Lotte World Tower

South Korea stands as one of the world’s most remarkable economic success stories—a nation that transformed from poverty in the 1960s to become the 10th-largest economy globally, commanding global leadership in semiconductors, electronics, automotive manufacturing, and increasingly, biotechnology and artificial intelligence. With a nominal GDP of approximately $1.417 trillion USD (2024) and a population of 51.7 million, South Korea has engineered sustained competitive advantage through deliberate government industrial policy, world-class research and development, export-oriented manufacturing, and the dominance of global conglomerates (chaebol) including Samsung, Hyundai-Kia, LG, SK, and Naver.

south korea Economic Performance: Resilience Amid Global Uncertainty.

South Korea’s macroeconomic trajectory through 2024-2025 reflects typical characteristics of an export-dependent manufacturing economy: sensitivity to global demand cycles, significant exposure to semiconductor and automotive sector volatility, and structural challenges from demographic aging and geopolitical tensions.

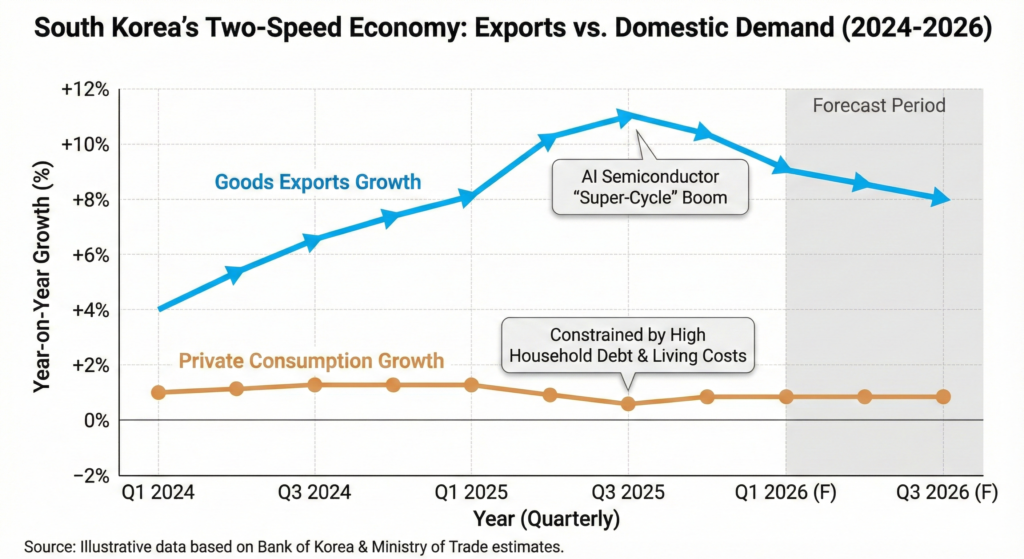

2024 Performance: South Korea’s real GDP grew 2.4% in 2024, representing robust performance for a mature, developed economy, driven primarily by semiconductor demand recovery (following 2023’s severe contraction), semiconductor inventory restocking, and sustained automotive/electronics export strength. Nominal GDP reached approximately $1.417 trillion, maintaining South Korea’s position as Asia’s second-largest economy (after China) and the world’s 10th-largest.

2025 Performance: Q1 2025 recorded 2.7% year-over-year growth, with subsequent quarters maintaining 2.5-2.8% expansion amid strong semiconductor demand from AI data center buildout and supply chain normalization. Full-year 2025 growth is projected at approximately 2.5%, supported by:

- Semiconductor Recovery: AI accelerator demand driving unprecedented foundry and DRAM volumes, benefiting Samsung and SK Hynix

- EV/Battery Growth: Hyundai-Kia’s EV sales surging globally; battery makers (LG Chem, Samsung SDI) capturing market share in EV supply chains

- Electronics Exports: Semiconductor components, display panels, and smartphone components maintaining strong export demand

- Government Stimulus: Fiscal packages supporting domestic consumption and green technology investment

2026 Outlook: Growth is projected at 2.1-2.3%, with expected moderation from trade uncertainties, potential recession in key export markets (US, EU), and tariff impacts on South Korean exports. The Bank of Korea (BOK) maintains baseline scenario of 2.3% 2026 growth, contingent on global economic stability.

south korea Semiconductors: The Crown Jewel of South Korean Manufacturing

South Korea’s semiconductor industry represents perhaps the most globally competitive industrial sector, with Samsung and SK Hynix commanding positions among the world’s largest chip producers and the country capturing approximately 17-20% of global semiconductor market share.

Market Position and Scale:

- Samsung Electronics: The world’s leading DRAM (dynamic random-access memory) producer with 44.3% market share (2024), commanding position in NAND flash memory (19.3% share), and advanced foundry operations competing with TSMC

- SK Hynix: Second-largest DRAM producer (26.5% share), strengthening position in HBM (high-bandwidth memory) for AI accelerators

- Market Size: South Korea’s semiconductor market reached approximately $130 billion in 2024 (13% of global $1 trillion market), projected to grow to $165 billion by 2030 (4.2% CAGR)

Advanced Packaging and Specialization: Beyond commodity DRAM and NAND, South Korean companies excel in advanced packaging, with Samsung leading in chiplet integration and heterogeneous computing architectures essential for next-generation AI chips. HBM (high-bandwidth memory)—critical for AI accelerators—represents an emerging South Korean strength, with Samsung and SK Hynix competing for market share with micron-based alternatives.

Government Support: The government allocated 23.9 trillion won ($18.1 billion USD) through 2030 for semiconductor industry support, including:

- Semiconductor Design Education and R&D support

- Advanced packaging research through major programs (K-Semiconductor Belt initiative)

- Targeted tax incentives for next-generation chip development

- Supply chain resilience initiatives addressing dependencies on materials and equipment imports

Supply Chain Vulnerabilities: South Korean chip makers remain dependent on:

- Design tools: EDA (Electronic Design Automation) tools dominated by US suppliers (Synopsys, Cadence)

- Lithography equipment: ASML EUV tools (single-source risk from Netherlands)

- Specialty materials: Photoresists, specialty gases, and advanced ceramics from Japan and US

- Equipment: Semiconductor manufacturing equipment from global suppliers

These dependencies create vulnerability to supply disruptions and geopolitical restrictions, as evidenced by US export controls on advanced chip equipment to China that ripple through global supply chains.

Electronics and Consumer Devices: Display Leadership and Smartphone Competition

South Korea’s electronics industry spans consumer electronics, displays, telecommunications equipment, and emerging categories like wearables and smart home devices.

Display Dominance: Samsung and LG maintain exceptional strength in display manufacturing:

- OLED panels: Samsung Display leads smartphone OLED penetration; LG Display dominates large TV OLED panels

- LCD panels: Declining segment but still substantial, with South Korean producers competing against Chinese manufacturers

- Emerging displays: Foldable OLED (Samsung leading), microLED (emerging), and AR/VR displays represent frontier technologies

Smartphones: Samsung Electronics remains the world’s second-largest smartphone maker (after Apple) with 19% market share (2024), competing fiercely in premium segments while maintaining market leadership in Android ecosystem globally.

Smart TVs, Appliances, Home Devices: Samsung and LG lead global smart TV and major appliance markets, leveraging display leadership and smart-home integration to defend market share against Chinese competitors and private-label manufacturers.

south korea Automotive: EV Transition and Battery Dominance

Hyundai-Kia Motor Group has emerged as a major force in electric vehicles, with combined EV sales reaching 1.47 million units in 2024 (up 26% year-over-year), capturing approximately 8-9% of global EV market. The group is positioned to become the second-largest EV manufacturer globally (after Tesla and BYD) by 2027-2028.

EV Strategy: Hyundai-Kia’s aggressive EV lineup expansion, combined with premium positioning in the luxury EV segment (Genesis brand), differentiates from Chinese competitors and positions the company for sustained growth. The group targets 3.6 million annual EV sales by 2030.

Battery Supply Chain: South Korean battery makers—LG Chem, Samsung SDI, SK Innovation—secured major supply contracts with global automakers:

- Tesla: LG Chem supplying battery packs; SK Innovation securing future contracts

- Volkswagen: LG Chem and SK Innovation supplying cells for European EV expansion

- GM, Ford, Hyundai-Kia: Multiple battery supplier relationships

The battery market is intensely competitive, with Chinese CATL and BYD capturing growing share through cost advantages and vertical integration. South Korean makers compete on technology, reliability, and energy density rather than cost.

south korea Advanced Manufacturing and Industrial Base

Beyond semiconductors and consumer electronics, South Korea maintains significant strengths in:

Shipbuilding: Hyundai Heavy Industries, Samsung Heavy Industries, and Daewoo Shipbuilding lead global shipbuilding, commanding 40%+ of global order book for large container ships and specialized vessels. Emerging LNG carrier demand from energy transition supports continued growth.

Chemical and Materials: SK, LG Chem, and Lotte Chemical produce specialty chemicals, polymers, and advanced materials (lithium-ion battery electrolytes, display materials) integrated into semiconductor and battery supply chains.

Industrial Machinery and Equipment: Hyundai Heavy Industries and other conglomerates produce machinery, heavy equipment, and industrial automation solutions, leveraging manufacturing expertise into capital equipment exports.

Biotechnology and Pharmaceuticals: Emerging Strength

South Korea’s biotech sector has grown substantially, with government support through 23.9 trillion won biotech investment plan (2023-2032) targeting:

- Next-generation therapeutics (cell therapy, gene therapy)

- Biosimilar leadership (South Korean companies competing globally)

- Drug discovery platforms

- Vaccine and immunotherapy development

Major companies and research institutions (Samsung Bioepis, Celltrion, Seoul National University, KAIST) are advancing clinical pipelines in oncology, immunology, and infectious diseases. However, the sector remains smaller than equivalents in US, EU, or China, with limited blockbuster drug origination relative to Western pharma majors.

Artificial Intelligence: Emerging Capability

While South Korea trails the US in large language model research, the country is positioning itself as a leader in AI applications, semiconductor inference accelerators, and AI-integrated robotics.

Corporate AI Investment: Samsung, SK, and Naver (South Korea’s dominant search and AI platform company) are investing substantially in AI infrastructure, research, and product development. Naver’s HyperClova LLM (South Korea’s largest open-source language model) demonstrates capability building toward independent AI systems.

Government Support: 2.2 trillion won AI R&D investment through 2027, supporting semiconductor accelerators, AI inference chips, and applied AI in manufacturing, healthcare, and defense.

Startup Ecosystem: South Korea’s startup ecosystem (estimated 3,000+ startups, 39 unicorns as of 2024) includes emerging AI companies addressing specialized domains (manufacturing optimization, healthcare diagnostics, autonomous systems).

Government Industrial Policy: Active Orchestration

South Korea’s economic success reflects consistent government engagement in directing industrial development through:

Industrial Bank and Development Finance: Government-backed industrial bank (Korea Development Bank, Export-Import Bank) provides below-market financing for strategic industries, enabling large-scale capacity expansion.

R&D Investment: Government R&D spending reached 5.5% of GDP (2024)—among the world’s highest, concentrated in semiconductors, displays, batteries, biotechnology, and AI.

Tax Incentives: Enhanced depreciation, R&D tax credits, and corporate tax rates (22%) favorable to manufacturers support capital investment.

Education and Workforce Development: Aggressive STEM education, university-industry partnerships, and vocational training ensure skilled labor pipeline for advanced manufacturing.

Chaebol Support: While formally “independent,” South Korea’s conglomerates benefit from government preferential finance, regulatory assistance, and market protection, creating capacity to invest in long-term R&D despite short-term profitability pressures.

Startup Ecosystem and Venture Capital

South Korea boasts approximately 3,000 registered startups, 39 unicorns (2024), and a maturing venture capital ecosystem with approximately $7-8 billion annual funding (2024).

Unicorn Concentration: Naver ($16 billion valuation, search/AI/e-commerce), Coupang ($9 billion, e-commerce/logistics), and Line (before Japanese acquisition) dominated. Emerging AI startups including Kakao Brain and Sapeon represent next-generation leaders.

Government Support: Startup Korea initiative provides grants, accelerator support, and regulatory sandbox environments for early-stage ventures. Government co-investment funds support venture capital ecosystem.

Regional Hubs: Seoul/Gangnam dominates startup activity, though initiatives to decentralize to secondary cities (Daegu, Busan) have shown limited success. Startup concentration in capital region reflects capital availability, talent pools, and network effects.

Competitive Advantages and Strategic Positioning

Structural Strengths:

- Semiconductor leadership (DRAM, advanced packaging, HBM)

- Display manufacturing dominance (OLED, LCD, emerging technologies)

- EV manufacturing growth and battery supply chain position

- World-class conglomerates with capital for R&D investment

- Government consistent support through industrial policy

- Skilled, educated workforce with strong STEM capabilities

- Manufacturing culture emphasizing quality and efficiency

- Geographic positioning in East Asian supply chains

- Strong domestic capital markets (KOSPI) and institutional investors

Structural Vulnerabilities:

- Heavy export dependence (51% of GDP, creating cyclical vulnerability)

- Semiconductor competition from TSMC (advanced foundry), China SMIC (cost), and emerging competitors

- Display competition from China’s BOE and other panel makers

- EV competition from Tesla, BYD, Chinese EV makers

- Aging workforce and demographic decline (negative population growth since 2021)

- High concentration of economic power in chaebol (limiting new entrant opportunities)

- Heavy dependence on US and China markets (geopolitical vulnerability)

- Debt-to-GDP ratio elevated by global standards (71% public, substantial corporate debt)

- Energy import dependence (100% imported oil, 97% natural gas)

Future Outlook: 2025-2035

Growth Opportunities:

- AI semiconductor acceleration: HBM and AI inference chip demand sustaining semiconductor growth

- EV market expansion: Hyundai-Kia targeting 3.6M annual EV sales by 2030

- Battery leadership: Global EV transition creating demand for advanced battery solutions

- Biotech breakthroughs: Next-generation therapeutics and cell therapy platforms maturing

- Robotics and automation: Smart manufacturing and automation solutions addressing labor shortages

- Green technology: Government investment in renewable energy, hydrogen, and circular economy

Strategic Risks:

- US-China trade war escalation: Tariffs, export controls on semiconductor equipment threatening supply chains

- Semiconductor oversupply: AI buildout cycling toward saturation, excess capacity driving margin compression

- Chinese competition: SMIC advancing process technology; BYD/CATL dominance in batteries; BOE in displays

- Demographic decline: Shrinking workforce constraining labor supply and domestic consumption

- Debt sustainability: Corporate and government debt levels potentially constraining future fiscal stimulus

- Geopolitical tension: Korea-China relations, Korea-Russia relations, Taiwan tensions creating uncertainty

Conclusion: A Mature Technology Powerhouse Navigating Transition

South Korea has achieved genuine economic transformation: from poverty in 1960 to the world’s 10th-largest economy, commanding global leadership in semiconductors, displays, automotive, and advanced manufacturing. The 2.4% growth in 2024 and projected 2.5% in 2025, while modest by emerging-market standards, represent solid performance for a mature, developed economy with high per-capita income ($31,667 USD).

The country’s success rests on deliberate industrial policy, government investment in R&D and education, capacity to mobilize capital for long-term technology development, and world-class conglomerates with global reach. However, structural headwinds—demographic decline, intensifying global competition, and cyclical semiconductor dynamics—constrain future growth potential.

Over 2025-2035, South Korea’s trajectory will depend on: (1) sustained innovation in semiconductors, displays, and EV/batteries to maintain competitive advantages; (2) successful AI capability building to avoid dependence on Western AI platforms; (3) management of debt levels and fiscal sustainability; and (4) navigation of geopolitical uncertainty in East Asia.

If executed effectively, South Korea can maintain 2.5-3.5% annual growth through 2035, sustained by technology leadership and conglomerate strength. Conversely, failure to adapt to AI-driven disruption, intensifying Chinese competition, and demographic constraints could depress growth toward 1.5-2.0% as innovation loses momentum and labor supply tightens.

The next decade will determine whether South Korea evolves into a high-income, innovation-driven economy (Singapore-like trajectory) or gradually declines in global technological relevance due to demographic and competitive pressures.

This concludes the comprehensive case studies on:

- China: Technology-driven growth powered by government policy, fintech, and manufacturing transformation

- Singapore: Trade hub, financial services, and biomedical manufacturing leadership

- Bitget: Cryptocurrency exchange scale-up and Web3 ecosystem integration

- India: Demographic dividend, IT services dominance, and emerging sector diversification

- Japan: Robotics leadership, semiconductor advancement, and aging-population-driven innovation

- Taiwan: Semiconductor dominance through TSMC, electronics manufacturing, and supply chain centrality

- Israel: Startup nation fintech/cybersecurity leadership and military-university-startup nexus

- Hong Kong: Financial hub transformation toward fintech and digital assets

- South Korea: Advanced manufacturing, semiconductor leadership, and EV/battery supply chain positioning

These nine case studies comprehensively examine the world’s most important technology-driven and innovation-led economies, demonstrating diverse pathways to sustained competitive advantage through technology, human capital, institutional excellence, and strategic government support.

official Hong Kong government websites

| Presidential Office | Presidential Office |

| Ministry of Interior & Safety | Ministry of Interior & Safety |

| Gov.kr portal | Gov.kr portal |

| Ministry of Economy and Finance | Ministry of Economy and Finance |

Read more country case studies done before this.