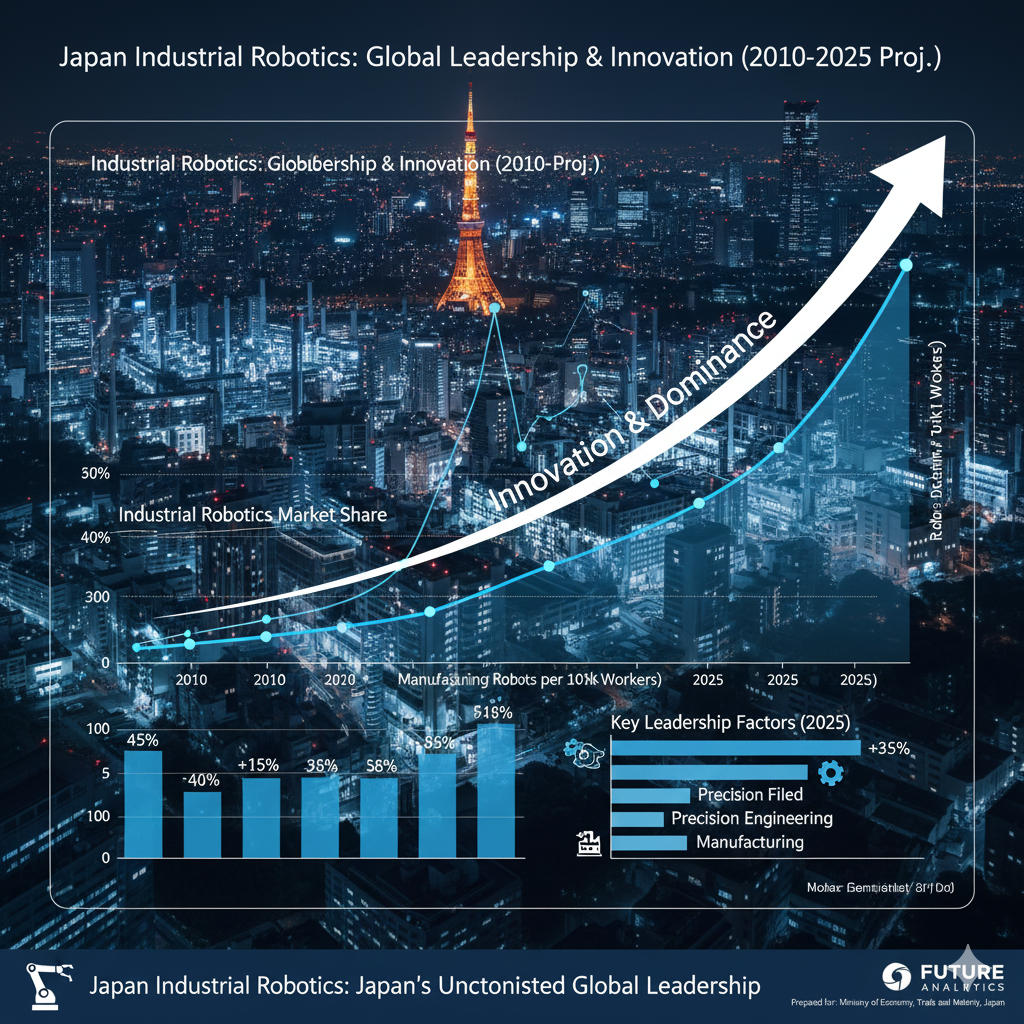

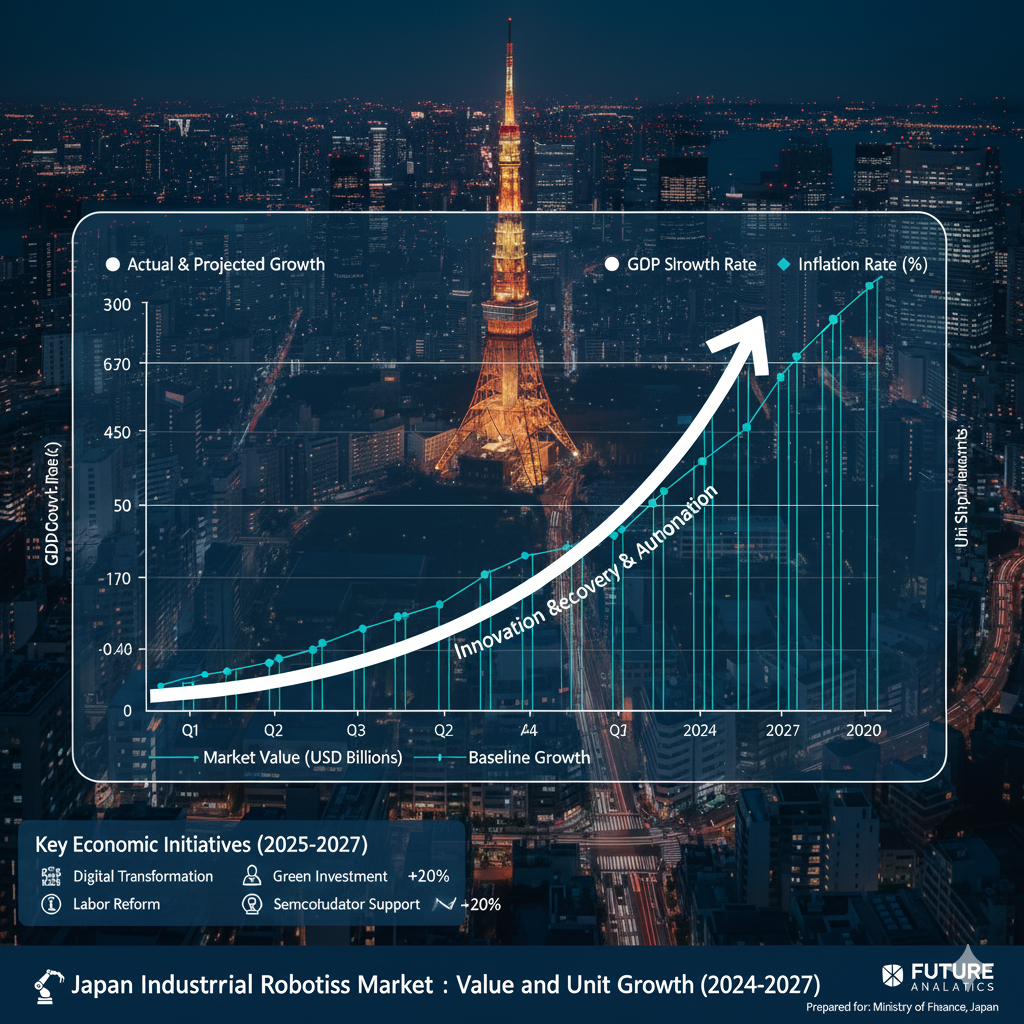

japan Industrial Robotics: Japan’s Uncontested Global Leadership

Industrial robotics represents Japan’s most distinctive technological achievement and source of sustained competitive advantage. The country produces 45% of all industrial robots globally, operates 300,000+ robots (the largest installed base), and maintains an extraordinary robot density of 631 robots per 10,000 manufacturing workers—the highest globally. This ecosystem advantage is structural, not cyclical.

Japan Industrial Robotics Market: Value and Unit Growth (2024-2030)

The market itself demonstrates robust growth: Japan’s industrial robotics market reached $2,970.5 million in 2024, expanding to $3,456.4 million by 2025, with projections to $5,773 million by 2030 (10.8% CAGR). In unit volume, 42,000 robots were installed in 2024, growing to 49,000 in 2025 and forecast to reach 80,000 by 2030 (10.4% CAGR). One aggressive projection suggests the market could reach $17.21 billion by 2033 at 23.33% CAGR, contingent on faster AI integration and broader SME adoption.

Leading companies—Fanuc, Yaskawa, Kawasaki, and Mitsubishi Electric—are driving innovation in three critical directions:

- Collaborative Robots (Cobots): Modular, flexible systems enabling human-robot interaction for precision tasks, high-mix manufacturing, and small-scale production. Cobots reduce capital requirements for SMEs and address safety concerns around traditional industrial robots.

- Autonomous Mobile Robots (AMRs): Mobile platforms equipped with AI for flexible warehouse logistics, material handling, and dynamic task allocation. AMRs address the “last-mile” automation challenge where traditional fixed-position robots prove inefficient.

- AI-Integrated Systems: Integration of artificial intelligence, IoT, and machine learning enables predictive maintenance, real-time process optimization, and adaptive manufacturing. AI integration reduced manpower requirements by approximately 30% when deployed in Japanese factories.

The government’s Society 5.0 initiative explicitly supports this trajectory, aiming to merge digital technologies with human capabilities through coordinated investment in robotics, smart manufacturing, and Industry 4.0 adoption. This policy framework ensures sustained funding and regulatory support for robotics expansion.

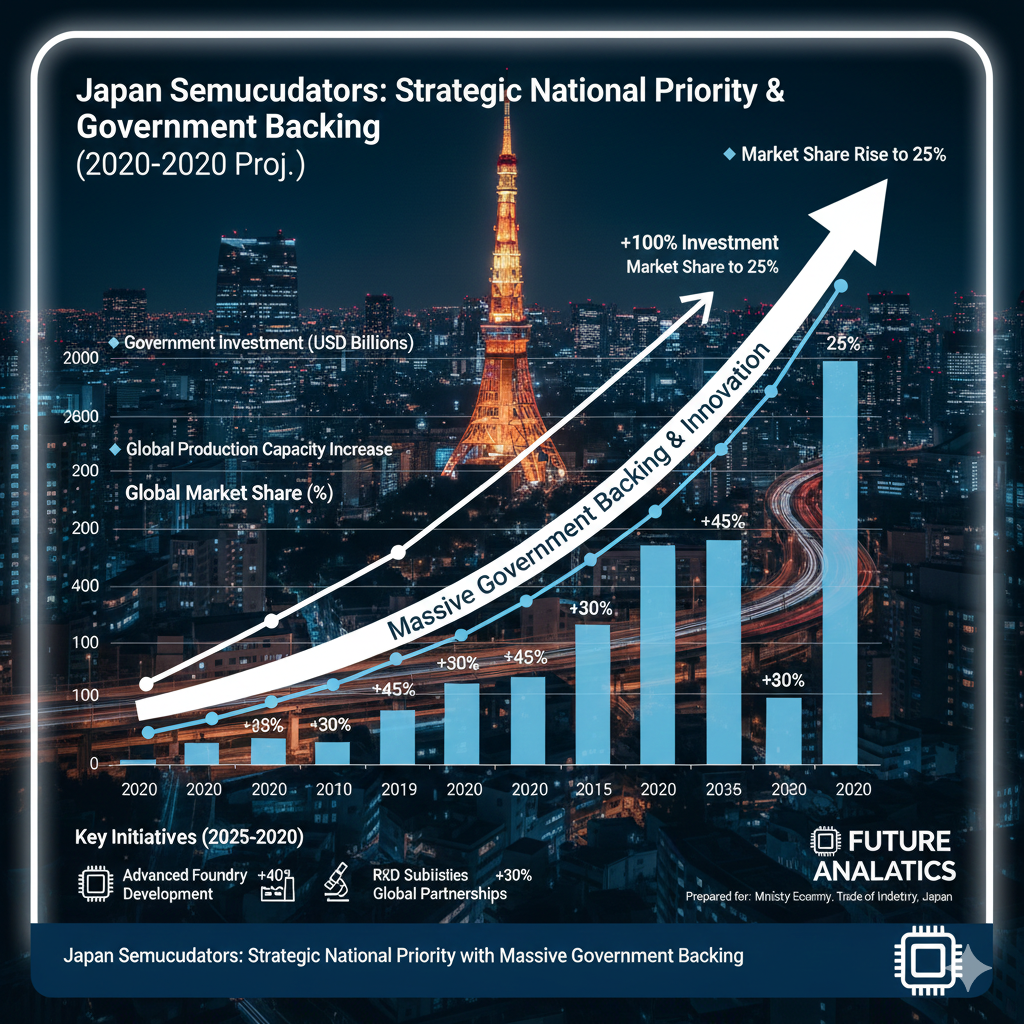

japan Semiconductors: Strategic National Priority with Massive Government Backing

Japan’s semiconductor industry, once globally dominant before TSMC and Samsung surpassed it in the 2000s, is undergoing deliberate government-led revitalization. The sector represents not merely commercial opportunity but strategic necessity—semiconductors underpin national security, industrial leadership, and AI capability.

Japan Semiconductor Market: Growth Scenarios

Market Size and Government Targets: Japan’s semiconductor device market stood at $56.83 billion in 2025 and is projected to reach $70.47 billion by 2030 (4.4% CAGR). However, more aggressive projections suggest the market could reach $175.25 billion by 2034 (15.8% CAGR) if Japan successfully executes its “Made in Japan” semiconductor strategy.

The Ministry of Economy, Trade and Industry (METI) set an ambitious target: triple domestic semiconductor industry sales from approximately 5 trillion yen (2020) to 15 trillion yen by 2030—representing a 3x increase over a decade. To fund this transition, Japan invested nearly 4 trillion yen in the semiconductor sector during FY 2021-2023, with strategic allocations to Taiwan Semiconductor Manufacturing Company (TSMC) for its JASM (Japan Advanced Semiconductor Manufacturing) foundry in Kumamoto Prefecture and to Rapidus Corporation for next-generation process development.

TSMC’s Kumamoto Facility and Cluster Formation: The JASM foundry, established through Japanese government incentives, represents a watershed moment. Commercial land prices in Kumamoto climbed over 10% in 2024 as suppliers—compressor manufacturers, gas suppliers, deionized water vendors—clustered around the facility to minimize downtime and optimize yields. This vertical integration creates a self-reinforcing ecosystem. Sony’s legacy in image sensor manufacturing compounds the advantage, creating a “full-stack corridor” from wafer etch through camera module assembly.

2nm Process Technology Roadmap: Japan is pursuing a collaborative industry-government-academia model to develop 2nm process technology with targeted mass production in 2027. This ambitious timeline, if achieved, would position Japan as a co-leader alongside TSMC and Samsung in cutting-edge process nodes. Advanced packaging technologies based on 2nm research will further differentiate Japanese semiconductor capabilities.

Device Composition and Strategic Positioning: Integrated circuits comprise 86.07% of Japan’s semiconductor market (2024), sustained by three pillars: (1) bespoke AI accelerators for specialized workloads; (2) automotive SoCs for EV and autonomous vehicle control systems; and (3) multilayer 3D NAND for cloud storage. Sensors and MEMS are growing fastest at 5.8% CAGR through 2030, driven by IoT proliferation and industrial automation.

Japan’s strategic approach differentiates by node and application. Sub-7nm lines support AI and high-performance computing, while 40-65nm mature nodes serve automotive electronics and industrial controls. This “dual-track” strategy avoids over-reliance on any single customer vertical and ensures balanced capacity utilization across semiconductor cycles. Japan innovation and tech ecosystem 2026.

RF Components and Substrate Dominance: Japan maintains formidable strength in communication infrastructure semiconductors (29.52% of market revenue, 2024), particularly in GaN (gallium nitride) RF filters and duplexers for 5G macro cells and optical-transport equipment. Advanced ceramic substrates, where Japanese suppliers dominate globally, represent a defensible moat in an era of RF densification.

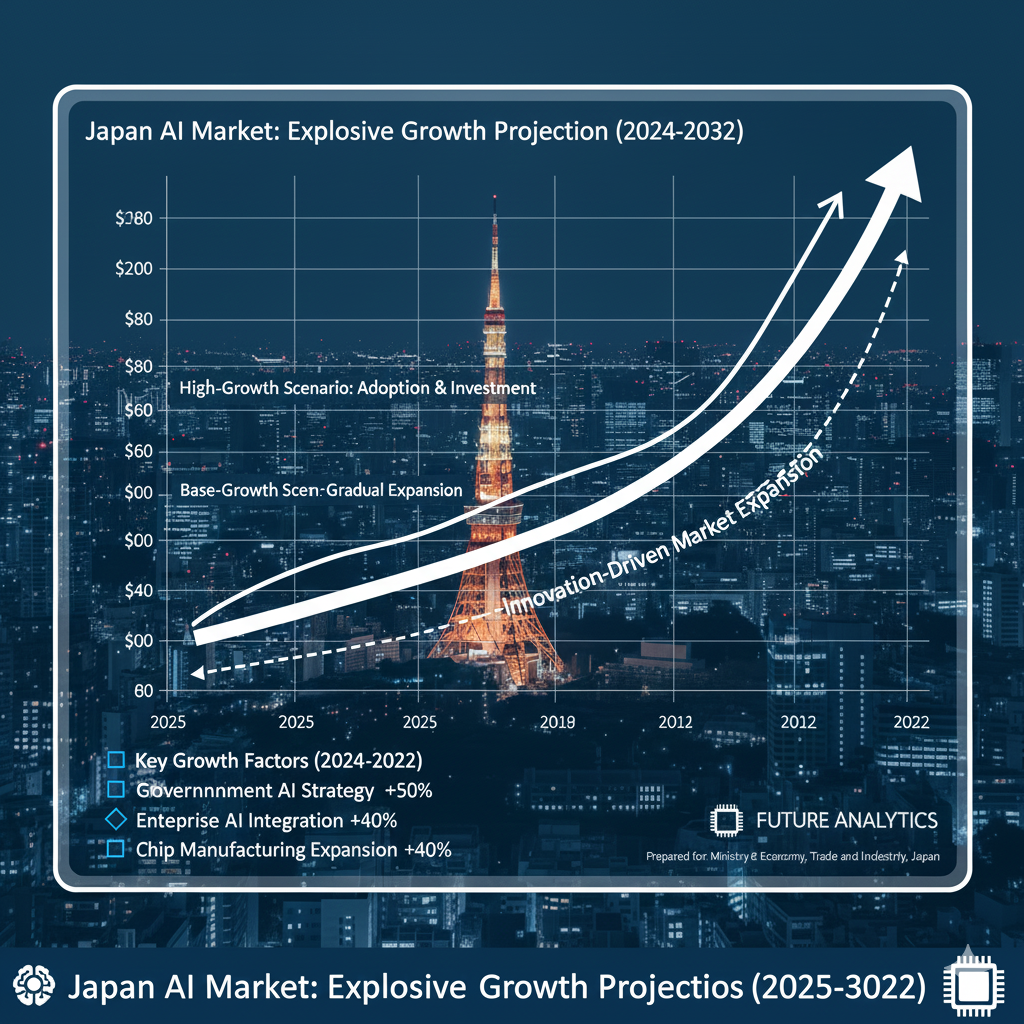

Artificial Intelligence: Japan’s Emerging Growth Engine

While Japan trails the US and China in large language model development and foundational AI research, the sector is experiencing extraordinary acceleration.

Japan AI Market: Explosive Growth Projection

Market Scale and Growth Rate: Japan’s AI market was valued at $11.84 billion in 2024 and is projected to reach $15.64 billion in 2025, expanding to $123.90 billion by 2032—representing an extraordinary 34.4% CAGR. This growth rate exceeds semiconductor growth (4.4% CAGR) and approaches robotics expansion (23.33% CAGR by 2033), positioning AI as Japan’s fastest-growing technology sector.

The AI Robotics sub-segment alone reached $1.06 billion in 2025, with rapid expansion anticipated as AI-powered robots address labor shortages in aging-population contexts.

Segment Composition: The market spans hardware (GPUs, FPGAs, ASICs, CPUs), memory systems, storage devices, and software/services (strategy consulting, system integration, model development, process automation, training, customer experience enhancement, support).

Leading Companies and Innovation Hubs: Japanese AI startups and established firms—including Preferred Networks (AI infrastructure), ABEJA (enterprise AI applications), and Leapmind (specialized AI chips)—are building differentiated solutions. The government’s IndiaAI Mission support (announced October 2025) selected ten cutting-edge Japanese startups for advanced AI development, signaling strategic commitment to indigenous AI capability building beyond IT outsourcing.

Strategic Applications: Data center demand from hyperscale cloud infrastructure and sovereign AI clusters drives growth. Memory-bandwidth requirements propel high-layer NAND shipments (complementing semiconductor expansion), while proprietary controller ICs and accelerators create ecosystem “stickiness” that ties Japanese semiconductor suppliers to AI infrastructure vendors.

Catch-up Challenges: While 34.4% growth is impressive in absolute terms, Japan remains dependent on Western foundational models and chip designs. The country excels in implementation, optimization, and vertical application (robotics control, manufacturing optimization, healthcare diagnostics) rather than originating breakthrough architectures. Success hinges on whether Japan can transition from importing AI frameworks toward developing indigenous large language models and foundational research capabilities.

japan Advanced Manufacturing: Automation, Precision, and Efficiency

Japan’s manufacturing ecosystem combines robotics leadership, precision culture (Kaizen philosophy), and automation adoption to sustain industrial competitiveness despite labor constraints.

Process Automation Market: The Japan process automation market reached approximately $4 billion in 2024 and is growing at 7.3% CAGR. Automation targets logistics (warehousing, packaging, transportation), food processing, pharmaceutical manufacturing, and healthcare—sectors where labor scarcity, quality demands, and 24/7 operations justify capital investment.

Sectoral Focus: Automotive remains the core driver, with strict manufacturing standards, just-in-time supply chains, and EVs requiring precision assembly. Electronics manufacturing leverages Japan’s strengths in miniaturization and quality control. Precision machinery, semiconductors, and medical devices represent high-value manufacturing where automation precision justifies investment.

Technology Integration: Modern Japanese factories integrate IoT sensors, cloud-based data analytics, and AI-driven optimization. Predictive maintenance algorithms, enabled by sensor-generated operational data, reduce unplanned downtime—critical in just-in-time systems where supply disruptions cascade through networks. Real-time process monitoring and adaptive control systems enhance quality while reducing waste.

Semiconductors and Materials: Japan’s Durable Moat

Japan’s semiconductor advantage increasingly rests not on foundry or chip design leadership, but on materials, equipment, and specialized components where Japanese suppliers enjoy structural advantages difficult for competitors to replicate.

Advanced Materials: Ceramics for RF components, specialized substrates for power semiconductors, precision chemicals for wafer processing—sectors where Japanese suppliers maintain 50%+ global market share in multiple sub-segments. These materials represent bottlenecks for competitors’ scaling, creating pricing power and strategic leverage.

Packaging and Assembly: Advanced packaging technologies—3D interconnects, chiplet integration, thermal management—where Japanese suppliers contribute specialized capabilities. As semiconductor manufacturing becomes increasingly complex, packaging becomes a competitive bottleneck, favoring Japanese equipment and materials vendors.

Equipment Supply: While Dutch ASML dominates lithography tools, Japanese suppliers excel in deposition, etching, and inspection equipment. The concentration of Japanese equipment vendors around clusters like Kumamoto reinforces regional advantages.

Demographics and Innovation Incentives

Japan’s aging population—with the world’s longest life expectancy and declining birth rate—paradoxically creates strong innovation incentives in robotics, HealthTech, medical devices, and automation. Labor shortages are not a constraint to overcome but a stimulus for innovation.

Rather than wage inflation (which erodes cost competitiveness), aging populations incentivize labor-saving innovation, surgical precision in manufacturing, and productivity enhancement through technology. Japanese companies have internalized this dynamic more thoroughly than younger-economy competitors, embedding automation and efficiency into corporate DNA.

HealthTech Innovation: Medical device manufacturing, surgical robots, and hospital automation address aging-population healthcare demands. Companies like Olympus (endoscopy), Shimadzu (diagnostic imaging), and Sony (image sensors for medical devices) leverage precision manufacturing capabilities toward healthcare applications. Laboratory automation (growing at 6.19% CAGR through 2033) addresses research productivity demands in aging-focused medical research.

Competitive Positioning: Strengths and Vulnerabilities

Structural Strengths:

- Robotics dominance: 45% global production, 631 robots per 10K manufacturing workers (highest globally)

- Semiconductor materials/packaging: 50%+ global share in critical sub-segments

- Precision manufacturing culture: Kaizen philosophy, quality obsession, continuous improvement embedded in organizational DNA

- Government support: Consistent, substantial strategic investment (4 trillion yen semiconductor fund, Society 5.0, green subsidies)

- Vertical integration: Suppliers clustered to optimize yields and minimize downtime (Kumamoto model replicable)

- Brand reputation: Global trust in reliability, precision, and quality

Structural Vulnerabilities:

- Demographic decline: Aging, shrinking population constrains domestic demand and labor force

- Deflation psychology: Structural pricing pressures limit inflation (even as nominal inflation rises)

- Debt burden: 252.6% debt-to-GDP ratio constrains fiscal flexibility for future crises

- Geopolitical exposure: Export-dependent economy vulnerable to tariff escalation, supply chain disruption

- AI catch-up: Dependency on Western foundational models, limited indigenous LLM development

- Commodity import dependence: Energy, raw materials vulnerabilities in volatile global markets

- SME adoption barriers: High implementation costs of robotics and automation deter small enterprises from upgrading

Policy Framework and Strategic Initiatives

Government Strategy Pillars:

- Society 5.0: Coordinated digital transformation merging technology with human capabilities

- Semiconductor Revitalization: 4 trillion yen investment (FY 2021-2023), TSMC partnership, 2nm technology roadmap

- Green Investment Subsidies: Supporting automation and digital transformation for sustainability

- International Partnerships: TSMC foundry, Intel back-end automation collaboration, academic partnerships

These initiatives represent deliberate positioning toward resilience—reducing import dependence, securing supply chains, leveraging demographic constraints as innovation stimulus rather than burden.

Conclusion: Constrained Growth, Enduring Competitive Advantage

Japan’s economic trajectory through 2025-2035 will likely remain modest—0.5-2.0% annual growth—reflecting demographic realities that no policy can fully overcome. The country will not reclaim 1990s-era growth rates or even 2000s-era expansion.

Yet within this constrained growth context, Japan’s competitive advantages in robotics, semiconductors, precision manufacturing, and increasingly AI create a durable foundation for continued global relevance. The $2.97 billion industrial robotics market growing at 10.8% CAGR, the $56.83 billion semiconductor market with 34.4% CAGR AI expansion, and the potential $123.90 billion AI market by 2032 collectively represent substantial value creation.

Success hinges on three critical factors: (1) sustained government support for strategic technologies despite fiscal pressures; (2) successful execution of the 2nm semiconductor roadmap and TSMC partnership; and (3) Japan’s ability to transition from implementing AI systems toward developing foundational models and algorithms. If Japan achieves these transitions, the 2025-2035 period could witness the emergence of a different Japan—smaller population, lower growth, but higher per-capita productivity and value-add through technology leadership in robotics, semiconductors, and precision manufacturing.

Japan GDP Growth Rate: Quarterly Performance and Forecast (2024-2027)

Japan Industrial Robotics Market: Value and Unit Growth (2024-2030)

Japan AI Market: Explosive Growth Projection (2024-2032)