Marina Bay Sands

Singapore economic growth drivers 2026.

Singapore stands as one of the world’s most strategically important trading hubs and a global financial powerhouse. From its position at the intersection of major maritime routes to its position as Asia’s fintech leader, the city-state has engineered a sophisticated, multi-pillar economy that punches far above the weight of its 5.6 million population. This case study examines Singapore’s economic architecture, competitive advantages, and strategic positioning in an increasingly uncertain geopolitical and commercial environment.

singapore Economic Performance and Growth Trajectory

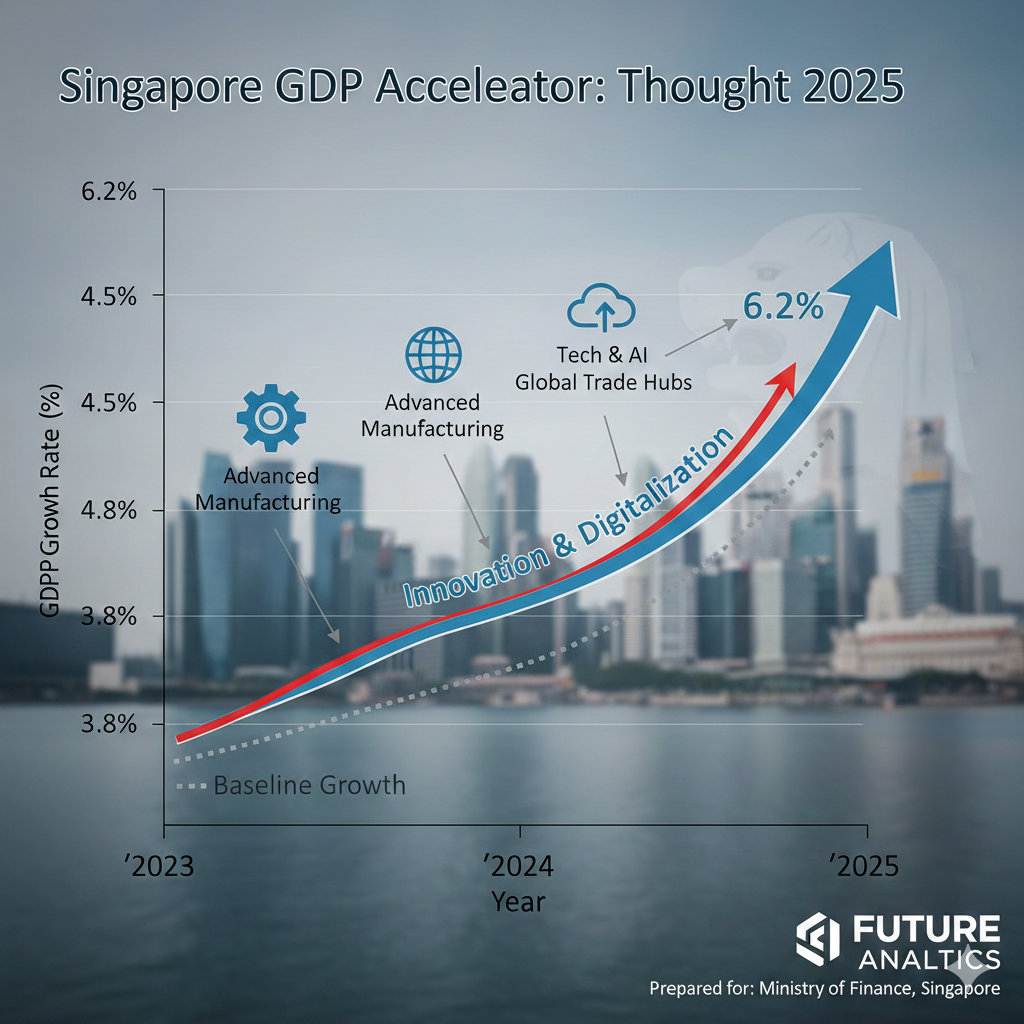

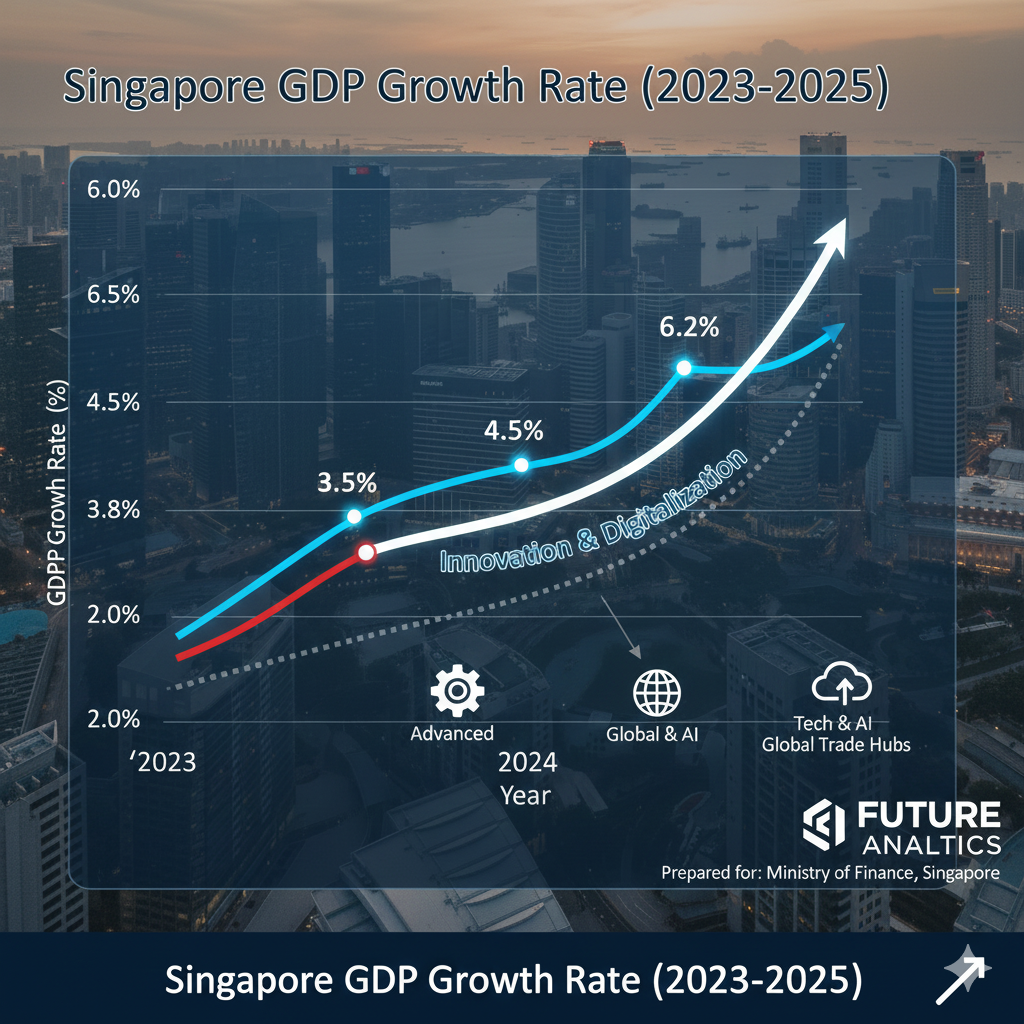

Singapore’s economy demonstrated robust recovery and expansion through 2024 and 2025, reversing the sluggish growth of 2023. The gross domestic product expanded 4.4% in 2024, marking the fastest pace since 2021, with Q4 recording 5% year-over-year growth. This momentum carried into 2025, with the Ministry of Trade and Industry upgrading full-year forecasts from an initial 1.5-2.5% range to approximately 4.0%, driven by stronger-than-expected manufacturing and trade sector performance. Q3 2025 recorded 4.2% growth, while Q4 surged to 5.7% year-over-year, with manufacturing alone expanding 15% driven by biomedical and electronics clusters.

Singapore GDP Growth Rate (2023-2025)

The acceleration reflects structural strengths in Singapore’s economy: its critical role in global supply chains, technological sophistication, and ability to attract capital-intensive industries. However, forward guidance for 2026 projects moderation to 1.0-3.0% growth, reflecting anticipated headwinds from US-China trade tensions, semiconductor export uncertainty, and decelerating regional growth. This cyclical pattern—strong performance followed by expected moderation—has characterized Singapore’s economic profile for decades, as the city-state’s economy is highly sensitive to external demand fluctuations.

singapore Port and Maritime Operations: A Global Chokepoiant

Singapore Port stands as the world’s second-largest container port and the uncontested global leader in transshipment operations, processing more than 40 million twenty-foot equivalent units (TEUs) annually. The port’s strategic location at the Strait of Malacca—the crossroads between the Indian Ocean and South China Sea—creates a natural entrepôt function for Asian-Europe trade flows. Approximately 200 shipping lines maintain connections through Singapore to more than 600 ports across 123 countries, with nearly 140,000 annual vessel calls (the highest of any port globally) and roughly 1,000 vessels present in the harbor at any moment. Singapore economic growth drivers 2026.

Port and Maritime Operations: A Global Chokepoiant

The transshipment operation itself represents an extraordinary achievement: 85-87% of the port’s throughput comprises containers being transferred from one vessel to another, enabling Singapore to function as a global exchange point for maritime logistics. This specialization creates powerful backward linkages into logistics, warehousing, ship finance, maritime insurance, and maritime law services, anchoring an entire ecosystem of supporting industries.

Singapore Port Container Throughput: Historical and Projected Growth (2024-2040)

Tuas Mega Port, launching Phase 1 in 2025, represents the next evolutionary stage. The world’s largest fully automated container terminal will incorporate automated guided vehicles (AGVs), AI-powered cranes capable of 30 moves per hour, digital twins for operational optimization, and zero-emission container movement systems. The facility is designed to scale capacity to 65 million TEUs by 2040, addressing anticipated growth in container shipping while reducing carbon intensity. This automation trajectory positions Singapore ahead of competitors—Port Klang (Malaysia) and Tanjung Pelepas emerging as alternatives—but also requires continuous capital investment and workforce retraining.

However, the Strait itself faces structural vulnerabilities. The narrow 800-kilometer passage carries approximately 30% of global container traffic and 25% of the world’s oil supply, making it a critical chokepoint for global commerce. Red Sea disruptions in 2024-2025 rerouted 15% additional traffic through Singapore, straining port capacity and turnaround times. Piracy threats, geopolitical tensions in the South China Sea, and climate impacts on the strait create ongoing risks that port operators cannot fully mitigate through infrastructure alone.

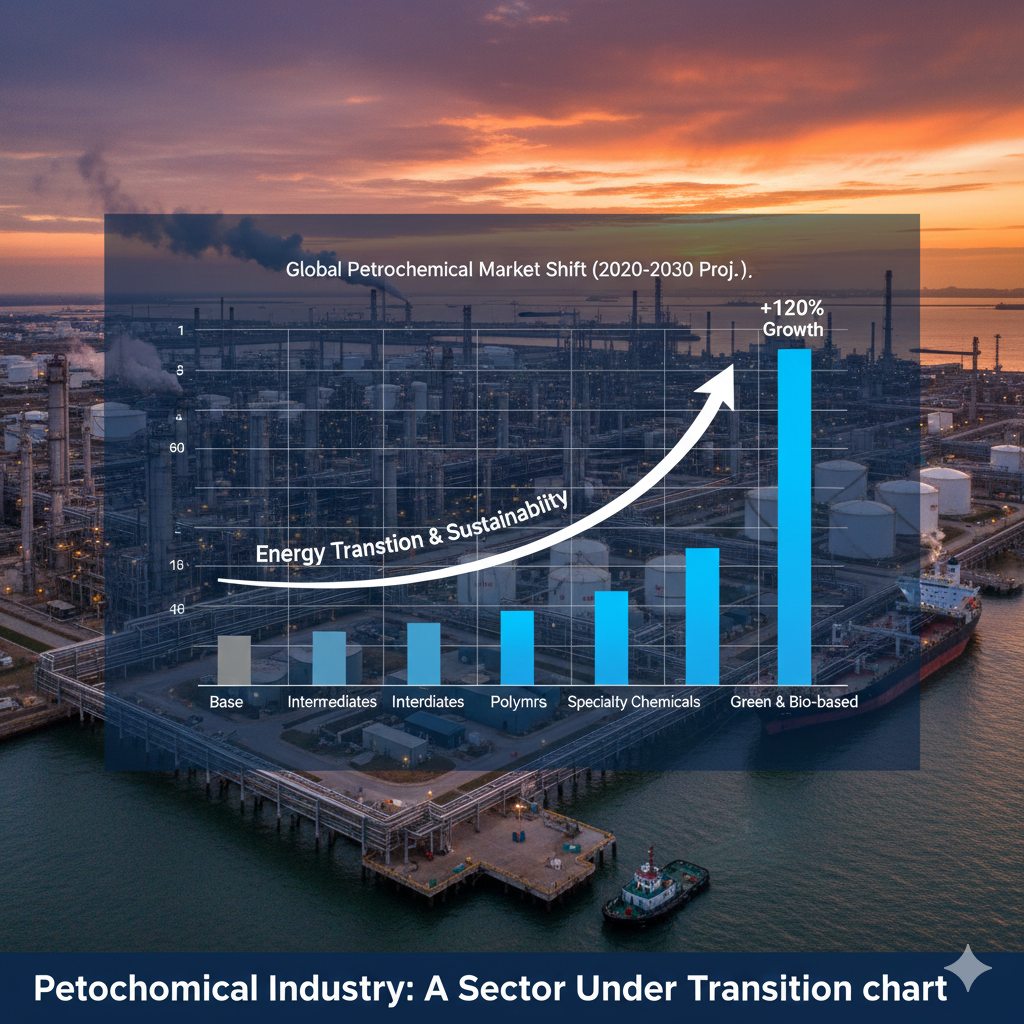

singapore Petrochemical Industry: A Sector Under Transition

Singapore ranks as the world’s third-largest oil trading hub and a major petrochemical production center, refining approximately 1.1 million barrels per day and contributing roughly 6% to Singapore’s GDP. The city-state exports over $45 billion in petrochemical products annually, producing 6.7 million tons of ethylene and 4.4 million tons of propylene—the building blocks for plastics, fibers, and specialty chemicals used across global supply chains.

Three major refineries—Shell (Pulau Bukom), ExxonMobil (Jurong Island), and Singapore Refining Company—have anchored the sector since the 1960s. However, 2025 marked a watershed moment: Shell announced the sale of its Pulau Bukom refinery to CAPGC, a joint venture between Indonesian petrochemical leader Chandra Asri and Swiss trading giant Glencore, effective end of 2025. This divestment, preceded by Shell’s halving of capacity from 500,000 to 237,000 barrels per day in 2020 and cancellation of biofuel and base oil projects, signals investor hesitation regarding Singapore’s refining future.

The underlying challenge is structural: Middle East refiners benefit from adjacent crude oil reserves and vastly lower feedstock costs, while China has rapidly expanded refining capacity through state subsidies and integration with petrochemical clusters. Singapore’s advantage lies in its geographic position as an entrepôt (purchasing crude at market prices and exporting refined products and chemicals) and in its conversion to specialty chemicals and sustainable aviation fuel (SAF). Singapore now hosts the world’s largest SAF production facility and is projected for the largest capacity increases alongside the U.S. and China. Specialty chemicals output rose 29.1% in 2024 compared to 1.7% for petroleum-based products, illustrating the sector’s pivot.

The government provided up to 76% tax rebates for refiners and petrochemical companies in 2024-2025 to ease cost pressures. While these incentives may stabilize near-term operations, they signal that competitive economics no longer favor high-capacity crude refining in Singapore—the sector is restructuring toward specialty, biochemical, and renewable fuel niches where geographic location and technical expertise matter more than feedstock costs.

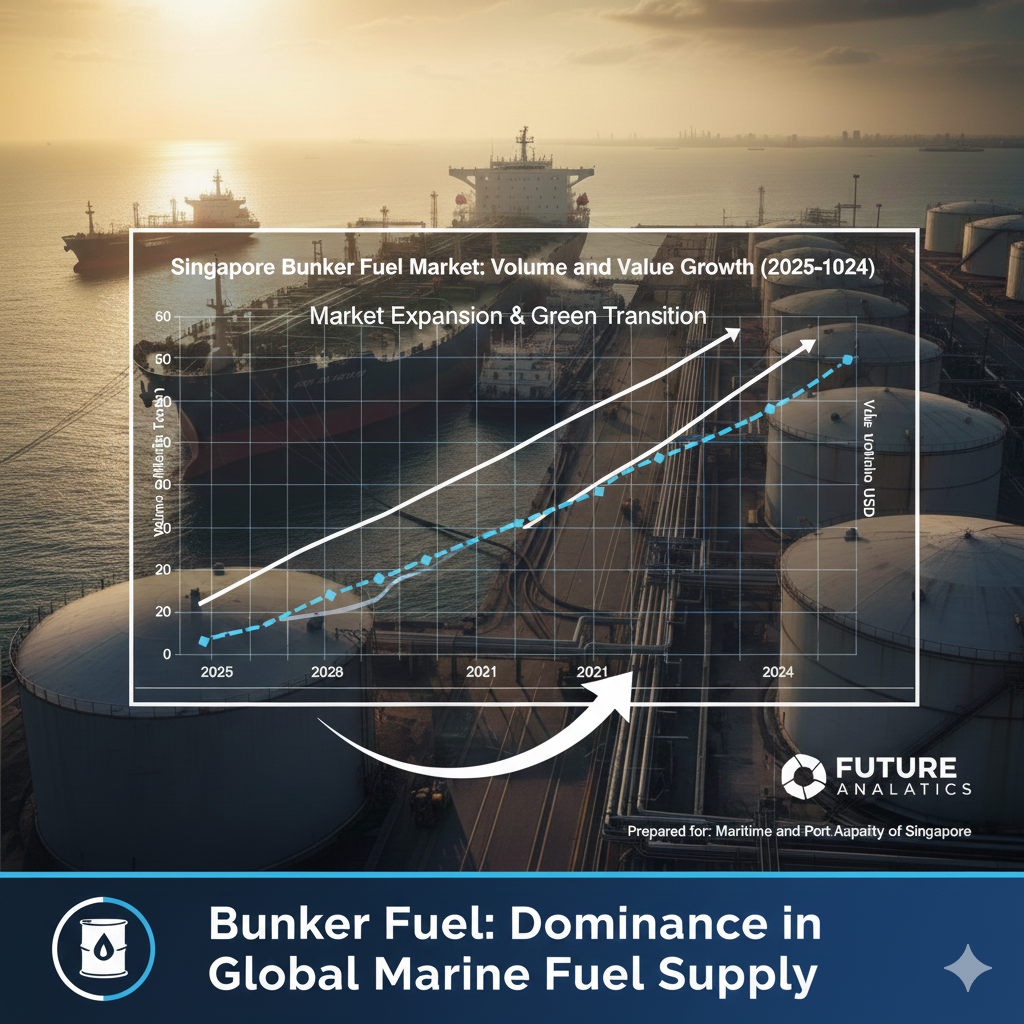

Bunker Fuel: Dominance in Global Marine Fuel Supply

Singapore’s bunkering (marine fuel) business represents one of its most profitable and strategically important operations. As the world’s largest marine refueling hub, Singapore supplied approximately 30-40% of global bunker fuel, with 2025 volumes reaching 58.23 million metric tonnes, projected to grow to 94.23 million tonnes by 2034 at a 5.85% compound annual growth rate. Market value expanded from $22.1 billion in 2024 to projected $33.3 billion by 2034.

July 2025 bunker sales reached 4.92 million metric tons (the highest in 18 months), up 7.0% month-over-month and 5.7% year-over-year, with October 2025 recording 5.07 million metric tons—a new historical high. Low-sulfur fuel oil (LSFO), mandated by the IMO 2020 regulation, comprises approximately 72% of the market, with marine gas oil (MGO) and alternative fuels (biofuels, LNG, methanol) accounting for the remainder.

Singapore Bunker Fuel Market: Volume and Value Growth (2025-2034)

The bunkering sector reflects both Singapore’s strategic geographic position and the global maritime industry’s reliance on this narrow chokepoint. Container shipping represents the largest revenue contributor, reflecting surging e-commerce and cross-border trade. However, bunkering faces regulatory and competitive pressures: carbon pricing (Singapore implemented carbon taxation in 2023), rising prices driven by crude volatility, and environmental regulations driving transition to low-emission fuels. The market’s growth trajectory depends on sustained maritime trade volumes and the speed of fuel-switching toward biofuels, LNG, methanol, and ammonia—transitions that require significant infrastructure investment across global ports.

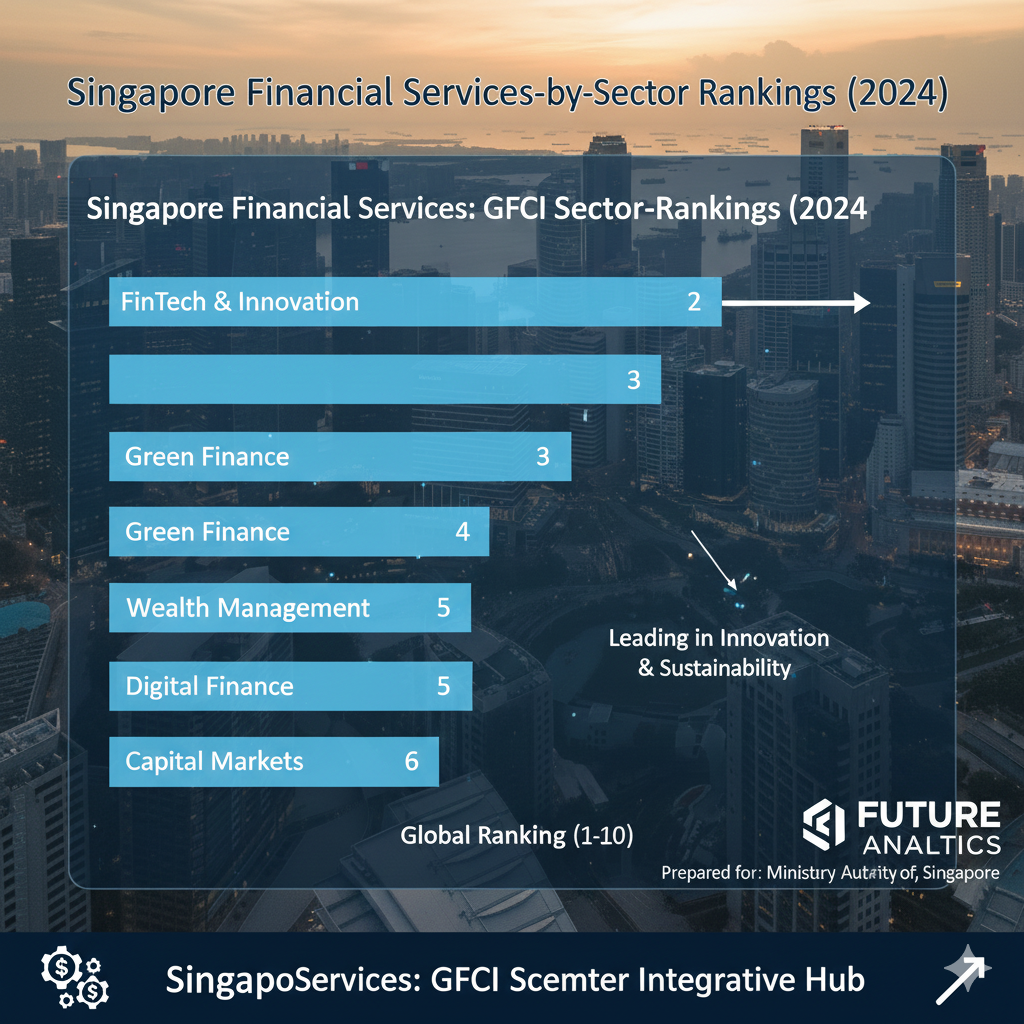

Financial Services: Asia’s Premier Integrative Hub

Singapore ranks as the world’s fourth most competitive financial center, according to the Global Financial Centres Index (GFCI 37-38), behind New York, London, and Hong Kong. More tellingly, Singapore ranks first globally in professional services, second in trading, third in fintech and government regulatory frameworks, fourth in insurance, and fifth in investment management, demonstrating breadth across the entire financial ecosystem.

The financial sector contributed approximately SGD 87.8 billion (approximately USD 65 billion) to GDP, with banking assets from DBS, OCBC, and UOB collectively exceeding USD 1.64 trillion, making Singapore’s banking sector the dominant force in ASEAN. The Singapore Exchange (SGX) maintains a market capitalization of over USD 644 billion, substantially exceeding regional competitors such as Bursa Malaysia (USD 400 billion) and the Indonesian Stock Exchange (USD 600 billion).

Singapore Financial Services: GFCI Sector-by-Sector Rankings

Singapore’s financial strength reflects several reinforcing factors: a 17% corporate tax rate (competitive with regional alternatives), English language fluency, a world-class legal system compatible with common law jurisdictions, stable governance, and English-educated talent. These structural advantages create a “stickiness” that encourages multinational financial institutions and wealth managers to establish regional headquarters in Singapore rather than alternatives such as Bangkok, Jakarta, or Kuala Lumpur, which increasingly compete for financial services investment.

FinTech Ecosystem: Payments Innovation and Blockchain Expansion

Singapore has emerged as Asia’s undisputed fintech leader, with 520 registered fintech companies (2025) and 8 fintech unicorns spanning digital banking, wealthtech, and insurtech sectors. The Global Fintech Index ranks Singapore sixth globally, ahead of Hong Kong and Seoul, and the city-state commands approximately 59% of all fintech funding across ASEAN, along with over 50% of fintech deals by number.

The Monetary Authority of Singapore (MAS) has engineered a regulatory approach that explicitly permits innovation while maintaining prudential oversight—a critical distinction that attracts entrepreneurs and technology companies globally. Over 100 firms now hold MAS-issued digital banking, payment, or capital market licenses, creating a thick institutional layer of regulated fintechs.

PayNow, launched in 2017, exemplifies Singapore’s payment innovation. The real-time payment system enables instant, secure fund transfers using mobile numbers or identity card numbers, built on the Fast and Secure Transfers (FAST) network. PayNow transactions surged from 138.38 million in 2020 (a 48% increase from 2019) to projected 393 million by 2025, demonstrating extraordinary adoption rates. The system has been extended internationally: a 2023 linkage between Singapore’s PayNow and India’s UPI system enabled real-time, low-cost cross-border transactions benefiting migrant workers, businesses, and consumers in both nations.

Project Nexus represents the next frontier: a multi-national payments connectivity initiative aiming to link payment systems globally to enable faster, cheaper international transfers. The Singapore Payments Network (SPaN), incorporated in 2025 with operational readiness targeted for end 2026, consolidates governance of Singapore’s eight national payment schemes (FAST, GIRO, PayNow, SGQR) under unified oversight, simplifying compliance and fostering innovation partnerships.

However, 2025 also revealed fintech vulnerabilities. The collapse of Tokenize Xchange left over SGD 266 million owed to customers, prompting MAS review of crypto asset service provider regulations and a broader reckoning with security versus convenience trade-offs. Surging scams led banks to introduce stronger authentication guardrails, sparking national debate about whether security measures unnecessarily impede user experience. These challenges suggest that fintech regulation remains a continuous negotiation between innovation and protection.

Web3 and Blockchain Expansion

The Web3 segment (blockchain, digital assets, cryptocurrencies) has expanded dramatically within Singapore’s fintech ecosystem, growing from 5% of the ecosystem (2022) to 16% (2024), becoming the second-largest segment behind payments. This expansion reflects MAS’s regulatory clarity on cryptocurrency and tokenization, which—in contrast to blanket bans in many jurisdictions—has created a permissive environment for experimentation.

The regulatory framework distinguishes between different types of digital asset activities: cryptocurrency exchanges, decentralized finance (DeFi) platforms, and tokenization of traditional assets each receive differentiated regulatory treatment. This nuance has attracted global blockchain companies and enables Singapore to position itself as a bridge between traditional finance and decentralized systems.

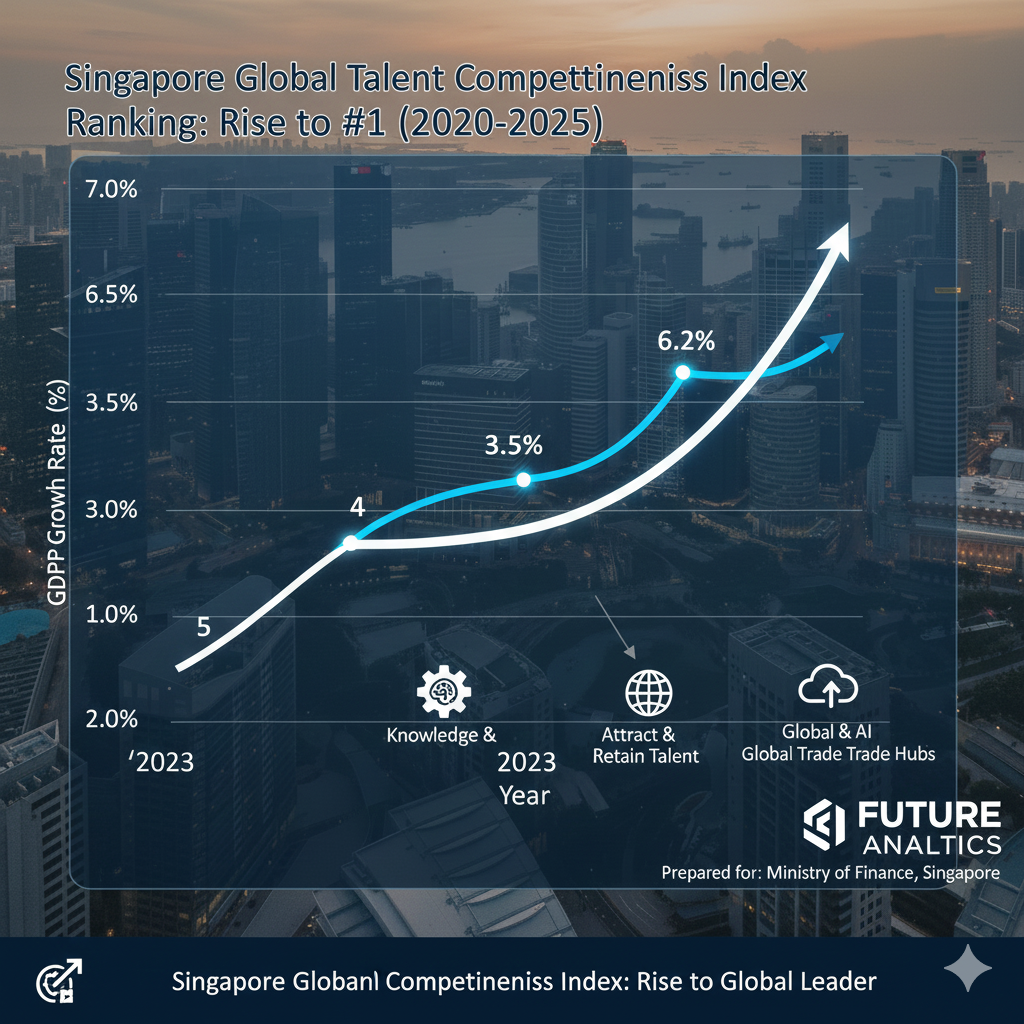

Human Capital and Talent Competitiveness

In a landmark 2025 development, Singapore claimed the top position in INSEAD’s Global Talent Competitiveness Index (GTCI) for the first time, dethroning Switzerland after 12 consecutive years at #1. Singapore’s ascent reflects five major competitive dimensions:

- Generalist Adaptive Skills: Singapore ranked first globally on “generalist adaptive skills,” a metric measuring workers’ soft skills, digital literacy, and innovation mindset. The government’s education system evolution prioritizes cross-functional flexibility and AI literacy over narrow technical specialization.

- Talent Retention: Singapore improved from 38th to 31st in talent retention between 2023 and 2025, addressing historical brain drain concerns. The city-state’s improved retention reflects both better compensation in competitive sectors (fintech, biomedical) and quality-of-life improvements.

- Institutional Quality: Strong educational institutions (National University of Singapore, Nanyang Technological University, INSEAD’s Asia campus), transparent governance, and rule of law create favorable conditions for talent development.

- Innovation Capacity: AI concentration, startup ecosystem maturity, and R&D spending demonstrate Singapore’s commitment to innovation-driven workforce development.

- Economic Competitiveness: The financial sector alone employs approximately 190,000 professionals, while biomedical and electronics clusters provide high-wage employment opportunities competitive with developed economies.

Singapore Global Talent Competitiveness Index Ranking: Rise to #1 (2020-2025)

This talent advantage carries strategic importance: as global companies face talent shortages and geographic dispersion of work, Singapore’s positioning as a talent magnet for Asia-Pacific operations becomes increasingly valuable. Unlike geographic advantages (ports, straits) that cannot be relocated, talent mobility creates competitive dynamics favoring jurisdictions that actively cultivate ecosystems for professional development, remuneration, and lifestyle quality.

Biomedical Manufacturing: A Model of Coordinated Cluster Development

Singapore’s biomedical manufacturing sector represents perhaps the clearest example of successful government-led cluster development in the post-war period. Since 2000, the city-state transformed from a pharmaceutical manufacturing outpost into an integrated biomedical sciences hub spanning drug discovery, clinical research, manufacturing, and healthcare delivery—achieving this transition through 25 years of coordinated, patient policy.

The sector’s economic contribution is substantial: biomedical manufacturing value added reached SGD 19.57 billion (approximately USD 14.5 billion) by 2019, representing 20% of total manufacturing value added and approximately 4% of GDP. Between 2000 and 2019, biomedical manufacturing grew at a compound annual growth rate of 9% (the fastest-growing manufacturing sector) compared to 5% average growth across all manufacturing. Employment surged from minimal levels in 2000 to 24,384 workers by 2019, with 65% in medical technology manufacturing and 35% in pharmaceuticals.

Most remarkably, 2025 saw a 79.3% year-over-year surge in biomedical manufacturing output, with pharmaceutical output jumping 124.3%, suggesting a new acceleration phase.

Singapore Biomedical Manufacturing Sector: 25-Year Growth Trajectory (2000-2025)

The policy architecture involved three distinct phases:

Foundation Phase (2000-2005): The government allocated USD 1 billion to construct Biopolis, a purpose-built 183-hectare biomedical research campus modeled on global best practices. The Economic Development Board (EDB), Agency for Science, Technology and Research (A*STAR), and Ministry of Trade and Industry coordinated international recruitment of leading scientists to head research institutions. A SGD 12 billion manufacturing output target for 2005 was met a year early, creating institutional confidence in the sector’s potential.

Attraction Phase (2006-2010): With research infrastructure in place and scientific leadership established, the focus shifted to attracting multinational pharmaceutical and medical device companies. Companies including Pfizer, Merck, Novartis, and Johnson & Johnson established manufacturing, R&D, and regional headquarters operations in Singapore. The second phase of Tuas Biomedical Park expanded the precinct by 188 hectares, providing additional infrastructure for expansion.

Consolidation Phase (2010+): The mature ecosystem attracted full-service operations: 8 of the world’s top 10 pharmaceutical companies now operate facilities in Singapore, producing 4 of the world’s top 10 drugs by profit. The sector transitioned from cost-driven manufacturing (competing with China and India on labor) to value-added activities in specialized pharmaceuticals, biologics, medical devices, and advanced manufacturing.

This model offers lessons for technology cluster development: coordinated government investment in physical infrastructure and talent recruitment can overcome initial disadvantages and create “sticky” competitive advantages when paired with regulatory stability and sufficient scale to attract multinational capital.

The Strait of Malacca: Geopolitical Chokepoint and Economic Vulnerability

Singapore’s geographic blessing—the Strait of Malacca—is simultaneously a structural vulnerability. The 800-kilometer passage accounts for approximately 30% of global container traffic and 25% of the world’s oil supply, with a daily value of goods in transit estimated at USD 2.74 billion. For China, the strait represents a critical vulnerability: approximately 80% of Chinese oil imports flow through this passage, and any disruption would immediately threaten energy security for the world’s second-largest economy.

The strait’s importance to Singapore is more nuanced: rather than a vulnerability, it is the fundamental justification for Singapore’s port dominance, financial services concentration, and bunkering operations. Control of this chokepoint—through geographic positioning, infrastructure investment, and political neutrality—has enabled Singapore to extract economic rents through transshipment operations, bunkering, and financial services for centuries.

However, 2024-2025 demonstrated the strait’s fragility. Red Sea disruptions rerouted 15% additional shipping traffic through Singapore, straining port capacity and turnaround times. South China Sea geopolitical tensions, piracy risks, and climate impacts on the strait’s navigability create ongoing risks. Academic research modeling hypothetical Strait blockade scenarios estimates annual global economic losses exceeding USD 2 trillion—an unfathomable figure that underlies the strategic calculus of all Indo-Pacific powers.

The broader vulnerability is that the Strait’s bottleneck characteristics have created an alternative logic: Southeast Asian governments, manufacturers, and shipping companies increasingly explore alternative routes, ports, and supply chain configurations to reduce dependence on this single chokepoint. Proposed canal projects between Thailand and Malaysia, expansion of ports in Malaysia, Indonesia, and Vietnam, and Arctic shipping route development reflect this diffusion of supply chains. While none of these alternatives offer the efficiency of the Strait, their development threatens Singapore’s unique economic moat.

Financial Competitiveness: Structural Advantages and Regional Competition

Singapore’s financial sector benefits from reinforcing advantages: rule of law and stable governance create confidence; a transparent legal system compatible with Anglo-American conventions attracts multinational institutions; 24/7 operations connect time zones across Asian and Western markets; and English language fluency eliminates communication friction. The city-state’s lack of natural resources historically forced development of human capital and service-sector sophistication, creating a comparative advantage in financial services unavailable to resource-rich competitors.

However, regional competition is intensifying. Bangkok, Jakarta, and Kuala Lumpur are aggressively expanding their banking and fintech ecosystems with government support. Bangkok has positioned itself as a Southeast Asian technology hub with lower operational costs than Singapore. Jakarta’s massive domestic financial services market (serving 275 million Indonesians) creates natural advantages for banks focusing on retail financial services. Kuala Lumpur’s Islamic finance hub offers specialized expertise Singapore cannot easily match.

Singapore’s response focuses on specialization: global institutional investors, wealth management, trading and derivatives, professional services, and cross-border fintech innovation. These segments require talent concentration, regulatory sophistication, and institutional depth—areas where Singapore’s advantages are most durable. Tax incentives, regulatory clarity, and talent pipelines create barriers to entry for competitors, though not impenetrable ones.

Forward Outlook and Strategic Challenges

Singapore faces four major strategic challenges in the medium term:

First, supply chain diversification away from China reduces the city-state’s transshipment advantage. As manufacturing disperses from China to Vietnam, Indonesia, Thailand, and India, the assumption that goods flow through one major Asian entrepôt (Singapore) weakens. Multiple ports and logistics routes become optimal, reducing the compression of traffic through the Strait of Malacca and Singapore Port.

Second, automation in port operations reduces the labor-dependent service industries that historically employed low-wage workers. Tuas Port’s full automation sets a precedent: future generations of port workers will number in dozens (managing AI systems) rather than thousands (loading/unloading containers). Singapore’s aging population and tight labor markets mean the economy cannot sustain employment-intensive service jobs indefinitely.

Third, geopolitical uncertainty in the Indo-Pacific creates planning difficulties for multinational firms and investors. US-China tensions, South China Sea disputes, and potential Taiwan conflict scenarios create tail risk for Singapore-based operations. Companies increasingly diversify across multiple Asian hubs rather than concentrating in Singapore, reducing single-point-of-failure exposure.

Fourth, climate change threatens the Strait of Malacca’s navigability and increases Singapore’s vulnerability to sea-level rise. As a low-lying island city-state, rising sea levels threaten critical infrastructure. The Strait itself faces risks from extreme weather events that could temporarily disrupt traffic. Singapore’s government is investing in climate adaptation (seawalls, drainage systems), but these costs increase over the 2025-2050 period.

Conversely, Singapore has positioned itself advantageously for several growth catalysts: (1) increasing demand for advanced semiconductors (data center chips) benefits the electronics cluster; (2) biomedical manufacturing momentum suggests the sector will continue expansion; (3) green energy transition creates demand for renewable fuel production (SAF, biofuels); and (4) emerging markets’ rising wealth supports growth in wealth management and financial services.

Conclusion: A Sophisticated Entrepôt Navigating Structural Transition

Singapore represents a remarkable economic achievement: a small island city-state with no natural resources has engineered a position as one of the world’s most important trading hubs, a financial powerhouse, and an innovation center. This achievement reflects five foundational factors: (1) geographic positioning at a critical maritime chokepoint; (2) institutional excellence including rule of law, transparent governance, and regulatory clarity; (3) long-term policy orientation enabling coordinated cluster development (biomedical, petrochemical, fintech); (4) talent competitiveness through continuous educational innovation; and (5) strategic capital deployment in infrastructure and human development.

The 4.4% GDP growth in 2024 and upgraded 4.0% forecast for 2025 reflect sustained economic momentum despite headwinds. However, forward growth projections of 1.0-3.0% for 2026 signal a return to trend, reflecting the economy’s sensitivity to external demand and the maturing nature of service-dependent growth models.

The city-state’s greatest vulnerabilities are structural rather than cyclical: supply chain diversification away from China, automation reducing service-sector employment, geopolitical uncertainty in the Indo-Pacific, and climate impacts on a low-lying island. These challenges cannot be addressed through policy adjustment alone; instead, they require continuous economic reinvention and repositioning toward higher-value services and technological sophistication.

Conversely, Singapore’s elevation to #1 in the Global Talent Competitiveness Index in 2025 suggests the city-state has succeeded in cultivating the adaptive, innovation-driven workforce required for 21st-century competition. Combined with strong financial sector positioning, biomedical manufacturing momentum, and fintech innovation, Singapore appears well-positioned for the 2025-2030 period—though the longer-term trajectory (2030-2050) depends on continued strategic adaptation to fundamental shifts in global supply chains, energy systems, and geopolitical alignment.

Singapore GDP Growth Rate (2023-2025)

Singapore Port Container Throughput: Historical and Projected Growth (2024-2040)

Singapore Bunker Fuel Market: Volume and Value Growth (2025-2034)

Singapore Financial Services: GFCI Sector-by-Sector Rankings

Singapore Global Talent Competitiveness Index Ranking: Rise to #1 (2020-2025)

| Singapore Government Portal | Singapore Government Portal |

| Open Data Portal | Open Data Portal |

| GoBusiness Singapore | GoBusiness Singapore |

| HealthHub | HealthHub |

| Singapore Digital Gateway | Singapore Digital Gateway |

| ScamShield | ScamShield |

| NS Portal | NS Portal |

| Parking.sg | Parking.sg |

Singapore: In-Depth Economic Case Study highlights the city-state’s impressive journey. With its top spot in the Global Talent Competitiveness Index for 2025, it’s clear that Singapore knows how to nurture a savvy workforce ready to tackle modern challenges. The booming financial sector, along with growth in biomedical and fintech, shows that Singapore is gearing up for an exciting future. However, staying ahead will require smart strategies to navigate the shifting global landscape in the coming decades.