Myanmar economic sectors crisis 2026 .

Executive Summary

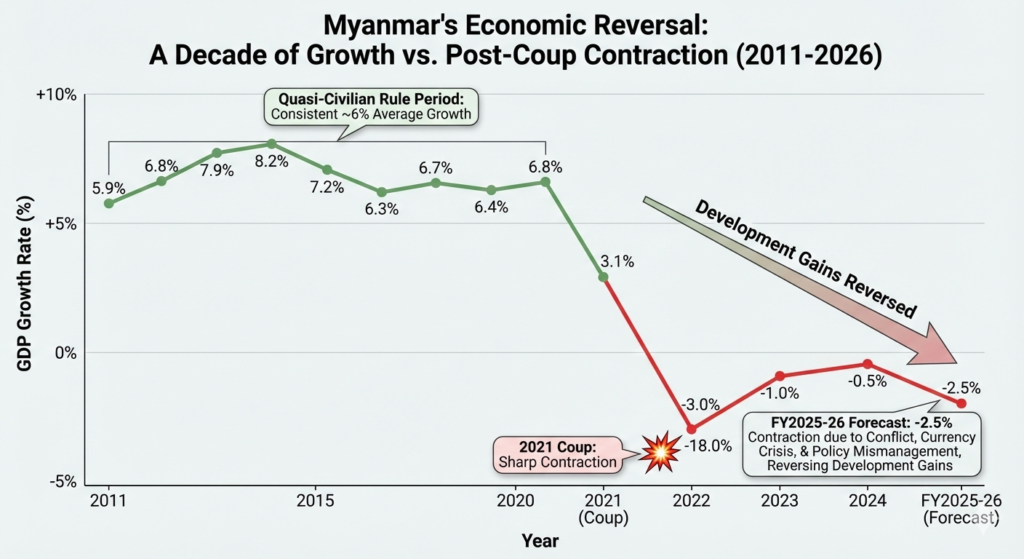

Myanmar stands at an economic precipice, having transitioned from a managed recovery (2011-2021) to near-total economic collapse following the February 1, 2021 military coup. Where the country recorded 6% average annual growth during a decade of quasi-civilian rule and partial liberalization, Myanmar now contracts at -2.5% (FY2025-26 ADB forecast) amid inflation exceeding 34%, currency depreciation of over 70% against the US dollar, and poverty affecting nearly half the population. This case study examines five critical sectors—energy and natural resources, agriculture, border trade and informal commerce, telecommunications and digital services, and manufacturing—to understand how military authoritarianism, international sanctions, currency collapse, and policy incoherence have systematically dismantled a fragile economy while inadvertently expanding parallel, illicit economies that finance armed conflict.

Unlike Bangladesh’s sectoral transformation strategy or standard development economics frameworks, Myanmar presents an inverted system: formal sector collapse has driven economic activity toward smuggling corridors, jade extraction by armed groups, and subsistence agriculture, reducing formal tax revenue and state capacity while enriching generals, ethnic armed organizations, and cross-border networks. Understanding Myanmar’s sectors requires abandoning conventional export competitiveness analysis and instead examining how state collapse creates survival economies disconnected from global markets. Myanmar economic sectors crisis 2026 .

Myanmar’s economy experienced consistent 6% average growth under quasi-civilian rule (2011-2021), followed by sharp contraction post-coup. FY2025-26 projects -2.5% contraction due to conflict, currency crisis, and policy mismanagement, reversing a decade of development gains

Myanmar’s decade-long recovery (2011-2021) created a false foundation for sustainable growth. The quasi-civilian government’s partial liberalization attracted foreign investment, deepened regional trade integration, and generated foreign exchange reserves. The February 2021 coup reversed these gains within months. By 2025, the economy has contracted for four consecutive years, inflation has reached historically unprecedented levels, and foreign direct investment has plunged 68.6% below pre-coup baselines. Economic output remains 13% below pre-COVID-19 levels—a performance that uniquely distinguishes Myanmar from every other ASEAN economy.

1. Energy and Natural Resources: Hard Currency Under Threat

Sector Overview and Strategic Importance

Myanmar’s oil and natural gas sector represents the economy’s largest source of foreign exchange and government revenue, generating approximately $2 billion annually in exports and constituting roughly 50% of the nation’s foreign currency earnings. This centrality to state finances provides the regime a critical cash flow source at a moment when sanctions have eliminated many alternative revenue streams.

Myanmar holds proven natural gas reserves of 23 trillion cubic feet, ranking 72nd globally but sufficient for sustained production across four major offshore fields: Yadana, Yetagun, Shwe, and Zawtika. These projects, initiated during the pre-coup liberalization era, involve complex international joint ventures including American (Chevron), French (Total), Japanese (Inpex), Thai (PTT), and Korean (Daewoo) entities, creating structural barriers to sectoral sanctions despite international pressure on the regime. Myanmar economic sectors crisis 2026 .

Production Dynamics and Export Structure

The Yadana Project, Myanmar’s largest offshore gas field, commenced production in 1999 and remains operational, generating majority gas flows to Thailand (80% of production) via pipeline, with Myanmar retaining 20% for domestic consumption and regional sales. Thailand’s energy dependence on Myanmar gas—anchored by long-term contracts—provides Myanmar with a resistant buyer base that continues purchasing despite coup-related reputational concerns and limited Western sanctions pressure on Thai importers.

China has emerged as a secondary but growing gas customer, with gas pipeline exports to Yunnan Province providing geopolitical leverage in Myanmar’s relationship with its larger neighbor. Japan purchases smaller quantities through LNG (liquified natural gas) arrangements, diversifying export risks across three countries.

However, production decline constitutes a looming structural threat. Myanmar’s natural gas output declined 11% from its 2021 peak, and the decline will accelerate as existing fields mature without replacement investment. The Yetagun Project, historically Myanmar’s second-largest field, ceased operations in April 2021, eliminating approximately 15-20% of production capacity. This decline trajectory, absent new field development and significant capital investment, suggests that gas export revenues will fall from current $2 billion levels to $1.2-1.5 billion by 2030 if no new projects reach production.

Petroleum Products: Import Dependence Crisis

A critical vulnerability compounds the gas sector’s decline: Myanmar imports 96% of refined petroleum products, primarily from Singapore, creating acute foreign exchange pressure and commodity price exposure. The regime attempted to address this structural deficit through the planned construction of a large domestic refinery, but political instability and capital constraints have prevented project advancement beyond planning stages.

The absence of refining capacity means that Myanmar cannot monetize crude oil resources domestically and instead experiences double currency loss: first from exporting gas at contracted rates without downstream value capture, and second from importing refined products at global market prices. Fuel shortages in 2024 generated extensive queuing at petrol stations and contributed significantly to transport cost escalation that fed inflationary spirals.

Joint Venture Complexity as Sanction Shield

The international partnership structure—involving Chevron (Yadana), Total (Yadana), PTT/Daewoo (Yadana/Zawtika), and Inpex (Zawtika)—creates a complicated sanctions architecture. While the Biden administration targeted Myanmar government funds in US banks and imposed restrictions on sensitive technology exports to the junta, Chevron and other international companies maintained operational presence throughout the coup period. This reflects the complexity of decoupling American foreign policy objectives (supporting democracy restoration) from energy security interests and shareholder obligations to international oil companies.

The regime’s reliance on gas revenues, combined with international companies’ sunk investments and Thai/Chinese contractual commitments, means that gas exports will likely continue even in scenarios of deteriorating political conditions. This paradoxically provides the junta a revenue stream precisely when sanctions have constrained alternative income sources—a dynamic that undermines sanctions’ leverage unless accompanied by energy-sector-specific measures targeting international financial flows.

Strategic Outlook

Unless new offshore discoveries materialize or technological advances lower development costs, Myanmar’s gas export revenues will contract to $1.2-1.5 billion by 2030, representing a 25-40% revenue loss relative to current levels. This trajectory occurs precisely as the regime’s fiscal position deteriorates (fiscal deficit at 5.5-5.7% of GDP), making the revenue cliff increasingly acute.

2. Mining: The Informal Economy Financing Conflict

Jade: Scale, Control, and Illicit Trade

Myanmar accounts for approximately 70% of global jade production, with deposits concentrated in Kachin State in the country’s northern regions. This concentration generates estimates of annual jade extraction valued at $30+ billion, with historical extraction over the past decade potentially exceeding $120 billion—figures that dwarf formal export revenues from any other sector.

However, the sector exists almost entirely outside formal state structures. Global Witness’s 2020 investigation revealed that military generals, ethnic armed organizations, and border guard militias collectively control jade extraction and export with minimal taxation or state oversight. The 2015 civilian government’s attempt to reform the sector through mining license restrictions and transparency mechanisms foundered on the military’s resistance, and post-coup the sector has devolved further into armed-group control and armed conflict over mining territories.

Post-Coup Dynamics: Competition and Coordination

Following the February 2021 coup, fighting erupted across Kachin State’s jade-mining regions, particularly in Hpakant—historically Myanmar’s largest single jade concentration. Paradoxically, this conflict has co-existed with extraordinary coordination among rival armed groups (Myanmar military, Kachin Independence Organization (KIO), United Wa State Army (UWSA), and Arakan Army (AA)) to accelerate jade extraction and export before political outcomes resolve.

This dynamic—enemies cooperating on resource extraction—reflects the sector’s extraordinary profitability and the realization among armed actors that political transitions inevitably involve resource-sharing negotiations. Rapid extraction maximizes each group’s bargaining position in post-conflict settlements. The consequence has been catastrophic: increased dangerous mining practices, over 200 deaths from major landslides in 2019-2020, and systematic environmental destruction including groundwater contamination and toxic dust generation.

Corruption and Elite Enrichment

Global Witness documented that Myanmar’s military commander and coup leader Min Aung Hlaing and his family have personally benefited from illicit jade trade proceeds, transforming the sector into “a personal treasure trove” and a source of political patronage financing the military apparatus. This creates a profound incentive alignment: the regime’s economic survival depends on unregulated jade extraction, pricing jade revenues below illicit market rates to maximize ethnic armed group cooperation, and providing smuggling passage to China (jade’s primary market) in exchange for border stability. Myanmar economic sectors crisis 2026 .

Rare Earth Minerals: Emerging Strategic Dimension

Parallel to jade extraction, illegal mining of rare earth elements (terbium, dysprosium, and others) has surged in northern Myanmar to meet Chinese demand for these inputs essential to electric vehicle motors, renewable energy equipment, and defense applications. Armed groups and Chinese companies have established joint mining operations in Kachin State, with minimal environmental regulation and zero formal royalty payments to Myanmar’s government.

The rarity of these elements globally and China’s strategic dominance in downstream processing creates a coercive demand dynamic: Myanmar armed groups extract at whatever volumes the market absorbs, Chinese companies process and export, and formal Myanmar government has no jurisdiction or revenue capture despite territorial sovereignty.

Financial Flows: Armed Groups Over State

The combined jade and rare earth mining sector likely generates $2-3 billion annually in revenue, but virtually none reaches Myanmar’s formal government treasury. Instead, revenues flow to:

- Myanmar military command structure (approximately 35-40% of flow)

- Kachin Independence Organization and other ethnic armed groups (40-45%)

- Border Guard Forces and pro-junta militias (10-15%)

- Chinese trading companies and smuggling networks (processing fees)

This inverted revenue structure means that Myanmar’s state apparatus depends on gas revenues while armed opposition forces depend on mining revenues, creating a structural stalemate where neither side can financially eliminate the other but both can finance indefinite conflict.

Environmental and Social Costs

The unregulated mining approach generates catastrophic environmental externalities: groundwater contamination with cyanide and mercury, soil degradation across thousands of acres, and toxic dust affecting respiratory health across mining regions. Local Kachin communities bearing these environmental costs receive minimal direct benefits, perpetuating grievances that sustain recruitment to ethnic armed organizations.

3. Agriculture: Rice Exports Under Stress

Production and Export Performance

Myanmar ranks third globally in rice exports, with FY2024-25 generating 2.48 million tonnes (MT) in exports valued at $1.12 billion. The sector employs millions of farmers across the country’s fertile deltaic regions and provides critical domestic food security for a 54-million-person population.

FY2025-26 targets 3 million MT in rice exports, with the first half (April-September) achieving 1.2 MT and generating $408 million. This performance reflects moderately resilient demand, particularly from China (the largest single buyer), the Philippines, and Spain, though global rice prices have softened from 2023-2024 peaks.

Myanmar’s exports remain heavily concentrated in three sectors: natural gas ($2B), informal minerals trade (estimated $1.5B), and rice ($1.1B). Garment exports have collapsed from pre-coup highs to $800M due to tariffs and sanctions. Formal trade statistics likely undercount illicit jade and mineral exports

Systemic Production Challenges

Myanmar’s rice sector faces interconnected crises that jeopardize medium-term production capacity:

- Input Cost Escalation: Currency depreciation has increased farmer acquisition costs for fertilizers, seeds, and equipment. Kyat depreciation of 24% (January 2024-May 2025) directly translates to 20-25% higher input costs for imported agrochemicals, with limited domestic substitutes.

- Conflict-Driven Supply Chain Disruption: Armed conflict in rural areas—particularly in Kayin, Kayah, Shan, and northern regions—has disrupted transport, prevented seasonal input delivery, and created security barriers to cultivation in strategic agricultural zones.

- Weather Extremes and Climate Shocks: A 7.7-magnitude earthquake in March 2025 and severe flooding during 2024 monsoon season caused significant agricultural production losses, with the World Bank forecasting agricultural sector contraction of 2.3% in FY2024.

- Labor Shortages: Military conscription (implemented February 2024) and ongoing Civil Disobedience Movement participation have pulled rural laborers from agricultural work toward resistance activities, exacerbating seasonal labor shortages during harvest periods.

- Farmer Distress: Falling producer prices combined with rising input costs have compressed farmer profit margins. The Myanmar Rice Federation (MRF) has recommended that farmers upgrade to higher-value varieties, aggregate supplies into cooperative-like structures, and negotiate directly with millers to improve price realization.

Market Structure and Price Dynamics

White rice with 5% broken rice content trades at approximately $320 per tonne (October 2025), while broken rice (B1/B2 grades) trades at $270 per tonne. These prices reflect global oversupply conditions and Asian competitive dynamics, with Indian and Thai rice competitors creating pricing ceilings that limit Myanmar’s ability to command premium prices despite quality advantages in certain varietal categories.

China’s emerging role as the dominant single buyer (346,919 MT in H1 FY2025-26) creates bilateral relationship risks: Myanmar’s ability to export depends on sustained Chinese demand and continued access across the China-Myanmar border, which could be leveraged for political concessions or diverted to support proxy actors.

Domestic Food Security Implications

While rice exports generate critical foreign exchange, domestic food security concerns are mounting. The World Food Program documented a 27% increase in food prices between October 2023 and April 2024, with conflict-affected regions experiencing 40-50% price spikes and extreme cases (Rakhine, Kayah states) exceeding 200% increases. This creates a perverse dynamic where rice exporters face domestic population food insecurity—a humanitarian crisis that could trigger migration pressures and internal instability independent of conflict itself.

4. Border Trade and Informal Commerce: The Replacement Economy

Scale and Mechanism

Myanmar’s border trade with Thailand, China, India, and Bangladesh represents a multi-billion-dollar informal economy that has expanded dramatically post-coup as the regime implemented severe import restrictions and foreign exchange controls. This trade is fundamentally dual-track: formal border-trade zones with documented transactions, and vast informal smuggling operations conducted through armed-group-controlled gates and unofficial crossing points.

The Thailand-Myanmar border presents the most systematic informal trade structure. Mae Sot, the Thai border town opposite Myawaddy in Myanmar’s Kayin State, serves as the primary smuggling hub, with Thai customs data indicating exports exceeding 110 billion Thai baht (approximately $3.2 billion USD) in calendar year 2024—approaching all-time records. However, Myanmar’s official import statistics from Thailand recorded only approximately $1.34 billion in the same period, revealing a $1.9+ billion disparity.

Gatekeepers and Control Structures

The Kayin State Border Guard Force (BGF)—a militia nominally loyal to the Myanmar military but effectively autonomous—operates approximately 30 smuggling gates along the Thaung Yin (Moei) River separating Thailand and Myanmar. This militia receives tacit junta permission to conduct smuggling in exchange for military loyalty during political instability and because the junta benefits from smuggling tax revenue and the foreign exchange it generates.

The smuggled commodity mix reveals Myanmar’s structural economic distortions: diesel and petrol (reflecting fuel scarcity), mobile phones and accessories (responding to telecommunications demand), consumer beverages, second-hand vehicles, and luxury goods targeted at regime-connected elites. Each of these commodities faces import restrictions or high tariffs through official channels, creating profit opportunities for smugglers exceeding legal arbitrage margins.

Cultural Legitimization and Normalization

Anthropological research has documented that smuggling constitutes “chiwit” (a way of life) for riverside merchants in border communities, dating back generations and predating modern state formation. This cultural embedding means that border communities view smuggling not as illegality but as legitimate commerce operating under different regulatory regimes. Even state-side customs officials participate in this system through informal “tea money” payments that effectively legalize transactions.

This normalization creates a structural problem for economic formalization: any attempt by Myanmar’s government to enforce stricter import licensing or customs collection faces not merely organized criminal resistance but community-level resistance from populations whose historical livelihoods depend on cross-border informal trade.

Economics of Control and Perverse Incentives

The military regime’s approach to managing the balance of payments crisis has inadvertently amplified smuggling. Implementing import licenses on 81% of tariff lines (up from 35% pre-coup) while maintaining an overvalued official exchange rate (2,094 kyat/USD) versus black market rates (3,000-4,000 kyat/USD based on December 2025 estimates) creates arbitrage opportunities that render legal imports uncompetitive. Businessmen facing impossible official import procedures rationally shift to smuggling, which works despite regulatory barriers.

This creates a vicious cycle: smuggling reduces formal import statistics, permitting junta officials to claim trade surpluses; these claimed surpluses justify continued import restrictions; restrictions deepen smuggling; smuggling further reduces formal trade reporting. The regime’s trade statistics (claiming a $7.84 billion export vs. $7.79 billion import balance in official data) bear no relationship to actual flows when informal trade is included.

Regional Dimensions and Strategic Implications

Border trade relationships with China reflect Myanmar’s geopolitical dependency. Myanmar’s northern border permits direct access to Yunnan Province, with Chinese merchants and traders operating extensively within Myanmar’s informal economy. Chinese companies dominate jade and rare earth mineral trading, effectively creating a situation where Myanmar’s most valuable resources are funneled directly to China through informal channels with minimal government oversight.

Thailand maintains economic leverage through its role as primary smuggling source, creating implicit Thai influence over Myanmar’s import policies and pricing. India and Bangladesh border regions see lower-magnitude smuggling but serve critical roles in consumer goods and fuel supply.

5. Garment Manufacturing: Sectoral Collapse

Employment and Historical Significance

Myanmar’s garment sector once represented a centerpiece of industrial policy, employing approximately 1 million workers (95% women) across 700,000+ positions in formal factories, with an additional 2+ million family members dependent on garment worker wages. The sector generated approximately $800 million in FY2024-25 exports, concentrated in US and EU markets that valued Myanmar’s combination of ultra-low wages, duty-free export access under LDC preferences, and geographical proximity to major apparel retail hubs.

Factory Closures and Labor Market Collapse

Since the February 2021 coup, at least 150 garment factories have closed permanently, with December 2024 alone witnessing 10 factory closures. These closures represent direct job losses for 100,000+ workers and indirect impacts on dependent family members facing income collapse.

The causes of closure evolved over time: initial closures (2021-2023) reflected political instability, Civil Disobedience Movement worker participation (boycotting production), and energy shortages limiting factory operations. Subsequent closures (2023-2025) resulted from order cancellations as international brands divested due to sanctions, ESG concerns around labor rights, and worker boycotts.

However, the shock that delivered a potentially fatal blow came from US tariffs implemented in August 2025. The Trump administration’s July 2025 announcement of “reciprocal tariffs” imposed a 40% tariff rate on Myanmar garments—the highest among major Southeast Asian competitors after other nations received substantial reductions.

Myanmar faces the highest US garment tariff rate (40%) after July 2025 reductions, while competitors received substantially larger cuts. Myanmar’s rate of 40% vs Vietnam’s 25%, Cambodia’s 32%, and Indonesia’s 22% creates a massive competitive disadvantage for Myanmar’s garment exporters despite ultra-low labor costs

Tariff Disadvantage and Competitive Unraveling

The tariff disparity reveals Myanmar’s structural isolation from geopolitical accommodation. While Cambodia’s rate was reduced from 49% to 32%, Vietnam’s from 46% to 25%, Indonesia’s from 32% to 22%, and Bangladesh maintained 37%, Myanmar’s 44% rate was reduced only modestly to 40%. This 8-18 percentage point disadvantage relative to regional competitors is insurmountable in apparel manufacturing, where product prices are globally set commodities and margin differences of 5-7% routinely determine production location.

The tariff creates a mathematical impossibility: Myanmar’s ultra-low wages (approximately 40-50% below Bangladesh and 30% below Vietnam) cannot overcome a 40% duty in a market where typical apparel markups are 25-35%. Purchasers cannot absorb tariff costs while maintaining retail prices, forcing brand purchasing managers to reallocate orders toward Vietnam, Cambodia, and Bangladesh.

Initial reactions were swift: Twinkle (Myanmar), manufacturing for Callaway Golf and Samsonite, closed operations; SDI Manufacture, Wan Xin Myanmar, and Eternal Fashion followed. Some factories began seeking orders from Japan, South Korea, and EU markets to replace lost US business, but these alternative markets lack the scale to absorb capacity.

Labor Rights and International Pressure

Compounding tariff pressures, the International Labour Organization invoked Article 33—its most serious enforcement mechanism—for Myanmar’s non-compliance with labor rights obligations regarding freedom of association and elimination of forced labor. This designation permits ILO-coordinated pressure on buyer brands to disengage from Myanmar sourcing, creating reputational and liability risks that accelerate order cancellations.

The junta’s response—arrests of workers reporting labor violations, forced conscription of garment factory workers, suppression of union organizing—have directly validated ILO concerns and strengthened international pressure to exclude Myanmar from ethical supply chains.

Structural Impediments to Recovery

Unlike historical manufacturing sector recoveries that rely on cost and wage competitiveness, Myanmar’s garment sector faces four non-price obstacles that wages cannot overcome:

- Political Risk: Investors require stability; Myanmar’s ongoing civil conflict, frequent internet shutdowns, and conscription of workers create uninsurable risks.

- Supply Chain Fragmentation: Many garment manufacturers require integrated sourcing (fabric, trim, findings, finished goods); Myanmar’s disrupted logistics and foreign exchange controls prevent integrated operations.

- Sustainability Compliance: EU and other premium markets increasingly mandate ESG certification; Myanmar’s minimal compliance infrastructure and labor rights violations disqualify most factories from premium segments.

- Tariff Penalty: The 40% US tariff is not a competitive disadvantage but a sectoral death sentence unless tariffs are substantially reduced.

Outlook

Unless the Trump administration materially reduces Myanmar’s tariff rate or the political situation stabilizes sufficiently to restore brand confidence, Myanmar’s garment sector will likely contract to 200,000-300,000 workers (from current 700,000+) by 2028. This represents an existential employment crisis for Myanmar’s women workers and dependent families.

6. Telecommunications and Digital Services: Growth Despite Collapse

Sector Overview and Market Position

Myanmar’s telecommunications sector presents a counterintuitive narrative: growth in certain dimensions persists despite broader economic collapse. The sector is valued at approximately USD 1.81-1.9 billion in 2024-2025, growing at 2.3% CAGR through 2030, with expanding mobile penetration and digital service adoption.

The sector’s major players include state-owned Myanmar Posts and Telecommunications (MPT), private operators Ooredoo, Mytel, and Atom (formerly Telenor), alongside digital service providers including Wave Money (mobile money, 80% market share), KBZPay, AYA Bank’s digital services, and TrueMoney Myanmar.

Mobile Money Success and Financial Inclusion

Wave Money stands out as a sectoral bright spot, providing mobile financial services to tens of millions of Burmese across the country’s limited formal banking infrastructure. The platform operates through approximately 58,000 agents nationwide, the majority of whom are women operating in rural areas through small retail kiosks (Store Sai)—a model paralleling the Sari-Sari stores of the Philippines.

Wave Money’s services—person-to-person transfers, merchant payments (QR code-based), international remittances to migrant workers in Thailand and Malaysia, and bill payments—address fundamental financial needs in a cash-based economy with minimal formal banking access. Transaction volumes experienced double-digit growth in 2024, and interoperability with banks through CBM Net and the national MMQR payment scheme has expanded digital payment adoption.

Female agent participation (58% of 58,000 agents) has created income opportunities for rural women in contexts where formal employment is limited, creating a socioeconomic multiplier despite low individual transaction values.

Digital Divide and Constraints

However, the sector’s growth occurs within a constrained context:

- Poverty Limiting Adoption: With 49% of households below poverty line, digital financial services adoption skews toward urban and middle-income populations; rural and conflict-affected regions remain cash-dependent.

- Internet Instability: Myanmar’s internet infrastructure faces frequent shutdowns ordered by the junta, with surveillance and blocking of opposition communication channels, creating user distrust of digital platforms.

- Conscription and Instability: Military conscription (February 2024) has accelerated youth emigration, reducing domestic user growth and remittance inflows from remaining workers.

- Inflation Impact: Kyat depreciation reduces purchasing power for digital services; consumers prioritize basic consumption over digital transactions during currency crises.

International Remittances as Lifeline

Myanmar’s migrant worker population—estimated at 2+ million working in Thailand, Malaysia, Singapore, and Gulf states—represents a critical remittance source. However, formal banking access among migrant workers is limited; many depend on informal hawala-style transfer networks. Wave Money’s expansion into international remittances aims to formalize these flows, reducing transaction costs and improving safety. Success would create a countercyclical stabilizer: as domestic wages collapse, overseas remittances could partially offset income losses for recipient households.

Regulatory Uncertainty

The junta’s control over telecommunications operators creates regulatory unpredictability. The military has intervened in mobile money pricing, internet service provisioning, and operational autonomy. State ownership of MPT (25% of market) creates coordination risks where government priorities override commercial efficiency.

Cross-Sectoral Economic Context: The Macroeconomic Crisis

Growth and Contraction Dynamics

Myanmar’s economic trajectory since the coup represents an unambiguous structural break. The pre-coup decade (2011-2021) averaged 6% annual growth, supported by liberalization, foreign investment, and regional integration. Post-coup, growth has been negative or near-zero across four consecutive years:

- FY2024: 0.8%

- FY2025: 0.2% (forecast)

- FY2025-26: -2.5% (ADB June 2025 forecast; December 2025 shows modest improvement to 1.1% but remains fragile)

This contraction is attributable to declines across all major sectors: agriculture (-2.3% in FY2024), industry (-0.1%), and services (-0.5%), reflecting systematic compression of productive capacity.

Inflation and Currency Crisis

Inflation has become the dominant macroeconomic shock for ordinary Burmese:

Myanmar’s inflation exploded from 3.64% pre-coup to 34.1% by April 2025, driven by currency depreciation, money printing to address civil disobedience shortages, and supply chain collapse. While easing to ~22% by December 2025, inflation remains 4-6x pre-coup levels, severely eroding purchasing power

Peak inflation reached 34.1% in April 2025 (from 3.64% pre-coup), eroding purchasing power faster than nominal wage gains. Food prices—the dominant household expenditure—increased 27% between October 2023 and April 2024, with regional variations revealing spatial inequality: conflict-affected areas experienced 40-200% food price increases.

The currency crisis compounds inflation’s impact. The Myanmar kyat depreciated from approximately 3,000-3,500 kyat/USD (early 2021) to black market rates reaching 7,500 kyat/USD in August 2024—a 70% loss of value. While official rates stabilized around 2,094 kyat/USD by January 2026, black market rates persist at 3,200-3,500, indicating persistent investor distrust of the currency.

Myanmar’s kyat experienced catastrophic depreciation, particularly in black markets where rates reached 7,500/USD in August 2024 (3.5x the official rate), driven by foreign currency shortages, money printing, and investor capital flight. Official stabilization attempts through currency controls have not restored confidence

The currency collapse reflects multiple reinforcing dynamics:

- Foreign exchange shortages from trade collapse and military capital controls

- Money printing to address cash shortages from Civil Disobedience Movement disruptions

- Investor capital flight due to political risk

- Junta currency control attempts that created arbitrage (official overvaluation vs. black market depreciation)

Poverty and Household Impact

The UNDP estimated 49% of households in poverty as of 2023, with the figure likely exceeding 55-60% by late 2025 given inflation acceleration and economic contraction. The “disappearing middle class” represents a structural shift: households previously above poverty line have fallen into poverty as wage growth failed to keep pace with 30%+ inflation, and informal employment (lacking benefits) has replaced formal sector jobs.

Unemployment peaked at 4.34% in 2021 (during initial coup disruptions) but declined as people transitioned to informal work; true underemployment (part-time informal work providing insufficient income) is substantially higher, potentially 15-25% of the labor force.

Fiscal Crisis and State Capacity

Myanmar’s fiscal deficit reached 5.7% of GDP in FY2024, projected to remain at 5.5-5.6% through FY2026. This structural deficit reflects:

- Weak tax revenue (formally-employed workers and formal businesses are declining)

- Increased state spending on security forces (conscription, military operations)

- Declining gas revenue as production declines

- Mining revenue capture difficulties (informal sector dominance)

The fiscal deficit of 5.5-5.7% is unsustainable without monetary financing (money printing) or external financing (impossible given sanctions). This implies either significant spending cuts (affecting security apparatus sustainability), tax rate increases (politically risky and compliance-difficult), or further currency depreciation through money printing.

Foreign Direct Investment Collapse

Myanmar’s FDI inflows collapsed 68.6% below pre-coup levels, declining from ~$1.2B pre-coup baseline to $656M by January 2025. Coupled with ASEAN peers attracting record investment ($230B in 2023), Myanmar now ranks last among ASEAN members, unable to compete on investor confidence or rule of law

Myanmar’s FDI inflows plummeted 68.6% below pre-coup baselines, declining from approximately $1.2 billion annually (FY2020) to $656 million in January 2025 commitments. This collapse reflects:

- International Firm Withdrawal: 17 companies publicly announced withdrawal, 9 suspended operations, with nearly 13% of total foreign firms ceasing all Myanmar activities.

- Policy Uncertainty: Junta regulations are opaque, applied inconsistently, and subject to sudden change; businesses cannot plan forward.

- Banking Isolation: Myanmar’s FATF blacklist (October 2022) complicates international financial transactions and complicates multinational company operations.

- Comparative Disadvantage: ASEAN peer economies attracted record FDI in 2023 ($230 billion), with Vietnam ($36B) and Indonesia ($29B) receiving multiples of Myanmar’s inflows, demonstrating that Myanmar is not competing for regional FDI.

Current Account and External Imbalances

The current account deficit narrowed to 2.0% of GDP in FY2025 (from 3.5% pre-coup), not due to improved competitiveness but due to import collapse: with businesses unable to access foreign exchange and consumers unable to afford imports, merchandise imports fell 24.6% in Q2 FY2024. This represents economic contraction masquerading as balance-of-payments improvement.

Understanding Myanmar’s Inverted Economy

Myanmar presents a unique case study where state weakness paradoxically strengthens informal economies and armed groups. In conventional development contexts, state collapse leads to humanitarian crises; in Myanmar, collapse has created parallel economic structures that sustain armed conflict while reducing regime state capacity.

The Informal Economy as Stabilizer and Destabilizer

Border trade, jade smuggling, and informal finance (hawala-style remittances) together likely exceed $5-7 billion annually—potentially matching formal export revenues. This informal economy provides:

- Survival income for populations excluded from formal employment (40-50% of working-age population)

- Foreign exchange for regime spending (through taxing border trade)

- Financing for armed opposition (through mining revenues)

- Consumer goods access despite import restrictions

However, this informalization simultaneously:

- Reduces tax revenue (regime cannot tax informal transactions)

- Finances conflict actors (jade/mineral revenues fund ethnic armed groups)

- Prevents policy coordination (informal actors respond to opportunities, not government directives)

- Creates vulnerability to external shocks (black market exchange rates, border closures)

Why Recovery Is Structurally Difficult

Myanmar’s economic recovery faces obstacles that do not apply to Bangladesh or other post-conflict economies:

- Sanctions Without Political Pressure: International sanctions target the regime but do not target the sectors most critical to regime finance (gas, jade trade); this creates penalties for the general population without leverage over regime behavior.

- Tariff Penalty: The 40% US garment tariff is not a temporary negotiating position but a structural penalty on Myanmar’s largest formal export sector; no wage reduction can overcome this penalty.

- Conflict Sustainability: Armed groups’ ability to finance themselves through mining revenues means they can sustain conflict indefinitely without occupying territory or achieving political power, creating a stalemate where neither side can defeat the other militarily.

- Regime Incentive Inversion: The regime benefits from border trade smuggling and mining informality; formalizing these sectors would reduce regime capture but also tax revenue from informal taxation of smugglers. Formal policies that would stabilize the economy (currency liberalization, import license elimination, formal mining regulation) would reduce regime discretionary spending and patronage.

Conclusion: State Collapse, Survival Economies, and Perpetual Crisis

Myanmar’s sectoral analysis reveals an economy that has inverted from a recovering lower-middle-income country (2011-2021) to a near-complete state collapse (2021-2025). Formal sectors—garments, manufacturing, formal finance—have contracted, while informal sectors—smuggling, illicit mining, informal remittances—have expanded. This inversion is not a temporary recession but a structural reconfiguration where the regime sustains itself through extraction of informal economic rents while armed opposition groups sustain themselves through mining revenues.

Natural gas remains a critical hard-currency earner, but declining production and absent new investment suggest this resource will contract significantly by 2030. Rice exports continue but under increasing pressure from input costs, climate shocks, and conflict. The garment sector faces near-terminal decline due to 40% US tariffs and labor rights pressures. Telecommunications shows modest growth, but digital financial services cannot compensate for 30%+ inflation and poverty affecting 50% of the population.

Unlike Bangladesh’s strategic challenge of managing tariff cliff and export diversification, Myanmar faces an existential state capacity crisis where economic instruments are being weaponized (tariffs, sanctions) against populations that have limited influence over regime behavior. Recovery would require either political transition (restoring legitimacy and foreign investment) or regime economic reform (currency liberalization, formal trade integration, mining regulation)—each politically implausible under military rule.

For international actors, Myanmar presents a tragic case where conventional development economics frameworks provide limited guidance, and where sectoral interventions (tariffs, sanctions, trade restrictions) may inadvertently strengthen informal networks and armed conflict rather than supporting civilian welfare or democratic transition.

official Myanmar government websites

| Myanmar national portal | Myanmar national portal |

| ministry of myanmar | ministry of myanmar |

Read more country case studies done before this.

| Qatar | Qatar |

| iran | iran |

| bangladesh | bangladesh |

| china | china |

| Indonesia | Indonesia |

| hong kong | hong kong |

| japan | japan |

| sinagpore | singapore |

| taiwan | taiwan |

| uAE | UAE |

| vietnam | vietnam |

| saudi arbia | saudi arbia |

| Malaysia | Malaysia |

| india | india |

| south korea | south korea |

Hey linkvaobong88com, are you really the best link to Bong88? I am so tired from link scams, hope you’re legit. Show me the money here: linkvaobong88com